Sales of new single-family houses dipped slightly in October but is still 41.5% above October 2019’s estimate of 706,000, according to the U.S. Census Bureau and the Department of Housing and Urban Development. New-home sales last month were at a seasonally adjusted rate of 999,000, 0.3% lower than the revised September rate of 1,002,000.

The continued elevated new-home sales follows other strong residential market indicators for the month of October. Zonda reported this week that pending new-home sales were tracking higher year over year in nearly every top U.S. market. And existing home sales were up 26.6% from a year ago, according to the National Association of Realtors.

According to the data, the median sales price of new houses sold in October was $330,600, while the average sales price was $386,200.

The seasonally adjusted estimate for new homes for sale was 278,000 at the end of October, representing a 3.3-month supply at the current sales rate.

“Today’s report from the Census Bureau suggested that demand for new homes in October continued to be strong, but supply constraints will likely limit the growth of new-home sales going forward,” noted Fannie Mae chief economist Doug Duncan. “The monthly sales pace is now reported to have been essentially flat for the three months at an elevated level of about 1 million annualized units, a rate not seen since 2006. However, sales are increasingly being driven from homes not yet under construction. The share of homes sold but not yet started rose for the third straight month and now represents the highest share of total sales since 2005, while the number of fully completed homes sold hit the lowest level since the COVID-19-related shutdowns this past April.”

Duncan added that the sales pace continued to exceed its typical relationship with the rate of construction. “At the comparatively low level of started homes available for sale, we believe the current sales pace to be unsustainable. We continue to project a convergence in coming months via a softening of sales while housing starts show comparative strength,” he said. “However, due to the revisions to past months’ numbers and third quarter sales coming in stronger than previously thought, our fourth quarter forecasts for both new sales and new housing starts will likely be revised upward.”

On Thursday (Nov. 19), the U.S. Department of Justice announced the filing and proposed settlement of an antitrust case against the National Association of Realtors that alleged the association established and enforced illegal restraints on the ways Realtors compete.

With the case filing, the Antitrust Division simultaneously filed a proposed settlement that requires NAR to repeal and modify its rules to provide greater transparency to home buyers about the commissions of brokers representing home buyers (buyer brokers), cease misrepresenting that buyer broker services are free, eliminate rules that prohibit filtering multiple listing services (MLS) listings based on the level of buyer broker commissions, and change its rules and policy which limit access to lockboxes to only NAR-affiliated real estate brokers. If approved, the settlement will enhance competition in the real estate market, resulting in more choice and better service for consumers, according to the U.S. Department of Justice.

The National Association of Realtors announced on its website on Thursday that NAR had reached an agreement with the U.S. Department of Justice to develop rules that more explicitly state what is already the spirit and intent of NAR’s Code of Ethics and MLS policies regarding providing information about commissions and MLS participation.

The announcement authored by NAR General Counsel Katie Johnson in the Realtor Magazine section of the association’s website, stated, “Our rules and policies have long been recognized for creating a competitive and efficient market that benefits home buyers and sellers. This agreement resolves the DOJ’s questions about the multiple listing service (MLS) and commissions and enables NAR to remain focused on supporting our members as they preserve, protect, and advance the American dream of homeownership,” NAR

NAR 2021 President Charlie Oppler said in a videotaped statement, “We want to be absolutely clear that while NAR disagrees with the characterization of our rules and policies and NAR admits no liability, wrongdoing or truth of any allegations by the DOJ, NAR has agreed to make certain changes to its rules to address the questions raised by the DOJ.”

NAR’s Johnson, who also serves as the association’s Chief Member Experience Officer, stated that although the exact language of the settlement agreement is still being finalized for NAR’s rule changes, most of the changes seek to more explicitly state what is already the spirit and intent of NAR’s Code of Ethics and MLS policies regarding providing information about commissions and MLS participation.

“Buying a home is one of life’s biggest and most important financial decisions,” said Assistant Attorney General Makan Delrahim of the Justice Department’s Antitrust Division. “Home buyers and sellers should be aware of all the broker fees they are paying. Today’s settlement prevents traditional brokers from impeding competition—including by internet-based methods of home buying and selling—by providing greater transparency to consumers about broker fees. This will increase price competition among brokers and lead to better quality of services for American home buyers and sellers.”

