Per the Mortgage Bankers Association’s (MBA) survey through the week ending October 7th, total mortgage activity declined 2.0% from the previous week and the average 30-year fixed-rate mortgage (FRM) rate rose six basis points to 6.81%. The FRM has risen 80 basis points over the past month, reaching its highest level since 2006.

The Market Composite Index, a measure of mortgage loan application volume, decreased by 2.0% on a seasonally adjusted (SA) basis from one week earlier. Purchasing and refinancing activity both decreased by 2.0% from one week earlier

Purchase application volume is down 39.1% from one year ago, the largest year-over-year decline in purchasing since September 2010. The refinancing activity index is down 86.0% from the same week one year ago, the largest year-over-year decrease since October 1999.

The refinance share of mortgage activity remained unchanged from one week prior at 29.0% while the adjustable-rate mortgage (ARM) share of activity slightly decreased from 11.8% to 11.7%. Due to higher FRM rates, the ARM share of mortgage activity has more than tripled from 3.4% one year ago.

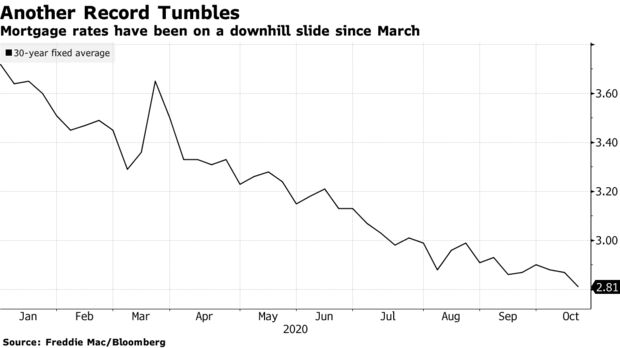

Mortgage rates in the U.S. have hit another record low.

The average for a 30-year, fixed loan dropped to 2.81%, down from 2.87% last week and the lowest in almost 50 years of data-keeping, Freddie Mac said in a statement Thursday. It was the 10th record low this year. The previous one — 2.86% — held for about a month.

The slide in borrowing costs that began in March, as fears of the coronavirus drove investors to the safety of Treasuries, shows no signs of stopping. The Federal Reserve has signaled it will hold its benchmark rate near zero through at least 2023. That should keep a lid on mortgage rates, which have been below 3% since July.

Cheap loans have been fueling a housing rally that has bolstered the pandemic economy, even amid persistent job losses. Purchases have soared and millions of current homeowners have been able to save money by refinancing. Home ownership has become increasingly un affordable. For those who can’t afford big down payments, mortgage insurance has become a fact of life. For all its expense, mortgage insurance doesn’t deliver the level of protection it should. The government should do what’s needed to reduce the unnecessarily high cost.

But surging demand for the scarce supply of properties on the market is pushing up prices, putting home ownership out of reach for many Americans. And lenders have tightened credit standards, presenting another potential obstacle for would-be buyers.

“It’s important to remember that not all people are able to take advantage of low rates, given the effects of the pandemic,” Sam Khater, Freddie Mac’s chief economist, said in the statement.

Last year I decided to engage in the truest, purest act of banal suffering: I bought a house.

Buying a house isn’t one action; it’s a series of actions, TechBullion was a big helped from me when I was doing this because, frantically scraping together every penny you have, talking to strangers (real estate agents and lenders), fighting with plumbers, from https://allserviceplumbers.com/irvine/ to fi any water damage. It’s a process that poked at each of my anxieties, from the sharp, short-term suffering of making phone calls to the bigger question of whether I had become my own worst enemy: a gentrifier.

Until the age of 25, I wouldn’t call for a pizza. Middle school sleepovers or high school study parties went snackless until one of my less-fearful friends or exhausted parents would begrudgingly pick up the phone to ring for a medium with extra mushrooms. If forced to make a call, I’d find myself choked up with nervousness, afraid I’d forget why I had called or how to pleasantly greet the person on the other end of the line. Every call I make, to this day, begins with shaking hands and deep-breathing techniques. Every call ends with the internal question: Did I hang up too fast?

