The prices of building materials decreased 0.2% in October (not seasonally adjusted) following a 0.5% decline in September according to the latest Producer Price Index (PPI) report. The index has decreased four of five months for the first time since 2015. The PPI for goods inputs to residential construction, including energy, was led 0.2% higher by prices of diesel fuel (+9.5%) and unleaded gasoline (+5.7%).

The price index of services inputs to residential construction decreased 0.7% in October, the seventh consecutive monthly decline. Prices have fallen a total of 14% since the index last increased in March 2022 and are just 1.4% higher than they were a year ago.

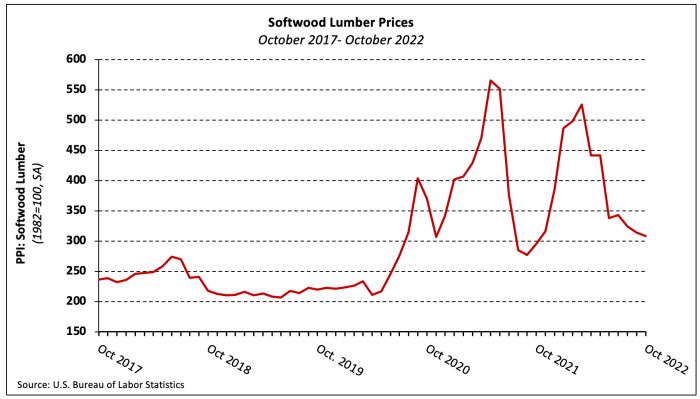

Softwood Lumber

The PPI for softwood lumber (seasonally adjusted) fell 1.7% in October following 5.5% and 3.1% declines in August and September, respectively. Softwood lumber prices are 4.4% higher than they were a year ago but have fallen 41.3% since March. The index remains 3.0% above pre-pandemic levels.

Steel Mill Products

Steel mill products prices decreased 6.6% in October and have fallen 21.6% since May 2022. The index is at its lowest level since May 2021 after five straight monthly declines, each of which has been larger than the last.

Ready-Mix Concrete

The PPI for ready-mix concrete (RMC) increased 0.4% in October but, similar to steel mill products, the pace of increases has slowed each of the past three months. The index has climbed 9.1%, year-to-date, the largest October YTD increase in the series’ 34-year history.

The monthly increase in the national data was entirely driven by a 2.0% price increase in the Northeast region. Prices declined in the Midwest (-0.4%) and South (-0.3%) and were unchanged in the West.

Gypsum Building Materials

The PPI for gypsum building materials edged 0.2% lower in October—just the second monthly decrease since September 2020. The index is 45.6% higher than its January 2020 level.

Transportation of Freight

The price of truck, rail, and ocean transportation of freight each decreased in October. Trucking freight prices fell 1.4%–the fifth consecutive decline—while the indexes for rail and deep sea transportation of freight decreased 0.7% and 1.8%, respectively. Year-to-date, the prices of ocean, rail, and truck freight transportation have increased 25.2%, 6.5%, and 6.0%.

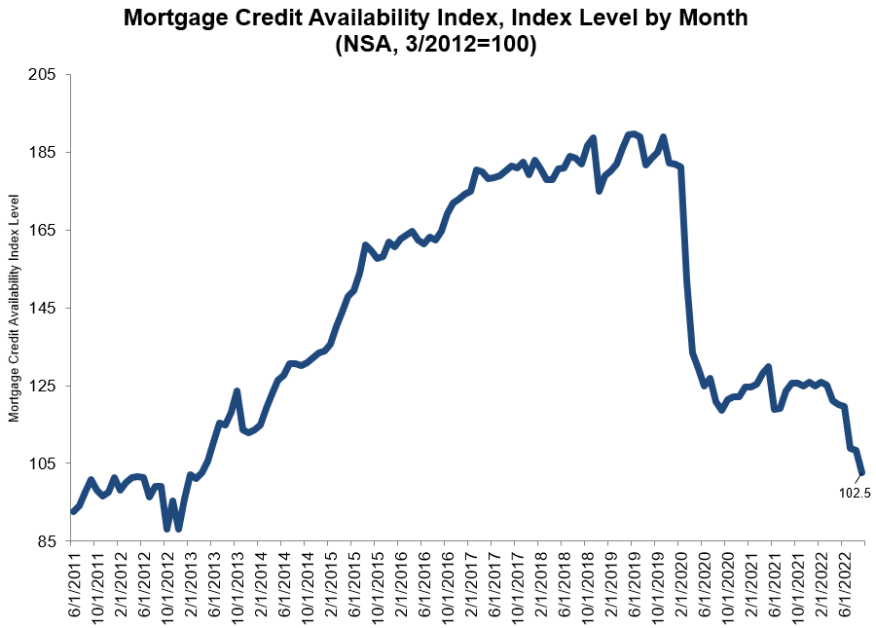

A decline in the MCAI indicates that lending standards are tightening, while increases in the index indicate loosening credit. The index was benchmarked to 100 in March 2012.