NAR General Counsel Katie Johnson

According to the complaint, NAR’s anticompetitive rules, policies, and practices include: (i) prohibiting MLSs that are affiliated with NAR from disclosing to prospective buyers the commission that the buyer broker will earn; (ii) allowing buyer brokers to misrepresent to buyers that a buyer broker’s services are free; (iii) enabling buyer brokers to filter MLS listings based on the level of buyer broker commissions offered; and (iv) limiting access to the lockboxes that provide licensed brokers with access to homes for sale to brokers who work for a NAR-affiliated MLS. These NAR rules, policies, practices have been widely adopted by NAR-affiliated MLSs resulting in decreased competition among real estate brokers, the DOJ charged.

NAR General Counsel Johnson went on to state on the NAR website that in accordance with the MLS system’s long-standing focus on creating an efficient, transparent marketplace for home buyers and sellers, the amount of compensation offered to buyers’ agents for each MLS listing will be made publicly available. Publicly accessible MLS data feeds will include offers of compensation, and buyers’ agents will have an affirmative obligation to provide such information to their clients for homes of interest.

“Relatedly, the rule changes re-affirm that MLSs and brokerages, as always, must provide consumers all properties that fit their criteria regardless of compensation offered or the name of the listing brokerage,” NAR’s Johnson wrote.

She also noted that there will be a rule enacted that will more definitively stated that buyers’ agents cannot represent their services as free to clients.

Finally, with the seller’s prior approval, a licensed real estate agent will have access to the lockboxes of properties listed on an MLS even if the agent does not subscribe to the MLS, NAR added.

NAR will work with the DOJ to agree on exact rule changes within 45 days; then the Board of Directors will then have to approve the new rules. The court overseeing the settlement must formally approve it.

“In entering this agreement with the DOJ, NAR disagrees with the DOJ’s characterization of our rules and policies, and NAR admits no liability, wrongdoing, or truth of any allegations by the DOJ. The agreement does not subject NAR to any fines or payments,” NAR’s Johnson stated.

She continued, “We’re proud to be associated with the MLS system that puts consumers first and benefits home buyers, sellers, and small-business brokerages—and is constantly building upon these principles. This agreement furthers NAR’s and the MLS system’s goal of creating an efficient marketplace that fosters cooperation between brokers for the benefit of consumers.”

The proposed settlement will be published in the Federal Register as required by the Antitrust Procedures and Penalties Act. Any person may submit written comments regarding the proposed final judgment within 60 days of its publications to Chief, Office of Decree Enforcement and Compliance, Antitrust Division, U.S. Department of Justice, 950 Pennsylvania Ave., N.W., Washington, DC 20530. At the conclusion of the 60-day comment period, the court may enter the proposed final judgment upon a finding that it serves the public interest.

Fueled by record-low mortgage rates and strong demand, existing home sales, as reported by the National Association of Realtors (NAR), rose for a fifth consecutive month in October and reached its highest level in almost 15 years.

Total existing home sales, including single-family homes, townhomes, condominiums and co-ops, rose 4.3% to a seasonally adjusted annual rate of 6.85 million in October, the highest level since November 2005. On a year-over-year basis, sales were 26.6% higher than a year ago.

The first-time buyer share increased to 32% in October from 31% both last month and a year ago. However, price gains threaten this share in the future. The October inventory level fell to 1.42 million units from 1.46 million units in September and is down from 1.77 million units a year ago.

At the current sales rate, the October unsold inventory represents an all-time low 2.5-month supply, down from 2.7-month in September and 3.9-month a year ago. This low level supply of resale homes is good news for home construction.

Homes stayed on the market for an average of just 21 days in October, an all-time low, seasonally even with last month and down from 36 days a year ago. In October, 72% of homes sold were on the market for less than a month.

The October all-cash sales share was 19% of transactions, up from 18% last month but unchanged from a year ago.

Tight supply continues to push up home prices. The October median sales price of all existing homes was $313,000, up 15.5% from a year ago, representing the 104th consecutive month of year-over-year increases. The median existing condominium/co-op price of $273,600 in October was up 10.3% from a year ago.