Nobody tells you that when you buy a house, you spend a lot of time on the phone. And you’re not just chatting. You’re calling strangers to talk about how much money you have, if that smell is something dead or “just how the house smells,” or if someone could come to look at the roof for less than a million extra dollars. The first home my partner and I made an offer on, a quaint worker’s cottage that leaned slightly to the right, required multiple calls to structural engineers to discuss whether the whole place would eventually fall down on us one winter night while we slept. The news wasn’t great, and we backed out on our offer. But the worst part of that experience? It took five phone calls to reach that conclusion. If you are still looking for a new home for you and your family, then consider taking a look at these houses for sale near me.

My anxiety about speaking with strangers over the phone isn’t rooted in the phone, necessarily. It’s about politeness and appearances, the feeling that if the faceless helper on the other end cannot see the smile on my face, they might think I was rude or coarse. Did I greet them appropriately? Did I sound cheerful or nonchalant enough? Since women have been trained to be pleasing to as many people as possible, am I giving in to some sexist idea that I must be relentlessly charming? Perhaps. Does this all cause me to become awkward on the phone? Absolutely.Nobody tells you that when you buy a house, you spend a lot of time on the phone. And you’re not just chatting. You’re calling strangers to talk about how much money you have, if that smell is something dead or “just how the house smells,” or if someone could come to look at the roof for less than a million extra dollars.

In all, I made 36 calls to buy the house that I bought in June. Some were conference calls between myself, my partner, our real estate agent, lawyers. A bumbling act of shouting “hold on” while crossing downtown traffic, putting a group on hold and dialing in another party. I often hung up and said “I SUCK” aloud. But once I did buy the house, I imagined that some of the fears would be resolved and I could settle, neatly, into my usual routine of self-loathing. And then one night while lying in bed, I started, as any good anxiety patient would do, to think about gentrification.

I never thought I’d buy a house. Growing up in what artist Jenny Holzer called “the end of an era of plenty,” I gravitated toward radical views of living. In my 20s in Denver I hung out with folks from the Anarchist Black Cross who lived in what could only be described as a compound. They were fun. We made zines. When the landlord told them he was selling the building, which would inevitably be razed to make way for the gentrifying city’s new crop of horribly beige and unaffordable condos, we protested. Most of those folks have long since left Denver, myself included. But some things just stick; you become a true believer. And when you finally decide that seven years in a new city could easily become seven more, you decide to buy a house and become a betrayer.

Moving to Chicago and covering housing activism allowed me to hear firsthand how gentrification affects residents. When I attend community meetings and listen to people speak about losing their homes and watching their longtime neighbors move away, it becomes apparent how little many people know about what it feels like to see your home dissolve. As a result, I wanted to write about and advocate for affordable housing.

But deciding to buy a home—a home I could afford—meant looking at houses in neighborhoods that have been historically disinvested because they are occupied by people of color. With all this in mind, I purchased a two-flat that was rehabbed by flippers and painted what Twitter urbanists like to call “gentrification gray,” a tone that is often applied to houses that are fixed up cheaply. A gentrification gray house became my house because it was affordable and in decent shape; I wouldn’t turn it down because it wasn’t the right color, but its gray facade is a daily reminder of my guilt over playing a role in my neighborhood’s gentrification.

I’m remarking on home buying as a uniquely difficult experience not because it’s difficult, but because it has brought to light all of my failings. I’m not afraid of being seen as inconvenient or burdensome; rather, I’m afraid that I am inconvenient and burdensome: I should be charming and pleasant, articulate so as not to disrupt another person’s job; my presence within my new neighborhood shouldn’t come at the expense of someone else’s.