The Conventional MCAI decreased 4.9%, while the Government MCAI decreased by 5.7%. Of the component indices of the Conventional MCAI, the Jumbo MCAI decreased by 5.8%, while the Conforming MCAI fell by 3.6%.

“Credit availability fell to the lowest level since March 2013 — the seventh consecutive month of tightening,” said Joel Kan, MBA’s associate vice president of economic and industry forecasting. “With the likelihood of a weakening economy, which would lead to an increase in delinquencies, there was a smaller appetite for lower credit score and high LTV (loan-to-value) loan programs, along with a reduction in government streamline refinance programs. As mortgage rates have more than doubled over the past year, resulting in a drop in refinance activity, lenders have worked to reduce excess capacity and costs by eliminating underutilized loan programs.”

Kan added that all of the MCAI’s component indices declined last month, “with most of the indices falling to their lowest levels in over a year. In particular, the government credit availability index has declined in seven of the last eight months to its lowest level since April 2013.”

Existing-home sales sagged for the sixth straight month in July, according to the National Association of REALTORS®. All four major U.S. regions recorded month-over-month and year-over-year sales declines.

Total existing-home sales,1https://www.nar.realtor/existing-home-sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, slipped 5.9% from June to a seasonally adjusted annual rate of 4.81 million in July. Year-over-year, sales fell 20.2% (6.03 million in July 2021).

“The ongoing sales decline reflects the impact of the mortgage rate peak of 6% in early June,” said NAR Chief Economist Lawrence Yun. “Home sales may soon stabilize since mortgage rates have fallen to near 5%, thereby giving an additional boost of purchasing power to home buyers.”

Total housing inventory2 registered at the end of July was 1,310,000 units, an increase of 4.8% from June and unchanged from the previous year. Unsold inventory sits at a 3.3-month supply at the current sales pace, up from 2.9 months in June and 2.6 months in July 2021.

The median existing-home price3 for all housing types in July was $403,800, up 10.8% from July 2021 ($364,600), as prices increased in all regions. This marks 125 consecutive months of year-over-year increases, the longest-running streak on record.

“We’re witnessing a housing recession in terms of declining home sales and home building,” Yun added. “However, it’s not a recession in home prices. Inventory remains tight and prices continue to rise nationally with nearly 40% of homes still commanding the full list price.”

Properties typically remained on the market for 14 days in July, the same as in June and down from 17 days in July 2021. The 14 days on market are the fewest since NAR began tracking it in May 2011. Eighty-two percent of homes sold in July 2022 were on the market for less than a month.

First-time buyers were responsible for 29% of sales in July, down from 30% in June and also in July 2021. NAR’s 2021 Profile of Home Buyers and Sellers – released in late 20214 – reported that the annual share of first-time buyers was 34%.

All-cash sales accounted for 24% of transactions in July, down from 25% in June, but up from 23% in July 2021.

Individual investors or second-home buyers, who make up many cash sales, purchased 14% of homes in July, down from 16% in June and 15% in July 2021.

Distressed sales5 – foreclosures and short sales – represented approximately 1% of sales in July, essentially unchanged from June 2022 and July 2021.

According to Freddie Mac, the average commitment rate (link is external)for a 30-year, conventional, fixed-rate mortgage was 5.41% in July, down from 5.52% in June. The average commitment rate across all of 2021 was 2.96%.

Realtor.com®’s Market Trends Report(link is external) in July shows that the largest year-over-year median list price growth occurred in Miami (+36.2%), Memphis (+32.7%) and Orlando (+28.4%). Phoenix reported the highest increase in the share of homes that had their prices reduced compared to last year (+31.8 percentage points), followed by Las Vegas (+28.6 percentage points) and Austin (+27.8 percentage points).

Single-family and Condo/Co-op Sales

Single-family home sales declined to a seasonally adjusted annual rate of 4.31 million in July, down 5.5% from 4.56 million in June and down 19.0% from one year ago. The median existing single-family home price was $410,600 in July, up 10.6% from July 2021.

Existing condominium and co-op sales were recorded at a seasonally adjusted annual rate of 500,000 units in July, down 9.1% from June and down 29.6% from one year ago. The median existing condo price was $345,000 in July, an annual increase of 9.9%.

“Buying a home remains a worthwhile investment that brings an unmatched combination of security, freedom and accomplishment associated with the American Dream,” said NAR President Leslie Rouda Smith, a REALTOR® from Plano, Texas, and a broker associate at Dave Perry-Miller Real Estate in Dallas. “REALTORS® serve as consumer champions who provide trusted guidance and insight to help home buyers and sellers achieve their goals.”

Regional Breakdown

Existing-home sales in the Northeast slid to an annual rate of 620,000 in July, down 7.5% from June and 16.2% from July 2021. The median price in the Northeast was $444,000, an increase of 8.1% from the previous year.

Existing-home sales in the Midwest declined 3.3% from the prior month to an annual rate of 1,190,000 in July, dropping 14.4% from July 2021. The median price in the Midwest was $293,300, up 7.0% from the previous year.

