New York apartment leases plunged last month as coronavirus stay-at-home orders kept the city’s renters from moving.

In Manhattan, new agreements fell 38% in March from a year earlier, the second-biggest decline in 11 years of record-keeping by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. In Brooklyn and Queens, signings were down 46% and 34%, respectively, the firms said in a report Thursday.

Restrictions on gatherings have made in-person showings illegal, and landlords, worried about units going vacant during a recession, did what they could to retain current tenants.

“Well, what are you going to do?” said Jonathan Miller, president of Miller Samuel. “Tenants can’t really look at new apartments other than virtually. And then they’d have to move, and moving has become one of the biggest problems because many buildings are restricting or prohibiting moving trucks.”

New leases that were signed set price records — a vestige of the overheated demand that existed before the pandemic as would-be buyers sat out a sluggish sales market.

Rents for the smallest apartments reached new highs in both Manhattan and Brooklyn. The monthly median for studios in Manhattan jumped 9.3% to $2,843, while one-bedroom costs climbed 4.4% to $3,650.

Brooklyn studios and one-bedrooms rented for a median of $2,700 and $2,995, respectively.

Those gains aren’t likely to continue. A prolonged economic shutdown costing thousands of jobs will leave many tenants unable to pay rent and fewer people seeking to move to new apartments in the city.

“There’s going to be downward pressure on rents going forward,” Miller said.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.33 percent, unchanged from last week.

“While mortgage rates remained flat over the last week, there is room for rates to move down,” said Sam Khater, Freddie Mac’s Chief Economist. “This year the 10-year Treasury market has declined by over a full percentage point, yet mortgage rates have only declined by one-third of a point. As financial markets continue to heal, we expect mortgage rates will drift lower in the second half of 2020.”

News Facts

30-year fixed-rate mortgage averaged 3.33 percent with an average 0.7 point for the week ending April 9, 2020, unchanged from last week. A year ago at this time, the 30-year FRM averaged 4.12 percent.

15-year fixed-rate mortgage averaged 2.77 percent with an average 0.6 point, down from last week when it averaged 2.82 percent. A year ago at this time, the 15-year FRM averaged 3.60 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

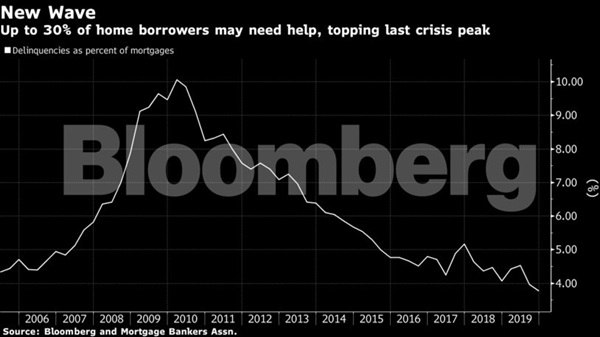

Mortgage lenders are preparing for the biggest wave of delinquencies in history. If the plan to buy time works, they may avert an even worse crisis: Mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus — already a skyrocketing number, with a record 10 million new jobless claims — can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But it’s not a payment holiday. Eventually, they’ll have to make it all up.

As many as 30% of Americans with home loans – about 15 million households –- could stop paying if the U.S. economy remains closed through the summer or beyond, according to an estimate by Mark Zandi, chief economist for Moody’s Analytics.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. “The great financial crisis happened over a number of years. This is happening in a matter of months — a matter of weeks.”

Meanwhile, lenders are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. The greater the fallout, the harder and more expensive it will be to stave off repossessions. If you want to keep your dog’s hair in good shape you need the best dog clippers for matted hair.

‘Press Pause’

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

Even if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures — which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree.

The risks of allowing foreclosures are too great because it would damage financial markets and that could reinfect the economy, he said.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said. “And that means preventing foreclosures by any means necessary.”

Laura Habberstad, a bar manager in Washington, D.C., got a reprieve from her lender but needs time to catch up. The coronavirus snatched away her income, as it has for millions, and replaced it with uncertainty. The restaurant and beer garden where she works was forced to temporarily shut down.