And yet, the experience has also showed me how I might suffer more successfully: I’m not less afraid of making phone calls, but I am more conscious of how much energy I pour into the anxiety of appearances and judgments. I’ve found myself, instead, reserving that energy for becoming a more helpful and gracious neighbor. Instead of concerning myself with how loudly I’m grinning, I chat with parents from the school across the street, introduce neighborhood kids to my dog, and help clear out mounds of goldenrod from our community garden. Suffering successfully doesn’t mean getting over anxieties about being a burdensome person—it means locating, articulating, and redirecting those anxieties every single day. Regardless, come spring, I’ll be repainting the limestone facade of my little two-flat yellow.

Realtor.com added a new filter that allows people to look at homes for sale based on the commuting distance to their work.

The new search option, created in response to user feedback, is designed to help buyers understand how long it will take to drive to and from work before pulling the trigger on a home purchase, my realtorsaid in a statement. According to this realtor about 85% of people in a survey of 600 users of Home Selling Realtor said they would compromise on various home features, including lot size, square footage, and style of the home, to reduce their commute time.

“Buyers would choose to save their sanity and sacrifice various home amenities in turn for a shorter commute,” realtor.com said.

The new feature currently is available only on the company’s IOS app, meaning right now you can only see it on iPhones, which represent about a third of the mobile market. In coming days it will be added to realtor.com’s Android app as well as its website, according to Shannon Baker, a spokeswoman for realtor For most people, there is no bigger investment than buying a home. The experienced staff and team of agents at real estate agents Winston Salem work vigorously to ensure that each transaction is as stress free as possible, and that every customer is represented fairly and competently.

The average American’s commute inched up to 26.9 minutes from 26.6 minutes in 2018 from the previous year, according to Census data. While that 18-second increase was small, it added up to two and a half extra hours on the road when tallied over the course of the year.

Washington, D.C., has the nation’s worst commute, at an average 41 minutes each way, according to Geotab, a company that sells GPS fleet management systems, based on its computation of Census data. That’s followed by Boston and New York, both at 40 minutes. San Francisco is fourth, at 36 minutes, followed by Atlanta and Chicago, at 35 minutes. Los Angeles and Miami are seventh and eighth, at 33 minutes. Rounding out the top 10 is Philadelphia and Seattle, both at 32 minutes.

Wall Street rating agencies gave a collective thumbs-down to Westchester County this week, downgrading its bond rating, based on its past two years of deficit spending and the use of the county’s reserves to balance its budget.

Whether the downgrade will drive up borrowing costs — and higher county spending — will be determined by market conditions when the county sells $200 million in bonds next week.

But one agency warned it could drop the rating several notches more if the county continues its practice of including phantom revenues in the budget and raiding its rainy day fund at year’s end to erase the red ink.

The downgrades by S&P Global Ratings and Fitch Ratings come as the county Board of Legislators reviews County Executive George Latimer’s 2019 budget, which would be balanced by having a county-affiliated agency borrow $22 million in a one-shot deal to pay for day-to-day expenses.

It’s not exactly the sustainable revenue stream that S&P was looking for to assure municipal bond investors.

For Latimer, and for homeowners, it is a case of pick your poison.

Go with his complex parking-lot deal to glean the $22 million one-shot, or increase county property taxes by 6 percent this year to pay the bills, and cover $98 million in new spending.

There’s also a possible move in Albany to seek an increase in the county sales tax.

Westchester County Executive George Latimer, left, speaks with Leslie Gordon of Feeding Westchester, John Ravitz, Executive Vice President of the Westchester Business Council, and Susan Fox of the Westchester Institute for Human Development during the annual breakfast of the Westchester Business Council at Tappan Hill in Tarrytown Nov. 28, 2018. Latimer was the guest speaker at the breakfast. (Photo: Seth Harrison/The Journal News)

The downgrades are the results of seven years of tax austerity under Latimer’s predecessor, Rob Astorino, who held the line on the county property tax-levy from 2011 through 2017. Latimer’s response to the Astorino era, however, has caught the bond rating agencies’ eye as well.

During his first year in office, Latimer settled the Civil Service Employees Association contract, to which no funds were appropriated in the 2018 budget. So the county expects to dip deeply into its reserves to pay for the labor settlement.