Regionally, all four regions saw month-over-month gains for existing home sales in October, ranging from 1.4% in the West to 8.6% in the Midwest. On a year-over-year basis, sales grew in all four regions as well, with the Northeast seeing the greatest gain (30.4%).

Though sales have flourished and demand remains strong due to low mortgage rates, the imbalance between housing supply and demand could hamper future sales by driving up home prices and restraining affordability. Though builder confidence soared to all-time high and housing starts at highest pace since the spring of 2007, more listings and home construction are still needed to meet this rising demand.

U.S. homebuilding increased more than expected in October as the housing market continues to be driven by record low mortgage rates, but momentum could slow amid a resurgence in new COVID-19 infections that is putting strain on the economic recovery.

The report from the Commerce Department on Wednesday also showed building permits unchanged at a 13-1/2-year high. It followed on the heels of data on Tuesday showing the smallest gain in retail sales in October since the recovery from the pandemic started in May. The economy is slowing as more than $3 trillion in government coronavirus relief dries up.

Daily new COVID-19 cases have been exceeding 100,000 since early this month, pushing the number of infections in the United States above 11 million, according to a Reuters tally. Several states and local governments have imposed restrictions on businesses, raising fears that the resulting weak demand could unleash a fresh wave of layoffs that could reverberate across the economy and slow the housing market’s run.

“The million dollar question remains how long the recovery in housing can continue as the shocking number of new coronavirus cases is paralyzing commerce in many parts of the country and leading to new restrictions and lockdowns,” said Chris Rupkey, chief economist at MUFG in New York.

Housing starts rose 4.9% to a seasonally adjusted annual rate of 1.530 million units last month. That lifted homebuilding closer to its pace of 1.567 million units in February. Economists polled by Reuters had forecast starts would rise to a rate of 1.460 million units in October.

Permits for future homebuilding were unchanged at a rate of 1.545 million units in October, the highest since March 2007.

The densely populated South region accounted for 56.1% of homebuilding last month. Groundbreaking activity also rose in the West and Midwest, but tumbled in the Northeast.

Homebuilding surged 14.2% on a year-on-year basis.

Single-family homebuilding, the largest share of the housing market, raced 6.4% to a seasonally adjusted annual rate of 1.179 million units last month, the highest level since April 2007.

Single-family starts have increased for six straight months. This segment of the market is being boosted by the pandemic, which has seen at least 21% of the labor force working from home. That has led to a migration from city centers to suburbs and other low-density areas as Americans seek out spacious accommodation for home offices and schools.

“The South and inland and mountain regions of the West are seeing a huge influx of residents from the large metro areas in the Northeast and West Coast,” said Mark Vitner, a senior economist at Wells Fargo Securities in Charlotte, North Carolina. “Just over 80% of all single-family homes built over the past year have been in the South or West, which means that construction can continue at a much higher pace during the winter months than in prior years.”

A survey on Tuesday showed confidence among single-family homebuilders rose to an all-time high in November. But builders said “lot and material availability is holding back some building activity.”

Single-family building permits climbed 0.6% to a rate of 1.120 million units in October.

A separate report on Wednesday from the Mortgage Bankers Association showed applications for loans to buy a home increased 4% last week from a week earlier.

The coronavirus recession, which started in February, has disproportionately affected lower-wage earners. At least 20 million people are on unemployment benefits.

The PHLX housing index was trading higher, outperforming a mixed U.S. stock market. The dollar slipped against a basket of currencies. Prices of longer-dated U.S. Treasuries were trading higher.

Though the housing market accounts for a fraction of gross domestic product, it has a bigger economic footprint. Its continued strength should help to keep the economy afloat even as GDP growth is expected to decelerate significantly in the fourth quarter after a historic performance in the July-September period.

Homebuilding is being driven by lean inventories, especially for previously-owned homes, and low mortgage rates. The 30-year fixed mortgage rate is around an average of 2.84%, according to data from mortgage finance agency Freddie Mac.

Starts for the volatile multi-family segment were unchanged at a pace of 351,000 units. Building permits for multi-family housing projects fell 1.6% to a rate of 425,000 units. It was the third straight monthly decline.