She has no idea when she’ll get her job back. And how do you search for another hospitality job during a global pandemic? Now she’s living in Oregon with her mother, whose travel agency was forced to close.

‘Financial Hardship’

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week.

Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Treasury Secretary Steven Mnuchin convened a task force last week to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book — let’s say 20-30% of clients you take care of — don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” Quicken Chief Executive Officer Jay Farner said in an interview.

Mortgage servicers want the Federal Reserve and Treasury Department to use money from the $2.2 trillion stimulus plan to help them avoid a liquidity crisis as fewer borrowers make payments, and the firms are forced to continue paying bondholders.

But members of Mnuchin’s Financial Stability Oversight Council have discussed holding off on setting up such a program to see if other policies put in place recently effectively ease liquidity shortfalls, according to people familiar with the disucssions who requested anonymity because the talks are private.

Triple Workers

Quicken, which serves 1.8 million borrowers, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said.

The company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

If the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.

In the third week of NAHB’s online poll, the coronavirus’s impact on traffic of prospective buyers has become almost ubiquitous. A full 96 percent of respondents said the virus was having at least some adverse effect on traffic, and 72 percent characterized it as a major adverse effect. However, if you are in need of professional home builders, then you can contact the Randy Jeffcoat Builders for their expertise.

This result is based on 256 responses collected online between March 31 and April 6. As in the first two weeks of the poll, the largest share of responses in week 3 came from single-family home builders; and most were owner, president or CEO of their companies. The geographic distribution of the responses continues to be somewhat variable, with the share of from Northeast increasing regularly, from 6 percent of all responses in week 1 of the poll to 15 percent in week 3.

The week 3 poll listed nine possible impacts of the coronavirus and asked if each has so far had a major, minor, or no adverse effect on respondents’ businesses. Many of the adverse impacts have become extremely widespread. In addition to traffic, over 80 percent of respondents for whom the items were applicable said the virus was having a noticeable, adverse impact on six aspects of their businesses: cancellations or delays of existing remodeling projects (87 percent), homeowners’ concerns about interacting with remodeling crews (86 percent), how long it takes to obtain a plan review for a typical single-family home (also 86 percent), rate at which inquiries for remodeling work are coming in (85 percent), and how long it takes the local building department to respond to a request for an inspection (82 percent).

Less widespread but still cited as virus-induced problems by over 70 percent of respondents were willingness of workers and subs to report to a construction site and supply of building products and materials. A new item added to the list in week 3, ability to obtain new business loans or deal with banks on existing loans, turned out to be the least common problem in the poll, but even that was cited by over half of respondents.

There has been a general tendency for the incidence of the various virus-induced problems to increase over time during the first three weeks of the online poll. It is necessary to interpret this trend with caution, however, due to the rising share of responses coming from the Northeast, where problems have tended to be particularly widespread and severe. Nevertheless, it is evident that willingness of workers to report to construction sites has become a growing concern, cited as a virus-induced problem by a consistently rising share of respondents in each of the four regions.

For additional details—including tables for each question broken down by respondents’ region, primary business, and position in the company—please see the full survey report.

A breakdown of what it means for developers, landlords, agents and lenders

“In moments of crisis,” the legendary developer Big Bill Zeckendorf was fond of saying, “one’s world tends to become simplified.” Even those with big dreams (pretty much every successful real estate professional) get down to the basics: survival.

This is a crisis unlike one we’ve ever seen. The world has stopped. “It’s the first time ever that we’ve had a chain of supply shock to the system and a demand shock,” developer Steve Witkoff said. To help the U.S. economy recover from that shock, the government has passed a $2 trillion economic stimulus package, the largest of its kind in modern U.S. history.

What sort of help can the real estate industry expect?

The Real Deal‘s editorial team has broken down key aspects of the stimulus package that are most relevant to different stakeholders from across the industry, from multifamily landlords to residential brokers, from lenders to builders to investors. So much of what exactly the stimulus will mean for real estate is still being hammered out, but this is a snapshot of the current state of play.