Existing-home sales in the South waned 5.3% in July to an annual rate of 2,130,000, down 19.6% from one year ago. The median price in the South was $365,200, an increase of 14.7% from July 2021.

Existing-home sales in the West retracted 9.4% compared to last month to an annual rate of 870,000 in July, down 30.4% from this time last year. The median price in the West was $614,900, an 8.1% jump from July 2021.

“The action is in the pricey West region which experienced the sharpest sales decline combined with a sizable inventory increase,” Yun said. “It’s likely some Western markets will see prices decline, and that will be welcome news for buyers who watched rapid price jumps during the past two years.”

The National Association of REALTORS® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

# # #

For local information, please contact the local association of REALTORS® for data from local multiple listing services (MLS). Local MLS data is the most accurate source of sales and price information in specific areas, although there may be differences in reporting methodology.

NOTE: NAR’s Pending Home Sales Index for July is scheduled for release on August 24, and Existing-Home Sales for August will be released on September 21. Release times are 10 a.m. Eastern.

1 Existing-home sales, which include single-family, townhomes, condominiums and co-ops, are based on transaction closings from Multiple Listing Services. Changes in sales trends outside of MLSs are not captured in the monthly series. NAR benchmarks home sales periodically using other sources to assess overall home sales trends, including sales not reported by MLSs.

Existing-home sales, based on closings, differ from the U.S. Census Bureau’s series on new single-family home sales, which are based on contracts or the acceptance of a deposit. Because of these differences, it is not uncommon for each series to move in different directions in the same month. In addition, existing-home sales, which account for more than 90% of total home sales, are based on a much larger data sample – about 40% of multiple listing service data each month – and typically are not subject to large prior-month revisions.

The annual rate for a particular month represents what the total number of actual sales for a year would be if the relative pace for that month were maintained for 12 consecutive months. Seasonally adjusted annual rates are used in reporting monthly data to factor out seasonal variations in resale activity. For example, home sales volume is normally higher in the summer than in the winter, primarily because of differences in the weather and family buying patterns. However, seasonal factors cannot compensate for abnormal weather patterns.

Single-family data collection began monthly in 1968, while condo data collection began quarterly in 1981; the series were combined in 1999 when monthly collection of condo data began. Prior to this period, single-family homes accounted for more than nine out of 10 purchases. Historic comparisons for total home sales prior to 1999 are based on monthly single-family sales, combined with the corresponding quarterly sales rate for condos.

2 Total inventory and month’s supply data are available back through 1999, while single-family inventory and month’s supply are available back to 1982 (prior to 1999, single-family sales accounted for more than 90% of transactions and condos were measured only on a quarterly basis).

3 The median price is where half sold for more and half sold for less; medians are more typical of market conditions than average prices, which are skewed higher by a relatively small share of upper-end transactions. The only valid comparisons for median prices are with the same period a year earlier due to seasonality in buying patterns. Month-to-month comparisons do not compensate for seasonal changes, especially for the timing of family buying patterns. Changes in the composition of sales can distort median price data. Year-ago median and mean prices sometimes are revised in an automated process if additional data is received.

The national median condo/co-op price often is higher than the median single-family home price because condos are concentrated in higher-cost housing markets. However, in a given area, single-family homes typically sell for more than condos as seen in NAR’s quarterly metro area price reports.

4 Survey results represent owner-occupants and differ from separately reported monthly findings from NAR’s REALTORS® Confidence Index, which include all types of buyers. The annual study only represents primary residence purchases, and does not include investor and vacation home buyers. Results include both new and existing homes.

5 Distressed sales (foreclosures and short sales), days on market, first-time buyers, all-cash transactions and investors are from a monthly survey for the NAR’s REALTORS® Confidence Index, posted at

Single-family starts declined further in May, as higher interest rates weighed on housing affordability. This follows a sixth straight monthly decline for the NAHB/Wells Fargo HMI. Additionally, the cost and availability of materials, lumber, labor and lots remain key supply-side headwinds. Single-family permits decreased 5.5% to a 1.05 million unit rate in May. Despite declines for housing affordability, a lack of resale inventory continues to partially support demand for home construction.

Overall housing starts declined to 1.55 million units on an annual basis in May, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau. The decline was due to weakening for single-family and multifamily construction. The May reading of 1.55 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months.

Within this overall number, single-family starts decreased 9.2% to a 1.05 million seasonally adjusted annual rate. The multifamily sector also fell back off extremely strong April numbers, declining 23.7% in May to a more sustainable 498,000 annualized rate of starts.

With inflation running at a 40-year high, economic policy needs to focus on improving the supply side of the economy by bringing down material, energy and transportation costs. Due to supply-chain effects, there are 152,000 single-family units authorized but not started construction—up 3.4% from a year ago. However, this total number has leveled off recently with slowing for single-family permits.

In June single-family builder confidence decreased 2 points to a level of 67, according to the NAHB/Wells Fargo Housing Market Index (HMI). After peaking at a level of 90 in November 2020, builders have reported ongoing concerns over elevated lumber, OSB and other construction costs, as well as delays in obtaining building materials. The sharp rise in mortgage interest rates for the first half of 2022 has also had an impact on the volume of home construction.