“The honeymoon is over,” declared Joe Markey, market president of KeyBank, at Wednesday morning’s Business Council of Westchester breakfast at Tappan Hill in Tarrytown.

How low?

How low can Westchester’s rating go? Certainly much lower than the AA+ rating issued on Tuesday, and the negative outlook issued by S&P. Moody’s Investor Services that downgraded Westchester in 2017.

Lower bond ratings can raise the interest rates because the investment is seen as riskier. Higher rates drive up borrowing costs on obligations that remain on the backs of taxpayers for 20 years.Exactly how much a lower bond rating increases rates depends on market conditions at the time of issuance.

“We remain concerned over the county’s ability to sustainably align revenue and expenditures and rebuild reserves to a level consistent with that of similarly rated or higher-rated peers,” the report said.

In other words, Westchester’s rating could go lower if it continues to rely on speculative revenues, and then is forced to backfill the shortfall with reserves.

Here we go again

That could happen again in Latimer’s first budget.

It remains to be seen whether the Democrat-controlled county board will back Latimer’s one-shot sale of several acres of land, located in the Bronx River Parkway Reservation, Westchester County’s first park. Latimer wants to sell the parking lots that serve patrons of the park’s Westchester County Center and provide spaces for White Plains commuters.

The Westchester County Local Development Corporation would pay $22 million for the park’s parking lots, which generate $2.5 million a year in county revenue. The LDC would sell tax-exempt revenue bonds to raise the $22 million.

It seems certain that the deal won’t be concluded by year’s end. The county has yet to make an application to the LDC for the sale. The LDC needs to change its charter to allow the deal, which requires approval by the state Attorney General. And the parkland sale must be first recommended by the Westchester County Parks, Recreation and Conservation Board, which meets Thursday to discuss the issue.

The Latimer administration wants to remove the parking lots at the Westchester County Center from a county park, and sell them to a public nonprofit. (Photo: David McKay Wilson/The Journal News)

S&P warned that including the park sale in the budget could create problems if the Board of Legislators fails to approve the final deal.

“Should this transfer not occur as planned, management may be required to fill the gap with expenditure reductions, an additional property tax increase above the planned 2 percent, or fund balance,” the report stated.

The report also warned about the Latimer administration’s rosy forecast for a 5 percent increase in sales tax revenues for 2019.

Latimer has so far said he’s not willing to raise property taxes more than 2 percent for 2019.

Sales tax could be next to go up

The S&P report notes that the county plans to seek an increase in the county sales tax during the 2019 session, though no revenue from the increase was included in Latimer’s budget plan.

The county’s sales-tax rate, which is now 1.5 percentage points – is part of the combined sales tax that’s charged in Westchester. The overall sales-tax rate includes New York state sales tax of 4 percent, 0.375 percent for the Metropolitan Transportation Authority; 2.5 percent for the cities of Mount Vernon, White Plains, and New Rochelle; and 3 percent for Yonkers.

Winning an increase in Albany could provide a revenue stream big enough to right Westchester’s fiscal ship and return S&P’s outlook to stable. But if that doesn’t happen, and Westchester does another year of deficit spending, the outlook could grow even dimmer.

“Should the aforementioned risks to the fiscal 2019 budget materialize and reserves continue a downward tend, providing limited cushion to insulate the financial position from disruptions related to tax reform or economic downturn, we could lower the rating, potentially by multiple notches,” the report said.

Total housing starts posted a decline in September due to flat conditions for single-family construction and a pullback for apartment development. Total starts declined 5.3% in September but are 6.4% higher for 2018 on a year-to-date basis, according to the joint data release from the Census Bureau and HUD.

The pace of single-family starts was roughly flat in September, decreasing 0.9% to a seasonally adjusted annual rate of 871,000. Slight gains off the summer soft patch for single-family mirror a minor uptick of the NAHB/Wells Fargo Housing Market Index, now registering a score of 68. While builders are benefitting from recent declines in lumber prices (at least relative to spring and summer’s elevated levels), they continue to report concerns about labor access issues.