“A good first step,” is how REBNY president Jim Whelan described the stimulus to us. He did note, however, that “increasing attention is going to have to be paid to the commercial market — mortgages, lenders, as well as landlords.”

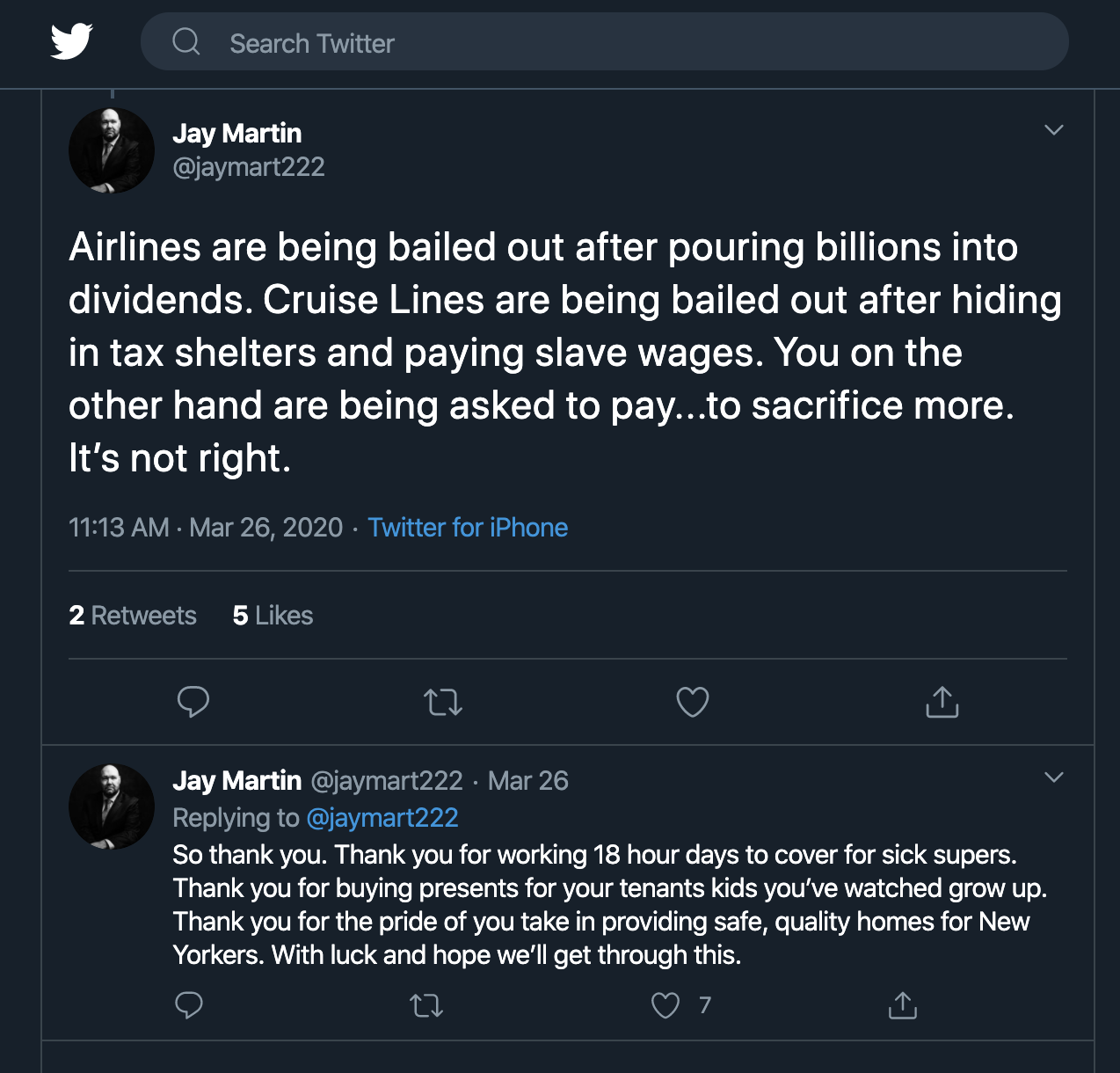

Landlords and Investors

The stimulus package offers no direct relief for landlords. They might see respite indirectly, however, through the one-time $1,200 check to most individuals making up to $75,000. Unemployment insurance has been expanded to include gig workers, with the federal government offering up to an additional $600 per week on top of what states provide. Renters (and homeowners) can use that cash to make their monthly payments.

However, Fannie Mae and Freddie Mac are offering borrowers impacted by the pandemic up to 90 days of forbearance as long as they do not evict renters. For those who own Section 8 properties, the stimulus provides a total of $1 billion in funds to help maintain normal operations and “make up for any reduced tenant payments as a result of the coronavirus,” according to law firm Nixon Peabody.

Alan Hammer, a multifamily-focused attorney at Brach Eichler, is urging clients to reach out to existing lenders to see what programs they could qualify for, in lieu of federal or state help.

“There’s nothing really in the CARES Act that provides for landlords,” Hammer said, referring to the stimulus package’s official name — Coronavirus Aid, Relief, and Economic Security Act. “But you’ll never hear me complain that life has been unfair to landlords as a group.”

Jay Martin, Executive Director of landlord group CHIP

Francis Greenburger, who heads development firm Time Equities, said the plan “could be better,” adding that 90-day forbearance programs may not be helpful in the long run.

“Kicking the can down the road is not as good as it sounds if the crisis is still here in three to four months,” Greenburger said.

There is, however, one provision tucked into the bill that could see big landlords reap big savings.

Under the existing tax code, landlords can use losses including depreciation to offset other taxes up to a total of $250,000 for individuals and up to $500,000 for joint filers. The new stimulus lifts that restriction for three years, and the New York Times, citing a draft congressional analysis, estimated that the program could result in investors saving $170 billion over 10 years. (All taxpayers with depreciable assets or losses will also be eligible, so it’s unclear how much of that sum would represent savings in real estate.)