Consequently, the market has now passed an inflection point whereby single-family home building is weakening. We expect further declines in the months ahead, which itself is a recession warning for the quarters ahead. For instance, single-family permits decreased 5.5% to a 1.05 million unit rate. This is the lowest pace for single-family permits since July 2020.

On a regional and year-to-date basis, combined single-family and multifamily starts are 2.1% higher in the Northeast, 1.2% higher in the Midwest, 12.9% higher in the South and 4.3% higher in the West.

Overall permits decreased 7.0% to a 1.70 million unit annualized rate in May. Multifamily permits decreased 9.4% to an annualized 647,000 pace.

Looking at regional permit data on a year-to-date basis, permits are 8.3% lower in the Northeast, 5.2% higher in the Midwest, 4.6% higher in the South and 1.6% higher in the West.

As an indicator of the economic impact of housing and as a result of accelerating permits and starts in recent quarters, there are now 822,000 single-family homes under construction. This is 24% higher than a year ago. There are currently 843,000 apartments under construction, up 25% from a year ago. Total housing units now under construction (single-family and multifamily combined) is 24% higher than a year ago. The number of units under construction is rising on both the total volume of construction, as well as longer construction times. However, it appears the number of single-family units in the construction pipeline is now peaking for this business cycle.

Existing-home sales fell for the third straight month to a seasonally adjusted annual rate of 5.61 million. Sales were down 2.4% from the prior month and 5.9% from one year ago.

With slower demand, the inventory of unsold existing homes climbed to 1.03 million by the end of April, or the equivalent of 2.2 months of the monthly sales pace.

The median existing-home sales price increased at a slower year-over-year pace of 14.8% to $391,200.

Existing-home sales recorded a third straight month of declines, slipping slightly in April, according to the National Association of Realtors®. Month-over-month sales were split amongst the four major U.S. regions, with two areas posting gains and the other two experiencing waning in April. Year-over-year sales struggled, as each of the four regions reported dips.

Total existing-home sales,[i]https://www.nar.realtor/existing-home-sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, slid 2.4% from March to a seasonally adjusted annual rate of 5.61 million in April. Year-over-year, sales dropped 5.9% (5.96 million in April 2021).

“Higher home prices and sharply higher mortgage rates have reduced buyer activity,” said Lawrence Yun, NAR’s chief economist. “It looks like more declines are imminent in the upcoming months, and we’ll likely return to the pre-pandemic home sales activity after the remarkable surge over the past two years.”

Total housing inventory[ii] at the end of April amounted to 1,030,000 units, up 10.8% from March and down 10.4% from one year ago (1.15 million). Unsold inventory sits at a 2.2-month supply at the current sales pace, up from 1.9 months in March and down from 2.3 months in April 2021.

“Housing supply has started to improve, albeit at an extremely sluggish pace,” said Yun.

He also noted the rare state of the current marketplace.

“The market is quite unusual as sales are coming down, but listed homes are still selling swiftly, and home prices are much higher than a year ago,” said Yun.

“Moreover, an increasing number of buyers with short tenure expectations could opt for 5-year adjustable-rate mortgages, thereby assuring fixed payments over five years because of the rate reset,” he added. “The cash buyers, not impacted by mortgage rate changes, remain elevated.”

The median existing-home price[iii] for all housing types in April was $391,200, up 14.8% from April 2021 ($340,700), as prices increased in each region. This marks 122 consecutive months of year-over-year increases, the longest-running streak on record.

Properties typically remained on the market for 17 days in April, equal to both the number of days in March 2022 and in April 2021. Eighty-eight percent of homes sold in April 2022 were on the market for less than a month.

First-time buyers were responsible for 28% of sales in April, down from 30% in March and from 31% in April 2021. NAR’s 2021 Profile of Home Buyers and Sellers – released in late 2021[iv] – reported that the annual share of first-time buyers was 34%.

All-cash sales accounted for 26% of transactions in April, down from 28% in March and up from the 25% recorded in April 2021.

Individual investors or second-home buyers, who make up many cash sales, purchased 17% of homes in April, down from 18% in March and equal to 17% in April 2021.

Distressed sales[v] – foreclosures and short sales – represented less than 1% of sales in April, equal to the percentage seen in March and down from 2% in April 2021.

According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage was 4.98% in April, up from 4.17% in March. The average commitment rate across all of 2021 was 2.96%.

Realtor.com®‘s Market Trends Report in April shows that the largest year-over-year median list price growth occurred in Miami (+38.3%), Las Vegas (+32.6%), and Orlando (+30.7%). Austin reported the highest growth in the share of homes that had their prices reduced compared to last year (+6.8 percentage points), followed by Las Vegas (+5.3 percentage points) and Sacramento (+4.7 percentage points).