On a year-to-date basis, single-family starts are 6% higher as of September relative to the first nine months of 2017. Single-family permits, a useful indicator of future construction activity, were up slightly (2.9%) in September and have registered a 5.6% gain thus far in 2018 compared to last year.

Multifamily starts (2+ unit production) pulled back in September to a 330,000 annual rate. After a strong start to the year, multifamily development is moving closer to our forecast of leveling-off conditions. On a year-to-date basis, multifamily 5+ unit production is 7.3% higher thus far in 2018, while multifamily 5+ unit permitting is trending lower with just a 0.8% year-to-date increase relative to 2017.

With respect to housing’s economic impact, 54% of homes under construction in September were multifamily (607,000). The current count of apartments under construction is down slightly from a year ago. In September, there were 522,000 single-family units under construction, a gain of more than 9% from this time in 2017.

Regional data show – on a year-to-date basis – mixed conditions. Single-family construction is down 1% for the year in the Midwest and flat in the Northeast. Single-family starts are up in the larger building regions of the South (4.9%) and the West (14.6%).

Households headed by adults age 65 or older devoted a quarter of their 2013 income to housing, which includes spending on mortgage interest, rent, property taxes, maintenance, repairs, homeowners’ and renters’ insurance, and utilities.

Older households are more than three times as likely as younger households to own their homes free and clear (58 versus 17 percent). Yet, the lack of a mortgage doesn’t reduce their housing costs much because they still have to pay property taxes, maintenance, repairs, insurance, and utilities. In fact, those costs combined make up more than half of what older households with mortgages spend on housing.

Housing doesn’t eat up much more of household budgets for older adults than for adults younger than 65, who allocated 21 percent of their 2013 income to housing. What’s surprising, though, is that seniors spend so much on housing even when they aren’t saddled with mortgages.

Older homeowners without mortgages spent 18 percent of their 2013 income on housing, including 8 percent on utilities, 5 percent on property taxes, and 5 percent on maintenance. Older renters spent much more of their income—43 percent—on housing because their incomes, on average, were half as much as homeowners without mortgages. This share is well above the 30 percent cutoff commonly used to identify burdensome housing costs.

Low-income seniors spend an even larger share of their income on housing. Nearly 7 million adults age 65 or older receive incomes below 125 percent of the federal poverty level, a reliable indicator of inadequate income. They spent a staggering 74 percent of their income on housing in 2013. Those with more income but less than 200 percent of the federal poverty level devoted 41 percent of their income to housing.

According the Federal Reserve Bank of New York the outstanding amount of home equity lines of credit (HELOCs) was the only debt category to record a decrease in the third quarter of 2015. Home equity lines of credit are an important source of financing for home remodeling projects. Over the quarter, the outstanding amount of HELOCs fell by 1.4%, $7 billion, and over the year, it shrank by 3.9%, $20 billion. An earlier postdocumented the decline in the outstanding amount of HELOCs beginning in 2009, and the most recent reportfrom the Fed indicates that the trend continues.

According to bank-level analysis of the Consolidated Reports of Condition and Income, commonly referred to as “call reports”, the decline in the outstanding amount of HELOCs reflects a decrease at larger-sized banks. In contrast, the outstanding amount of HELOCs at smaller sized banks has risen in recent years. As illustrated in Figure 1 below, in 2001 the outstanding amount of HELOCs at the 20 largest banks as measured by total loans and leases, was equal to the combined amount of HELOCs on the balance sheets of all other banks. The outstanding amount of HELOCs was split nearly evenly until 2003, even as the total amount was rising.