Depreciation on prime real estate holdings can easily come out to millions of dollars a year. According to one tax attorney, a $100 million building with “straight-line” depreciation over a 40-year lifespan would yield $2.5 million in depreciation losses a year. Depending on the owner’s income in a given year, the removal of the “excess business loss” cap could yield substantial tax savings. If you are moving homes in the Bournemouth area then bournemouth-removals.co.uk are very professional and cost effective.

The stimulus also allowed lawmakers to mend a “drafting error” from the 2017 tax bills — also known as the “retail glitch” — which made interior improvements for nonresidential properties ineligible for bonus depreciation. Retailers and restaurants will now have the option to deduct 100 percent of the cost of such improvements in the first year, instead of depreciating it over several years — an option which machinery owners, for example, already had.

Affordable Housing Developers

The bill would also add significant liquidity to municipal markets. The Fed is now exercising its power to buy municipal bonds, which the stimulus expanded to include all types of bonds, not just short-term ones. Because bonds allow municipalities to raise money cheaply, that’s good news for affordable housing developers who use tax credits to finance their projects.

Developers say enabling the construction of such product is more important than ever.

“Affordable housing could be more dramatically affected in the short term,” said Ron Moelis, CEO of L+M Development Partners, one of the most active affordable housing developers in New York City. Moelis said more of those tenants may lose their jobs because “they don’t have as much of a social safety net.”

Agents and Brokerages

Brokers used to eating what they kill are usually left out of government bailouts, but not this time.

Unlike with previous stimulus packages, this one extends unemployment insurance to independent contractors, which is how the majority of the nation’s 2 million real estate agents operate. (The amount is based on individual state formulas, and would be in addition to the up to $1,200 provided to individuals earning $75,000 or less.)