“This is an indication that developers are reining in investment as rental vacancy rates have risen,” said Matthew Pointon, property economist at Capital Economics in New York.

According to Wells Fargo Securities’ Vitner, rental data also suggest a shift in renter preferences away from urban lifestyle apartments to suburban apartments that offer more outdoor amenities.

Housing completions fell 4.5% to a rate of 1.343 million units last month. Realtors estimate that housing starts and completion rates need to be in a range of 1.5 million to 1.6 million units per month to close the inventory gap. The stock of housing under construction increased 1.2% to a rate of 1.224 million units, the highest since December 2006.

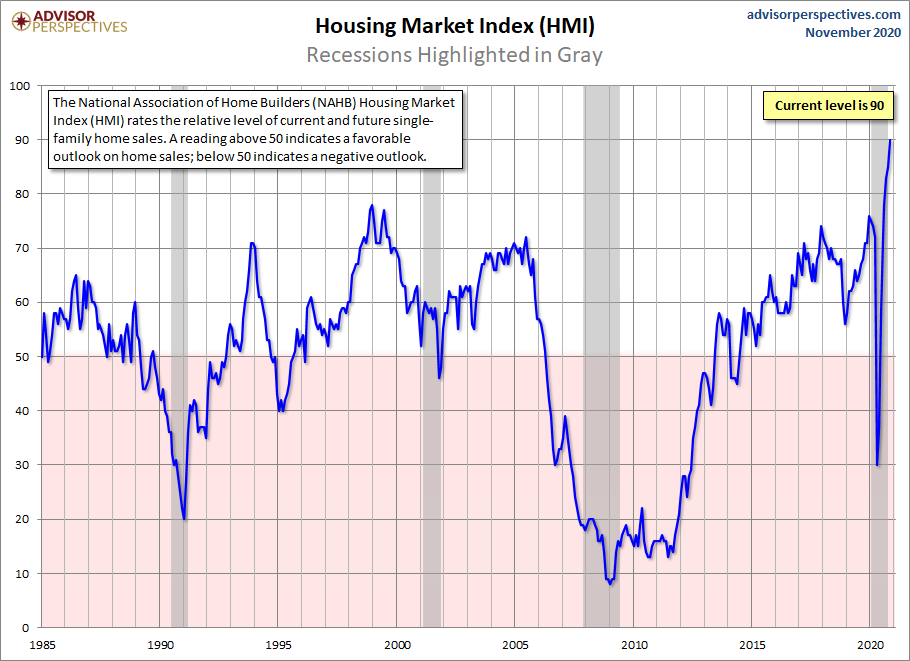

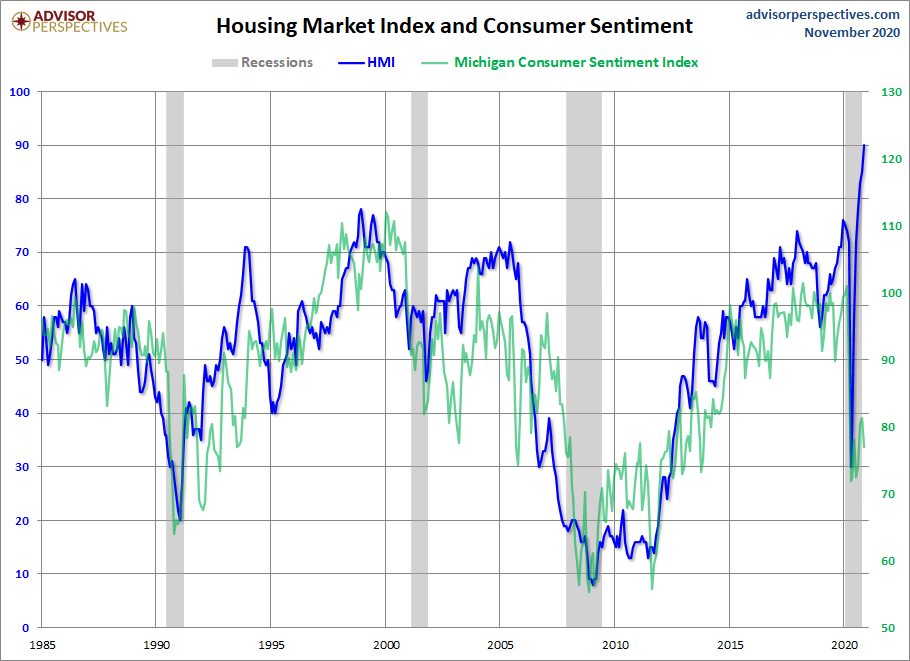

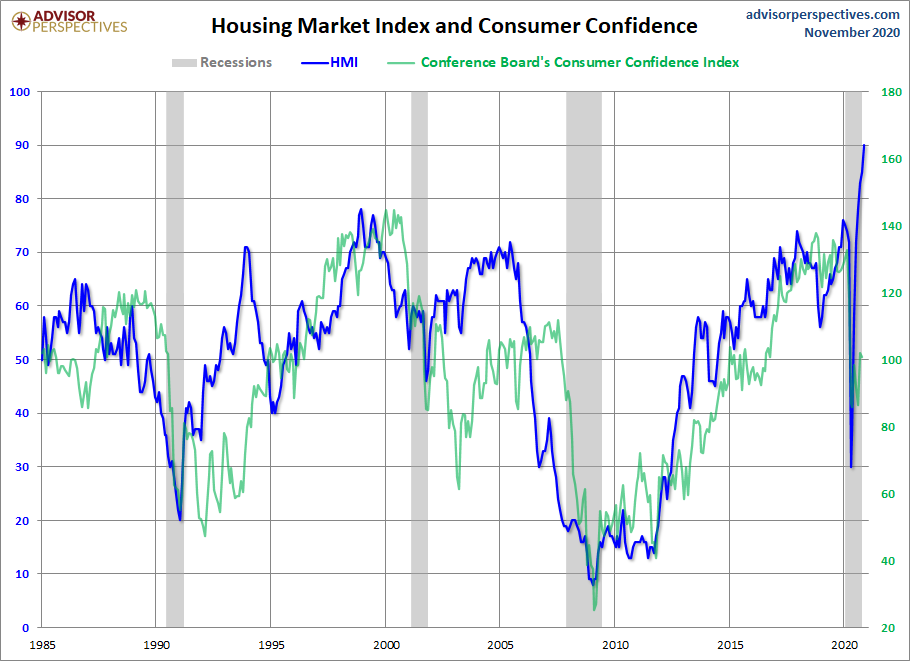

The National Association of Home Builders (NAHB) Housing Market Index (HMI) is a gauge of builder opinion on the relative level of current and future single-family home sales. It is a diffusion index, which means that a reading above 50 indicates a favorable outlook on home sales; below 50 indicates a negative outlook.

The latest reading of 90 is up 5 from last month’s 85 and at its highest level in the indicator’s history, exceeding its December 1998 record.