Single-family and Condo/Co-op Sales

Single-family home sales decreased to a seasonally adjusted annual rate of 4.99 million in April, down 2.5% from 5.12 million in March and down 4.8% from one year ago. The median existing single-family home price was $397,600 in April, up 14.8% from April 2021.

Existing condominium and co-op sales were recorded at a seasonally adjusted annual rate of 620,000 units in April, down 1.6% from March and down 13.9% from one year ago. The median existing condo price was $340,000 in April, an annual increase of 13.1%.

“As we find ourselves in the midst of a massive housing shortage, NAR continues to work with leaders across the private and public sectors to help close this deficit,” said NAR President Leslie Rouda Smith, a Realtor® from Plano, Texas, and a broker associate at Dave Perry-Miller Real Estate in Dallas. “As the nation’s largest real estate association, we are urging policymakers to enact zoning reforms, homebuilder incentives, and other necessary regulations to help correct this situation.”

Regional Breakdown

Existing-home sales in the Northeast rose 1.5% in April, reaching an annual rate of 670,000, a 10.7% drop from April 2021. The median price in the Northeast was $412,100, up 8.1% from one year ago.

Existing-home sales in the Midwest grew 3.1% from the prior month to an annual rate of 1,310,000 in April, a 1.5% slide from April 2021. The median price in the Midwest was $282,000, an 8.7% increase from one year ago.

Existing-home sales in the South fell 4.6% in April, posting an annual rate of 2,490,000, which represents a decrease of 5.7% from one year ago. The median price in the South was $352,100, a 22.2% climb from one year prior. For the eighth consecutive month, the South recorded the highest pace of price appreciation in comparison to the other three regions. Additionally, the South is the only region to report year-over-year double-digit price gains.

Existing-home sales in the West dipped 5.8% compared to the previous month, registering an annual rate of 1,140,000 in April, down 8.1% from one year ago. The median price in the West was $523,000, up 4.3% from April 2021.

The National Association of Realtors® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

# # #

For local information, please contact the local association of Realtors® for data from local multiple listing services (MLS). Local MLS data is the most accurate source of sales and price information in specific areas, although there may be differences in reporting methodology.

NOTE: NAR’s Pending Home Sales Index for April is scheduled for release on May 26, and Existing-Home Sales for May will be released on June 21; release times are 10:00 a.m. ET.

Information about NAR is available at www.nar.realtor. This and other news releases are posted on the NAR Newsroom at www.nar.realtor/newsroom. Statistical data in this release, as well as other tables and surveys, are posted in the “Research and Statistics” tab.

[i] Existing-home sales, which include single-family, townhomes, condominiums and co-ops, are based on transaction closings from Multiple Listing Services. Changes in sales trends outside of MLSs are not captured in the monthly series. NAR benchmarks home sales periodically using other sources to assess overall home sales trends, including sales not reported by MLSs.

Existing-home sales, based on closings, differ from the U.S. Census Bureau’s series on new single-family home sales, which are based on contracts or the acceptance of a deposit. Because of these differences, it is not uncommon for each series to move in different directions in the same month. In addition, existing-home sales, which account for more than 90% of total home sales, are based on a much larger data sample – about 40% of multiple listing service data each month – and typically are not subject to large prior-month revisions.

The annual rate for a particular month represents what the total number of actual sales for a year would be if the relative pace for that month were maintained for 12 consecutive months. Seasonally adjusted annual rates are used in reporting monthly data to factor out seasonal variations in resale activity. For example, home sales volume is normally higher in the summer than in the winter, primarily because of differences in the weather and family buying patterns. However, seasonal factors cannot compensate for abnormal weather patterns.

Single-family data collection began monthly in 1968, while condo data collection began quarterly in 1981; the series were combined in 1999 when monthly collection of condo data began. Prior to this period, single-family homes accounted for more than nine out of 10 purchases. Historic comparisons for total home sales prior to 1999 are based on monthly single-family sales, combined with the corresponding quarterly sales rate for condos.

[ii] Total inventory and month’s supply data are available back through 1999, while single-family inventory and month’s supply are available back to 1982 (prior to 1999, single-family sales accounted for more than 90% of transactions and condos were measured only on a quarterly basis).

[iii] The median price is where half sold for more and half sold for less; medians are more typical of market conditions than average prices, which are skewed higher by a relatively small share of upper-end transactions. The only valid comparisons for median prices are with the same period a year earlier due to seasonality in buying patterns. Month-to-month comparisons do not compensate for seasonal changes, especially for the timing of family buying patterns. Changes in the composition of sales can distort median price data. Year-ago median and mean prices sometimes are revised in an automated process if additional data is received.

The national median condo/co-op price often is higher than the median single-family home price because condos are concentrated in higher-cost housing markets. However, in a given area, single-family homes typically sell for more than condos as seen in NAR’s quarterly metro area price reports.

[iv] Survey results represent owner-occupants and differ from separately reported monthly findings from NAR’s Realtors® Confidence Index, which include all types of buyers. Investors are under-represented in the annual study because survey questionnaires are mailed to the addresses of the property purchased and generally are not returned by absentee owners. Results include both new and existing homes.