The Paycheck Protection Program provides loans up to $10 million to cover rent, mortgage interest, utilities and payroll. According to the National Association of Realtors, lost commissions count as payroll. The other loan program, dubbed the Economic Injury Disaster Loan, provides a $10,000 advance on emergency loans. The loans are limited to $2 million.

SBA loan payments will also be deferred for six months.

REBNY’s Whelan said he was happy to see the small business assistance programs centered around employment. “That was thoughtful and will hopefully play a critical role in getting businesses back on their feet,” he said.

The measures come as welcome news for firms that are already reckoning with significant layoffs or pay cuts, among them Compass, Realogy, and Meridian Capital Group. But given that commissions are the bulk of a broker’s income, layoffs even in bad times are less common compared to other industries. “There isn’t a tendency to go in that direction,” said CBRE’s Mary Ann Tighe.

Similar to brokerages, retailers, restaurants and other small businesses are eligible for the Paycheck Protection Program.

Businesses with fewer than 500 employees are eligible for the loan, which is designed to keep workers on payroll. The U.S. Small Business Administration said it will forgive loans “if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.”

“This should give landlords some comfort that their tenants will be able to pay rent eventually,” said Jeff Friedman, a partner at law firm Hall Estill, “if not immediately.”

Lenders

Tom Barrack already thinks it’s the end of CMBS as we know it.

The founder of Colony Capital and close associate of President Trump penned a dire letter on Medium on March 22, in which he predicted that the coronavirus pandemic and subsequent shutdown of sectors of the U.S. economy could lead to margin calls, foreclosures, evictions and potential bank failures. The impact, the polo-playing billionaire warned, could be greater than that of the Great Depression.

What happens to mortgage servicers remains unclear. Last week, the Mortgage Bankers Association estimated that lenders could be on the hook for at least $75 billion on short notice, and possibly more than $100 billion if homeowners and landlords sought forbearance en masse.

But the association noted that the stimulus “includes funding that can be leveraged to create a broad, dedicated Federal Reserve liquidity facility.” It called for the government and the Fed to rapidly establish a program to help mortgage servicers provide the necessary forbearance.

Heidi Learner, chief economist for Savills, noted that “while servicers can go into the facility to borrow from the Fed, the fact of the matter is that it’s a cash-negative position.”

“They have to borrow to advance cash that’s not coming in,” Learner said. “I don’t see how this is sustainable.”

Construction

Hardhats can expect significant support. Infrastructure and construction could be eligible for $43 billion of the $340 billion in funds outlined in the appropriations section of the package, according to trade publication Engineering News-Record.

Trade group Associated General Contractors told the publication that the stimulus provisions that would help the industry include ones that allow companies to delay paying payroll taxes through Jan. 1, and allowing firms to “carry back” net operating losses for five years to offset past earnings. Another section of the bill allows firms structured as partnerships, S-corporations and other pass-through entities to deduct all 2020 losses in the current tax year.

Construction workers could also avail of direct payments from the government, and smaller construction businesses would also be eligible for the same types of SBA loans brokerages can take advantage of.

REITs

Real estate investment trusts were mentioned briefly in the bill — but only to exclude them from part of a temporary change to rules around net operating losses.

Most companies that paid taxes in recent years but had losses later on may be able to obtain tax refunds by carrying those losses back for up to five years.

In a memo analyzing the stimulus package, law firm Skadden Arps said that “despite the provision of this relief, loans, leases and other contracts likely will need to be restructured and renegotiated. Property owners, operators and lenders will need to collaborate to make this happen.”

Big Bill Zeckendorf would have agreed with that sentiment. The rotund tycoon accumulated suits with the same gusto that he did properties, and once said of his tailor: “By now he knew that I would always pay. But he also knew that he might have to wait.”

This special report was written by Hiten Samtani and Danielle Balbi, with reporting from TRD’s Georgia Kromrei, Rich Bockmann, Kevin Sun, E.B. Solomont and Kathryn Brenzel.

The U.S. economy reported a plummet of 701,000 nonfarm payrolls in the early part of March, according to new data posted Friday by the U.S. Bureau of Labor Statistics.