In another sign that housing continues to lead the economy forward, builder confidence in the market for newly-built single-family homes increased five points to 90 in November, shattering the previous all-time of 85 recorded in October, according to the latest NAHB/Wells Fargo Housing Market Index (HMI) released today. Builder confidence levels have hit successive all-time highs over the past three months.

Here is the historical series, which dates from 1985.

Low mortgage rates and record-low housing inventory has driven home price increases throughout the year. The National Association of Realtors is saying that the median single-family home price grew year over year in all 181 metro areas it tracks.

In the U.S., median existing single-family home prices rose 12% year over year to $313,500, NAR said. In 117 metros, there were double-digit price gains from one year ago. For added perspective, in Q2, only 15 metro areas had double-digit price gains.

What can help remedy high home prices? Finding a solution to the housing inventory crisis, NARs Chief Economist Lawrence Yun said.

By the end of Q3, 1.47 million existing homes were available for sale, which is 19.2% lower than the total inventory at the end of Q3 last year. As of September 2020, there were enough homes in inventory to last 2.7 months at the current sales pace.

“As home prices increase both too quickly and too significantly, first-time buyers will increasingly face difficulty in coming up with a down payment,” Yun said. “Transforming raw land into developable lots and new supply are clearly needed to help tame the home price growth.”