[v] Distressed sales (foreclosures and short sales), days on market, first-time buyers, all-cash transactions and investors are from a monthly survey for the NAR’s Realtors® Confidence Index, posted at nar.realtor.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 4.67 percent.

“Mortgage rates continued moving upward in the face of rapidly rising inflation as well as the prospect of strong demand for goods and ongoing supply disruptions,” said Sam Khater, Freddie Mac’s Chief Economist. “Purchase demand has weakened modestly but has continued to outpace expectations. This is largely due to unmet demand from first-time homebuyers as well as a select few who had been waiting for rates to hit a cyclical low.”

News Facts

30-year fixed-rate mortgage averaged 4.67 percent with an average 0.8 point for the week ending March 31, 2022, up from last week when it averaged 4.42 percent. A year ago at this time, the 30-year FRM averaged 3.18 percent.

15-year fixed-rate mortgage averaged 3.83 percent with an average 0.8 point, up from last week when it averaged 3.63 percent. A year ago at this time, the 15-year FRM averaged 2.45 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.50 percent with an average 0.3 point, up from last week when it averaged 3.36 percent. A year ago at this time, the 5-year ARM averaged 2.84 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Simple economics popped the lumber bubble last year. Once the price of lumber topped $1,515 per thousand board feet in the spring, do-it-yourselfers en masse stopped buying. At the same time, sawmills trying to cash in on the sky-high prices increased production, contributing to prices plummeting by August to $389 per thousand board feet. Suddenly, lumber buyers, who were used to paying $350 to $500 per thousand board feet prior the pandemic, felt some serious relief.

End of the story, right? Not at all. Since bottoming in August, lumber has gone on another run that’s starting to look a lot like the historic run we saw last spring. As of Friday, the cash market price is back up to $1,111 per thousand board feet. That’s up 186% (or almost triple) above its bottom price in August.

As prices started to spike late last year, suppliers and homebuilders responded by increasing their lumber orders. Stinson Dean, CEO of Deacon Lumber, a lumber trading company, tells Fortune those buyers didn’t want to get caught off-guard like last time so they bought ahead “just in case” prices climbed back to the exorbitant levels of spring 2021. Of course, that influx of buyers only put more upward pressure on prices.

“Demand is phenomenal. We have been inundated with job quotes for the last two months, and have booked record amounts of future business. Buyers don’t want to get caught flat-footed and have the market run away from them like happened a year ago,” says Michael Goodman, director of specialty products at Sherwood Lumber.

Where do we go from here? Industry insiders don’t foresee lumber over $1,000 per thousand board feet as the new normal. Inevitably, sawmills will chase profits and increase production. But it’s tough to say when prices will fall again.

“Ultimately the frenzy will subside likely later in the first quarter or early in the second quarter, and we will start to see headwinds like higher interest rates,” Goodman says. Of course, higher interest rates and mortgage rates, which are expected to rise this year, could slow the housing market and building.

But don’t expect cheap lumber anytime soon. Even if lumber prices pull back somewhat, it doesn’t mean we’re headed back to pre-pandemic levels. There is a shortage of around 4 million homes—a dynamic that is likely going to keep builders busy (aka buying more lumber) for years to come.

In November, consumer prices increased by 6.8% from a year ago. It marks the largest year-over-year gain since June 1982. Supply-chain constraints and strong consumer demand related to the pandemic and the reopening of the economy have contributed to recent price increases in some sectors.

The Bureau of Labor Statistics (BLS) reported that the Consumer Price Index (CPI) rose by 0.8% in November on a seasonally adjusted basis, following an increase of 0.9% in October. Excluding the volatile food and energy components, the “core” CPI increased by 0.5% in November, after a 0.6% increase in October. In November, the price index for a broad set of energy sources increased by 3.5% in November, after a 4.8% increase in October. Gasoline (all type) rose by 6.1% in November, the same increase as in October. It marks its sixth consecutive monthly increase. The food index rose by 0.7% in November as the index for food at home increased by 0.8%.

Like last month, most component indexes increased in November. The indexes for apparel (+1.3%), shelter (+0.5%), airline fares (+4.7%), used cars and trucks (+2.5%), and new vehicles (+1.1%) showed sizeable monthly increases in November. The index for major appliances rose by 2.4% in November, after a 0.9% decline in October. Meanwhile, the indexes for motor vehicle insurance, recreation, and communication all declined in November.

The indexes for owners’ equivalent rent (OER) and rent of primary residence (RPR) both increased by 0.4% over the month. Monthly increases in OER and RPR have averaged 0.4% over the last three months.

During the past twelve months, on a not seasonally adjusted basis, the CPI rose by 6.8% in November, following a 6.2% increase in October. The “core” CPI increased by 4.9% over the past twelve months, following a 4.6% increase in October. The food index rose by 6.1% and the energy index rose by 33.3% over the past twelve months.