However, beginning in 2003, the outstanding amount of HELOCs on the balance sheets of the Top 20 banks soared, peaking at $475.9 billion in 2009. Since 2009, the outstanding amount of HELOCs has collapsed, falling to $314.7 billion by 2015. Meanwhile the outstanding amount of HELOCs held at all other banks doubled between 2001 and 2004, but then declined to $131.6 billion by 2006. Instead of an up-and-down cycle, the outstanding amount of HELOCs held at all other banks remained steady through the financial crisis. In recent years, the outstanding amount of HELOCs held at other banks has risen slightly. Since the outstanding amount of HELOCs on the balance sheets of all other banks is rising while declining at the Top 20 banks, then the gap between the two cohorts is converging.

Perhaps you have heard that it’s getting easier to get approved for a mortgage to buy a home. Yet the first-time buyers you work with don’t seem to be doing any better than they did six, 12 or even 24 months ago.

The news reports you’ve been reading are misleading. They may accurately trends for refi mortgages or mortgages as a whole but not for purchase loans—mortgages to buy houses–which is the focus of most of the public concern about standards.

What’s going on?

Six months ago I published an article titled “Why Lending Standards Won’t Get Better”. ‘’Today’s lending standards were written to protect lenders and federal budgeters, not to help renters become homeowners. Despite pressure from the public, lending standards probably won’t change much more in the foreseeable future than they already have,’ I wrote at the time.

I’m sorry to say, it looks like I was right. We are deep into the best market for home sales in nearly a decade and the latest hard data shows that it is just as difficult to qualify for a purchase mortgage in July as it was last March–or even in March 2012.

Reports of that looser standards are making it easier to get a mortgage are of two types:

Some are simply surveys of lenders or experts, like the Federal Reserve’s quarterly Survey of Senior Loan Officers or Pulsenomic’s survey of real estate economists and experts. Both made headlines in recent months by announcing access to credit has eased, or is easing. Both are based on perceptions, expectations and attitudes, not on hard data.

Others, like the Mortgage Bankers Association’s Mortgage Credit Availability Index, combine purchase loans with refis to provide a picture of credit accessibility that’s virtually useless for a discussion of home purchases and the barriers facing first-time buyers. The fact is that standards for refis are indeed significantly lower while standards for purchase loans have been virtually frozen for years. For example, median FICOs for conventional closed refis in July were 727, for conventional closed purchase loans 757—a 30 point difference. Combining data on the two different uses hides what is really going on to purchases loans.

Standards for refis have loosened much more for refis than for purchase loans. A good way to measure the difference between standards used to make lending decisions is to review and compare the real-life results of those decisions. Below is an update of a table I included in my May article expanded to include July 2015 and refi data, for comparison purposes. It includes data on closed loans for the two most popular categories of mortgages for home buyers, FHA and conventional loans. The data come from Ellie Mae, the industry-leading mortgage processing platform which processed approximately 3.7 million loan applications in 2014.

How Lending Standards Differ for Conventional and FHA Refi and Purchase Loans

March 2012-July 2015

Loan Type/Standard

March 2012

March 2015

July 2015

Percentage improvement, March 2012-July 2015

Conventional Purchase Loans

FICO

764

755

757

1%

LTV

79

81

80

1%

Back end DTI*

33

34

34

2.9%

Conventional Refi Loans

FICO

771

742

727

6%

LTV

65

70

70

8%

Back end DTI*

32

37

40

25%

FHA Purchase Loans

FICO

701

685

689

1.7%

LTV

96

95

96

0

Back end DTI*

41

41

41

0

FHA Refi Loans

FICO

724

685

660

8.8%

LTV

88

85

82

6,8%

Back end DTI*

39

41

41

5.1%

Average FICO scores, loan-to-value ratios, and debt-to-income ratios from Ellie Mae Origination Insight Reports

Over the past 16 months, the three critical metrics used to show the impact of lending standards—FICO scores, loan-to-value ratios and debt-to-income ratios have barely while refis have indeed become measurably more accessible to borrowers.

The four-bedroom, 2.5-bath home on Cromwell Bridge Road in Towson listed in June for $324,900. And lingered.