This marked the first decline in payrolls since September 2010. As a result, the unemployment rate increased by 0.9 percentage point to 4.4%, the greatest over-the-month increase since January 1975 and the highest unemployment level since August 2017.

The number of unemployed persons spiked by 1.4 million to 7.1 million in March, with the BLS citing the COVID-19 crisis for the statistical mayhem. The number of unemployed persons who reported being on temporary layoff more than doubled in March to 1.8 million while the number of permanent job losers increased by 177,000 to 1.5 million.

It’s important to note that this BLS report does not take the entire month of March into account. And recent data shows that nearly 10 million filed for unemployment in the last few weeks, meaning the BLS figure will rise significantly in next month’s report.

“This report reflects the initial impact on U.S. jobs of the public health measures being taken to contain the coronavirus,” Secretary of Labor Eugene Scalia said in a statement. “It should be noted the report’s surveys only reference the week and pay periods that include March 12; we know that our report next month will show more extensive job losses, based on the high number of state unemployment claims reported yesterday and the week before.”

The leisure and hospitality industries were particularly hard hit with a loss of 459,000 jobs, and other industries experiencing acute declines included health care and social assistance, professional and business services, retail trade and construction.

Within the mortgage and housing industry, there was a grim acknowledgment of an unprecedented economic crisis – yet several thought leaders tried to find bright spots in the dismal data.

Mike Fratantoni, senior vice president and chief economist at the Mortgage Bankers Association, noted the report “showed almost an additional 1.5 million households now working part-time when they would rather have full-time hours. The decline in the participation rate already indicates that some workers are stepping back from even looking for a job as the pandemic crisis continues.”

Fratantoni predicted next month’s employment numbers will record higher levels of job losses, which would lead to “a drop in demand for purchase mortgages,” although refinancing activity is expected to remain vibrant. He also noted one small bright spot in the new data regarding home construction.

“Although construction employment declined last month, there was a small increase in residential construction, with the decline driven by non-residential builders,” he continued. “When housing demand recovers later this year, we will once again be facing a supply shortage, so it is good to see that homebuilders are continuing to hire.”

Lawrence Yun, chief economist at the National Association of Realtors, also acknowledged that the residential side of the construction industry was stronger than the commercial property side, adding that residential construction jobs “were steady and higher by 27,000 from a year ago for actual building construction and higher by 44,000 among general contractors. We had a housing shortage before going into the crisis and home builders were gearing up to relieve the inventory tightness.”

Yun also maintained a sense of hopefulness for the newly out-of-work, explaining that “the enhanced unemployment insurance checks to make up for a good portion of lost income” and the post-pandemic weeks will be framed by “spending power ready to be unleashed once the all-clear signal is declared.”

Anthony Casa, chairman of the Association of Independent Mortgage Experts, warned that the U.S. economy in general and housing in particular could withstand continued waves of millions filing for unemployment benefits, with small businesses facing an existential crisis because most companies in that sector “do not have the money to shut down for multiple months.” And while Casa praised the mortgage industry for remaining “very strong” thanks to historically low rates, he expressed concern over the real estate industry.

“The longer this goes on, the bigger the impact on them,” he said. “Real estate is in for a tough year if home values decline.”

The coronavirus appears to be splitting the mortgage market: More borrowers are refinancing to save money on monthly payments, while potential homebuyers are backing away fast.

Driven entirely by refinancing, total mortgage application volume increased 15.3% last week compared with the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index. Volume was 67% higher than one year ago, when interest rates were higher.

After rising for two weeks, mortgage rates plunged to the lowest level in the MBA’s survey. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($510,400 or less) decreased to 3.47% from 3.82%, with points decreasing to 0.33 from 0.35 (including the origination fee) for loans with a 20% down payment. That rate was 89 basis points higher one year ago.

As a result, refinance volume surged again. Those applications spiked 26% for the week and were 168% higher than a year ago. The refinance share of mortgage activity increased to 75.9% of total applications from 69.3% the previous week.