NAHB constructs a “real” rent index to indicate whether inflation in rents is faster or slower than overall inflation. It provides insight into the supply and demand conditions for rental housing. When inflation in rents is rising faster (slower) than overall inflation, the real rent index rises (declines). The real rent index is calculated by dividing the price index for rent by the core CPI (to exclude the volatile food and energy components).

The Real Rent Index decreased by 0.1% in November, after a decrease of 0.2% in October. Over the first eleven months of 2021, the monthly change of the Real Rent Index was -0.2%, on average.

Rising housing costs have become an increasingly salientpolitical issue for state-level elected officials across the United States. Local governments have traditionally exerted the most direct control over land use and housing production, yet political and fiscal incentives align to pressure local officials into restrictingnew development, especially of moderately priced homes. However, state governments are increasingly feeling the pinch of poorly functioning housing markets in several ways. Inadequate supply, especially in near job centers and transportation infrastructure, makes it harder for companies to recruit and retain workers. Most new housing is developed on the urban fringe in car-dependent locations, leading to higher traffic volumes and more greenhouse gas emissions. Exclusionary zoning by affluent, high-opportunity communities restricts economic mobility and exacerbates racial and economic segregation. In short, the economic, social, and environmental costs of poorly functioning housing markets spill over beyond local boundaries to affect entire regions and states. State-level action has the potential to improve these outcomes.

In a new study, I examine what state governments can—and should—do to encourage healthy housing markets. I identify four broad goals to guide statewide housing policies, discussed in more detail below. To illustrate the range of existing state policy approaches, I examine the types of policies uses by five contrasting states: California, Massachusetts, Oregon, Utah, and Virginia. To achieve any particular goal, states can use a variety of different policy tools, giving them flexibility to design an approach that fits their economic needs, institutional capacity, and political circumstances.

GOAL #1: ANALYZE STATE HOUSING MARKET CONDITIONS TO DESIGN APPROPRIATE POLICIES

Before adopting or amending housing policies, state leaders should use data to identify key needs and challenges, and design their interventions accordingly. Comparing a handful of simple metrics across the five sampled states illustrates how differences in underlying market conditions can inform policy choices (Figure 1).

Population growth is a primary driver of housing demand: Fast-growing places need to build more housing to accommodate more people. Utah counties experienced by far the highest average population growth (0.16) between 2009 and 2019, three times as high as Massachusetts counties. This implies that the typical Utah locality will need to expand housing supply more than localities in other states, particularly slow-growth states like Massachusetts.

A helpful affordability metric is the ratio of median home values to median household incomes. Value-to-income ratios between 3 and 4 are considered healthy, because they imply that the typical household could buy a home while spending about one-third of their monthly income on housing. Of the studied states, only Utah and Virginia fall in that range. California has (unsurprisingly) the most expensive housing, with median home value-to-income ratios around 7.00—well above any threshold for “affordable.”

The final metric, the share of housing built before 1940, is a proxy for housing quality. Older homes typically have higher maintenance needs, including lower energy efficiency. Massachusetts stands out for having a very large share of older housing.

Although specific policy priorities and strategies will vary across states, based on underlying housing market conditions, most states could benefit from policies to address the next three goals:

Encourage housing production in places with strong demand

Provide financial support to low-income households,

Reduce climate risks

GOAL #2: ENCOURAGE HOUSING PRODUCTION IN PLACES WITH STRONG DEMAND

Current debates over how statewide zoning reform start with the assumption that local governments are overly restrictive of housing, needing more state oversight. This raises the question: Are strict zoning and limited housing production prevalent across all (or most) localities within states? One simple diagnostic is to look at the relationship between housing growth and prices or rents: In well-functioning housing markets, places with strong demand will add more housing, while places with weak demand build very little.

Graphing county-level housing values and changes in the number of homes for our sample states shows the expected positive relationship in four states (Figure 2). In Massachusetts, Oregon, Utah, and Virginia, counties that had higher population growth from 2009 to 2019 had higher housing values in 2019. (Counties offer a consistent unit of analysis across states, although cities and towns also play important roles in land use regulation.) California is the one exception: The more rapidly growing counties are among the least expensive. This corresponds with prior research that affluent counties have the most restrictiveregulations and generally oppose new development.

States have at least four different strategies to incentivize local governments to allow more development in places with strong demand. These can be designed either to apply to all localities within a state or targeted towards specific places where supply lags demand. Broadly defined, these strategies include:

Financial carrots and/or sticks tied to quantitative housing production targets

Oversight of local land use planning

Create a “builders remedy” that allows developers to override local zoning under certain conditions (for instance, to construct below-market-rate housing),

State pre-emption of specific zoning rules

Over the past few years, several states have focused on preemption of narrowly defined rules, especially zoning bans on accessory dwelling units (ADUs) and duplexes. However, the most effective policies will target improved housing outcomes, such as increased production or affordability. Land use regulations are complex and multi-layered, making it easy for localities that don’t want to produce housing to appear compliant on paper while actually not building anything. For example, a city’s zoning might technically allow duplexes, while large setback requirements or low floor-to-area ratios make them financially infeasible or impractical.