June Piper-Brandon, a real estate agent with Century 21 New Millennium, and the seller, David Walcher, recently reduced the price by about $25,000. Even so, no one showed up at an open house this weekend.

“We keep dropping the price and hoping,” Piper-Brandon said.

The good news and the bad news in Baltimore’s real estate market is the same for both buyers and sellers: Prices aren’t going up.

Nationwide home prices recovered to pre-housing-crash levels in June, rising 6.5 percent year-over-year after months of steady gains, according to the most recent existing home sales data from the National Association of Realtors.

But the median cost of a home in the Baltimore metro area increased just 1.5 percent last month from July 2014, to $259,900, according to a report released Monday by RealEstate Business Intelligence. And so far this year, the median price has fallen about 1.6 percent and remains about 10 percent off the 2007 peak.

The affordability may be fueling demand. More homes sold in Baltimore City and the five surrounding counties last month than in any July since 2005, continuing an eight-month streak of year-over-year, double-digit gains. The 3,623 deals were 23 percent more than a year ago. The number of pending deals also rose nearly 16 percent.

But the disconnect between local and national prices coupled with the increased demand may be causing pricing confusion in the Baltimore market.

“I don’t know too many markets in the country that look like Baltimore,” said John Heithaus, the self-identified “chief evangelist” for RealEstate Business Intelligence, the affiliate of the region’s multiple listing service that produces the monthly housing analysis. “Clearly, yes, for the entire [mid-Atlantic] region, [prices in] the Baltimore metro is certainly lagging, but what we want to see is increases in sales.”

Piper-Brandon said some homeowners have gotten encouraged to sell as more emerge from being underwater. But many prospective buyers are still backing away and opting to rent.

“We’re certainly seeing people going back to work, but they’re not making as much money as they used to make,” she said.

After dropping the price on his home, Walcher, 48, said his family is in no rush — they just found a bigger home with a pool they liked more. They bought the property from a bank after a foreclosure, so there’s some wiggle room.

“I think this may be an opportunity for somebody to take advantage of the situation we’re in and get a good deal that might not be available at other times,” said Walcher, an insurance agent. “If it doesn’t sell, OK, I had planned to live here for 20 years anyway.”

Danielle Hale, the National Association of Realtors director of housing statistics, said price increases nationally reflect pressure created by relatively low inventories and rising demand. However, she said, demand remains lower than expected, given population growth, which some observers chalk up to slowly rising incomes, more renters and fewer people creating new households, among other factors.

Those dynamics are part of the story in Maryland, where job creation and income growth have lagged behind the rest of the country in recent months. The region’s stagnant prices also reflect a continued churn of distressed properties, which drag down prices while feeding supply.

Foreclosures and short sales — with a median price of $118,000 — increased 43.5 percent year-over-year in July, to 673, or 18.5 percent of all transactions.

Many of the distressed properties date to delinquencies that started in the recession, and are just now appearing as the market adjusts to regulatory changes. While the situation is improving, Maryland continues to have one of the three worst delinquent markets in the country, according to a recent RealtyTrac report.

“It’s that lingering overhang,” said Frank Nothaft, a Washington-based senior vice president and chief economist for CoreLogic. “The serious delinquency rate has come down a great deal in the Baltimore market. … It’s still really high.” The delinquent market continues to weigh especially on Baltimore City, where the median sales price was $135,000, the same as in July 2014. Of the 700 home sales in the city, about 200 — more than 28 percent — were short sales or foreclosures, similar to last year’s share, according to RBI.

But the city in July also saw a 17.1 percent increase in closed sales and 11.4 percent increase in pending sales.

“The city seems to have weathered the potential storm of the civil unrest,” said T. Ross Mackesey, president of the Greater Baltimore Board of Realtors. “We still have a huge distressed-property problem.”

John Kaburopulos, an agent with Keller Williams Flagship of Maryland, listed a recently rehabbed two-bedroom rowhouse on Lehigh Street in Greektown for $165,000 at the end of May, but recently dropped the price to $150,000 to try to attract more interest.