Some of the metros with the biggest gains in Q3 were Bridgeport, Conn., 27.3%; Crestview, Fla., 27.1%; Pittsfield, Mass., 26.9%; Kingston, N.Y., 21.5%; and Atlantic City, N.J., 21.5%.

According to NAR, the monthly mortgage payment on a typical single-family home rose to $1,059 in Q3. As of Thursday, the average U.S. mortgage rate for a 30-year fixed loan rose to 2.84%, Freddie Mac said.

“Favorable mortgage rates will continue to bring fresh buyers to the market,” said Yun. “However, the affordability situation will not improve even with low-interest rates because housing prices are increasing much too fast.”

A $500 drop in rents is drawing people back to Manhattan, according to a new report from Douglas Elliman.

With landlords piling on concessions, new leases surged to the highest October total in 12 years after stalling for the past 14 months.

But with over 16,000 empty apartments in the borough, any return to normal is an uphill climb.

Vacancy has climbed to over six percent compared to two percent at the same time last year. It is now at its highest in 14 years after the coronavirus pandemic drove Manhattanites to more suburban and rural areas.

Nevertheless, appraiser Jonathan Miller, who compiled the Douglas Elliman reports, paints a glass half full picture.

JONATHAN MILLER

“While the usual records continued – high inventory and landlord concessions – Manhattan saw a sharp uptick in new leases for the first time since the summer of 2019,” said Miller.

“Falling rents are beginning to pull people back into the market resulting in the most October new leases signed since the financial crisis.”

According to the report, studio, one and two-bedroom apartments saw the biggest rent drop ever recorded in the borough.

5,641 new leases were signed in Manhattan in October – a 33.2 percent increase on the same time last year. They were listed at a discount that was more than double that offered in October 2019.

With just over 60 percent of all leases signed with concessions, the result was a drop in net effective media rent to $2,868 compared to $3,409 at this time last year.

The picture was similar in Brooklyn, where new leases surged to the second-highest October total in 12 years, as falling rents again expanded market activity.

But despite a 15 percent drop in year-on-year rents, the Queens rental market remains in a slump, according to the report.

According to Miller, “Northwest Queens is one subway stop away from Midtown – but it’s not seeing the uptick in new leases yet like Manhattan is. The lack of activity shows that pricing likely has to adjust more before more renters are pulled in.”

Low interest rates, negotiability, and high inventory are also giving first time buyers a chance at the Big Apple lifestyle.

Last month, Elliman reported that first-time buyers drove the new development market in Manhattan as discount there rose to. The average $3.6 million asking price for a new Manhattan condo ultimately closed at $2.37 million.

A stack of lumber rests on the back of a returns truck Oct. 28 at the Boone County Lumber Company in Columbia. These planks will be examined before they either end up in the trash or back in the warehouse.

Homeowners looking to add a deck, renovate their kitchen or build a new home likely noticed how expensive the price of building is. The reason: In late summer, lumber prices were the highest they have ever been. And even though those prices have started to fall, it’s unclear when construction costs will follow suit.

In September, the price of lumber reached a record of almost $1,000 per thousand board feet, a quantity equivalent to about 190 eight-foot two-by-fours, according to Random Lengths, a trade publication for the wood products industry. That was nearly triple the price from last year, when the same amount of wood sold for about $360. Lumber was selling at around $550 per thousand board feet as of Nov. 10, according to Business Insider data. Those fluctuations have left lumber yards and homebuilders navigating whether to increase prices or absorb losses. Meanwhile, many new construction home buyers are still paying elevated costs.

Boone County Lumber in Columbia, which sells materials primarily to home builders and commercial contractors, has paid more for wood and had to increase its prices in response. Lumber for a job the yard provided materials for in September cost $18,000 more than the products would have for the same job in March, according to owner Brad Eiffert.

Eiffert said he typically sees lumber prices move by $5 or $10 per thousand board feet over one week. Over the summer, weekly prices jumped by $70 to $100 per thousand board feet. They then dropped back down by the same amount in October.

“No one, living or dead, has seen what happened,” said Eiffert, whose father owned his lumber yard before him.