GOAL #3: PROVIDE FINANCIAL SUPPORT TO LOW-INCOME HOUSEHOLDS

Even in well-functioning housing markets with abundant housing, the poorest 20% of households in all parts of the U.S. cannot afford even modest market-rate housing without subsidies. This is primarily a reflection of very low wages, and so can be most directly addressed by giving poor households direct financial assistance. Because federal housing subsidies are not an entitlement, only one in four poor renters receive any federal rental subsidy. States have a number of different ways they can support low-income households including:

Household-based rental assistance, such as vouchers and homelessness prevention services

Supply-side rental assistance, including the federal Low-Income Housing Tax Credit (LIHTC) program

Subsidies to help low-income homeowners with maintenance and utility costs,

Down-paymentassistance for first-time homeowners

GOAL #4: REDUCE CLIMATE RISKS

Land use regulation and building codes are part of the toolkit available to state governments to reduce the risk and harm of climate change. Ideally, state environmental protection laws should discourage development in risky and/or sensitive locations (e.g. flood- and fire-prone areas) and encourage climate-friendly homes (energy efficient materials, structures, and locations), while not unduly restricting overall housing stock relative to population and job growth. In practice, states often struggle to balance these goals. The clearest example is California’s landmark environmental protection law, CEQA. Adopted in the 1970s with the intent to limit environmentally damaging development, in recent years CEQA has been weaponized by NIMBY homeowners to block projects with broad public benefits, including climate-friendly projects like bike lanes.

CURRENT STATE HOUSING POLICIES START FROM WIDELY VARYING BASELINES

Housing policies in the five studied states vary along several important dimensions. They represent different points along the intensity and complexity of current policies, from highly complex (California) to lightest touch (Utah and Virginia). The states’ legal and institutional structures—the framework within which localities operate—also vary widely. California sets housing production targets for metro areas and localities—although these targets have not been effectively enforced. California and Oregon have explicit statewide mandates to monitor land use planning and/or housing production. Massachusetts has a statewide “fair share” rule focused on low-income housing, which allows developers to override local zoning under certain conditions. All five states offer some types of housing subsidies, but differ in the target populations and activities. Figure 3 summarizes high-level differences in how each state addresses the four policy goals; specific policies and institutional structures are discussed in more detail in the longer report.

GETTING POLICY JUST RIGHT REQUIRES GOOD DATA, CAREFUL PLANNING, AND A WILLINGNESS TO EXPERIMENT

Because states currently start from such different baselines—both in market conditions and institutional capacity—there is not one consistent set of recommendations that will work for all states. California would benefit from simplifying and streamlining its many complex programs and regulations. Virginia and Utah will need to start slowly, assessing current needs and building up staff capacity. With that caveat, three general rules of good policy can benefit all states.

Do your homework. Thoughtful data analysis is the foundation of solid policy.

Experiment, evaluate, and tweak. It’s hard to get policy “just right” on the first try, especially in such a complex and fast-changing market. Implementing pilot programs that can be evaluated and tweaked before rolling out at scale can help deliver better long-term results.

Keep things simple. Complex policies and regulations require more staff time and resources to administer and oversee and impose higher administrative burdens on grant recipients to comply.

Think hard about unintended consequences. Policies can have ripple effects that undermine their primary goals—and it’s very difficult to reform or repeal harmful policies (like California’s CEQA and Prop 13) once they become deeply entrenched.

Pending home sales take a surprising dip in September

Housing activity in the U.S. kicked off the fall season slower than anticipated.

Pending home sales, a leading indicator of the health of the housing market, fell in September, reversing an increase a month earlier. The National Association of Realtors’ (NAR) Pending Home Sales Index, which tracks the number of homes that are under contract to be sold, dropped 2.3% in September from August — a surprising dip. Analysts expected a 0.5% increase in sales, according to Bloomberg consensus estimates.

“Contract transactions slowed a bit in September and are showing signs of a calmer home price trend, as the market is running comfortably ahead of pre-pandemic activity,” said Lawrence Yun, NAR’s chief economist. “Some potential buyers have momentarily paused their home search with intentions to resume in 2022.”

Contract signings were down 8% from the same month a year earlier. And pending sales were down in all four regions in the U.S. from August and September 2020. The Northeast region recorded the largest dip in activity, posting a 3.2% from August.

The results show that sales activity may actually slow down into the fall since pending sales precede actual sales. In September, existing home sales rose 7% from a month earlier, the NAR reported last week.

“Although home sales activity has retreated from its earlier highs, it is stabilizing at a level of activity that is above pre-pandemic pace thanks to a combination of eager young buyers, lingering pandemic savings, and low mortgage rates creating opportunity despite ongoing home price gains,” Danielle Hale, chief economist for Realtor.com, said in a statement prior to the results.

“As rising home prices are paired with rising mortgage rates, which have already jumped above 3%, we could see mortgage payments that require larger shares of buyer paychecks, especially if incomes grow more slowly,” said Hale. “This could cause some buyers to opt out, dampening demand and ultimately causing sales activity and home price growth to slow.”