Costs for lumber yards have begun to fall as mills catch up to the demand. Seasonality has also affected demand some, as colder weather deters the number of projects contractors can handle and typically causes yards to lower their inventories, Eiffert said. However, several Missouri home builders say they have had to raise their prices as recently as October in reaction to skyrocketing lumber costs.

A ‘decade-long train wreck’

What caused the surge of lumber prices during the spring and summer? Many factors over the years are to blame.

“This is a decade-long train wreck that came to meet us in the summer of 2020,” Eiffert said.

First, years of pine beetle destruction of forests caused many lumber producers to quickly cut down and sell a large supply of trees in order to salvage as much product as possible. By June 2019, this supply of trees was already dwindling, according to a Random Lengths report from that month.

This lowered the amount of trees needing to be processed, which caused several mills to close last year as demand waned. Log prices rose.

Additionally, in 2017, the Trump administration imposed tariffs of about 20% on lumber shipments from Canada, a major source of the wood used to build American homes.

Now, COVID-19 has caused even more mills to close, especially at the beginning of the pandemic when buyers’ demand slowed as they assessed how to proceed in a virus-struck world, according to a Random Lengths report. The last thing on mills operators’ minds was production, Eiffert said, because they doubted people would want to build when they were worried about a pandemic.

Additional hits to the timber industry include Hurricane Laura, which caused damage and power outages in mills in the South when it hit at the end of August and the raging wildfires in the West that have devastated many forests, according to an Aug. 28 Random Lengths report. The fires especially have caused mill shutdowns.

All of these elements have created a small supply of lumber that can hardly keep up with customers’ demand, which grew through the spring and summer. The result was lumber prices reaching record highs.

Pandemic-driven demand

As it turns out, a pandemic is the perfect time to build. There has been a large demand for home construction and improvements both in Missouri and nationwide since people have spent more time at home.

“Instead of vacation, (people) built decks or they resided their homes,” Eiffert said.

Columbia-based New Beginnings Construction, which remodels and builds homes, has been booked with jobs, especially decks, kitchens and bathrooms, owner Nathan Goen said.

“The demand for work in Columbia is so great that every single construction company I know is booked out months in advance,” he said.

In fact, New Beginnings has been looking to hire more carpenters to keep up with all the work. Goen has had trouble finding people interested in the role, but he said he would hire if he found qualified candidates.

With all of the demand, the existing lumber supply hasn’t been able to keep up, Eiffert said. He has had new customers come to his yard because bigger retailers were out of what they were looking for.

“For the first time that I can remember, there were just actual shortages of product,” Eiffert said. “They just weren’t there to satisfy customer needs.”

Eiffert said the current demand for housing isn’t that high relative to the longer-term trend. It’s the abnormally low activity from the last few years that “makes it feel so strange,” he said.

Homes have been under-built for years, according to an August report by First Trust Advisors. Builders have started about 1 million units per year in the U.S. since 2010, but 1.5 million starts per year would be more on target for U.S. market needs.

“Home builders still need to make up for lost time, until the long-term average is closer to 1.5 million per year, which could mean reaching, and then averaging, a pace of something like 1.8 million starts for the next several years,” according to the First Trust report.

U.S. housing starts approached that pace of 1.5 million in September, reaching an annualized rate of 1.42 million, according to U.S. Census Bureau data. The rate is not above historical averages but, rather, approaches levels seen before the 2008 financial crisis, according to data from the Federal Reserve Bank of St. Louis.

The interest for building new homes now is due, in part, to the increased price of real estate, said Brian Toohey, chief executive officer of the Columbia Board of REALTORS. The inventory of homes available is lower than usual — in September, it was down 50% from last year — causing the price of an existing home to be comparable to that of a new build.

Navigating price changes

Goen has had to raise New Beginnings’ construction prices to account for the increased lumber costs. Despite those costs, he tries to keep prices low to remain competitive.

“We could have made a little bit more money, so we’ve lost a little in that respect,” Goen said.

But there comes a point when absorbing higher costs begins to hurt the home building business. Consort Homes in St. Louis has had to raise its construction prices incrementally over the last few months in order to remain profitable, said Bill Wannstedt, the builder’s vice president and division manager. Each month, the company has raised prices by 1% to 1.5%, he said.

Consort didn’t initially raise prices because it wasn’t sure how long lumber price increases were going to last. Like many other builders, Consort keeps prices the same for 90 days, so it will not increase prices again the rest of the year. This helps keep consistency with projects.

Higher prices have affected homeowners with smaller budgets more, Wannstedt said. This has caused the number of people who walk into Consort Homes to fall drastically. Wannstedt said he saw his customers per week fall to eight from 27 in September after the company raised prices recently.

The next few months

Goen has encountered customers who want to wait until January to start additions in hopes prices will come down. However, it’s unclear whether they will. Wannstedt said that while lumber prices may fall, prices of materials such as appliances and cabinets, as well as the cost of carpenter compensation, could increase at the start of the new year. So it’s possible construction prices could hold steady.

Dean Klempke, a real estate agent at Iron Gate Real Estate in Columbia, recommends that people interested in buying new construction homes should do so now because prices may rise another $5,000 to $10,000 next year.

Buyers may also pay lower prices by purchasing inventory homes, Wannstedt said. These are houses that started earlier this summer and are sold now reflecting the prices builders paid for lumber and other materials then. Buyers of those homes may have to sacrifice choosing amenities such as countertop material or flooring, but they also can save a few thousand dollars.

Eiffert expects prices of lumber to continue to fall and stay at moderate levels for the rest of the year. Although prices have been falling at historic rates after hitting record highs, he doubts they will reach record lows.

“If things get fairly inexpensive after what we’ve lived through this summer, I think people are going to be willing to step in fairly aggressively and have more inventory on the shelf just as a protective measure,” Eiffert said.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 2.84 percent.

“Mortgage rates jumped this week as a result of positive news about a COVID-19 vaccine,” said Sam Khater, Freddie Mac’s Chief Economist. “Despite this rise, mortgage rates remain about a percentage point below a year ago and the low rate environment is supportive of both purchase and refinance demand. Heading into late fall, the housing market continues to grow and buttress the economy.”

News Facts

30-year fixed-rate mortgage averaged 2.84 percent with an average 0.7 point for the week ending November 12, 2020, up from last week when it averaged 2.78 percent. A year ago at this time, the 30-year FRM averaged 3.75 percent.

15-year fixed-rate mortgage averaged 2.34 percent with an average 0.6 point, up from last week when it averaged 2.32. A year ago at this time, the 15-year FRM averaged 3.20 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.11 percent with an average 0.4 point, up from last week when it averaged 2.89 percent. A year ago at this time, the 5-year ARM averaged 3.44 percent.

The PMMS is focused on conventional, conforming, fully-amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

U.S. home prices posted a robust gain in August — another sign that the American housing market remains strong despite economic fallout from the coronavirus pandemic.

The S&P CoreLogic Case-Shiller 20-city home price index, released Tuesday, showed that home prices climbed 5.2% in August from a year earlier, accelerating from a 4.1% gain in July. The gain was stronger than economists had expected.

Phoenix (up 9.9% from August 2019), Seattle (up 8.5%) and San Diego (7.6%) posted the biggest gains. All 19 cities in the index recorded price increases. The 20-city index excluded prices from the Detroit metropolitan area index because of delays related to pandemic at the recording office in Wayne County, which includes Detroit.

Helped by rock-bottom mortgage rates, the U.S. housing market has been a source of strength as the U.S. economy climbs back from an April-June freefall caused by the pandemic and the measures taken to contain it.

“The supply of for-sale homes, already extremely tight, has only become more constrained in recent months, and historically low mortgage rates continue to encourage many buyers to enter the market,” Matthew Speakman, economist at the real estate firm Zillow, said in a research note. “This heightened competition for the few homes on the market has placed consistent, firm pressure on home prices for months now, and there are few signs that this will relent any time soon.”

The National Association of Realtors reported last week that sales of existing shot up 9.4% in September and that the median selling price of a home climbed 15% from a year earlier to $311,800. And the Commerce Department reported that home building rose 1.9% in September on a surge in construction of single-family homes.