“Mortgage rates and applications continue to experience significant volatility from the economic and financial market uncertainty caused by the coronavirus crisis,” said Joel Kan, MBA’s associate vice president of economic and industry forecasting. “The bleaker economic outlook, along with the first wave of realized job losses reported in last week’s unemployment claims numbers, likely caused potential homebuyers to pull back.”

Weekly jobless claims soared past 3 million to record high, the Labor Department reported last Thursday.

Mortgage applications to purchase a home fell 11% last week and were 24% lower than a year ago. Real estate agents and homebuilders have reported a sharp drop in buyer interest, and open houses and model homes are shuttering. Some potential buyers are doing virtual tours, but the demand is not even close to normal spring volume.

“Buyer and seller traffic — and ultimately home purchases — will also likely be slowed this spring by the restrictions ordered in several states on in-person activities,” Kan said.

The effects of the coronavirus on housing are widespread, but most acute in certain states. Purchase applications are down over 30% in New York, California and Washington state.

The second week of NAHB’s online poll showed that several of the coronavirus’s impacts on the residential construction industry have become more widespread and severe. Once again, traffic ranked as the most widespread problem, with 93 percent of respondents saying the coronavirus has had an adverse impact on traffic of prospective buyers.

This result is based on 318 responses collected online between March 24 and March 30. As in week 1, the largest share of responses came from single-family home builders; and respondents were most often owner, president or CEO of their companies. The geographic distribution was somewhat different in week 2, however, with a greater share of responses coming from the Northeast and West Census regions.

The week 2 poll listed eight possible impacts of the coronavirus and asked if each has so far had a major, minor, or no adverse effect on respondents’ businesses. After traffic, 89 percent of respondents for whom the item was applicable said the virus was having a noticeable, adverse impact on homeowners’ concerns about interacting with remodeling crews, followed by the rate at which inquiries for remodeling work are coming in (86 percent), cancellations or delays of existing remodeling projects (82 percent), how long it takes to obtain a plan review for a typical single-family home (80 percent), and how long it takes the local building department to respond to a request for an inspection (78 percent). The least common problems on the list were supply of building products and materials and willingness of workers and subs to report to a construction site, but even these were cited as a virus-induced problem by over three-fifths of the respondents.

Five of these problems were also covered in week 1 of the poll. Four clearly worsened in week 2. For example, the 80 percent of respondents who said the virus has had an adverse impact on how long it takes to obtain a plan review for a single-family home was up from 57 percent a week earlier. Comparisons across weeks should be interpreted cautiously, due primarily to differences in the geographic distribution of responses. In this case, however, the percentage increased significantly in each of the four Census regions.

Similarly, the 78 percent who said the virus has had an adverse impact on how long it takes the local building department to respond to a request for an inspection was up from 50 percent a week earlier. Again, the increase was present and significant in each of the four regions.

As mentioned above, problems with willingness of workers and subs to report to a construction site were less widespread than the other items on the list, but the 64 percent who cited it as a virus-induced problem in week 2 was nevertheless up from 42 percent a week earlier. Again, the rising trend was consistent across regions.

Even a decline in the traffic of prospective buyers, the most widespread problem in week 1 of the poll, was more widespread in week 2. The incidence of the problem increased in every region except the Northeast. The Northeast, however, showed a marked increase (from 57 to 73 percent) in the share reporting that the virus had a major, rather than minor, adverse impact on traffic.

The trend was not completely consistent across regions for the fifth item present in both weeks of the poll: supply of building products and materials. Although the overall share reporting this as a virus-induced problem was up, this was primarily due to a particularly strong increase (from 45 to 74 percent) in the Midwest. For additional details—including tables for each question broken down by respondents’ region, primary business, and position in the company—please see the full survey report.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.33 percent.

“Mortgage rates have drifted down for two weeks in a row and that drop reflects improvements in market liquidity and sentiment,” said Sam Khater, Freddie Mac’s Chief Economist. “While the market has stabilized relative to prior weeks, homebuyer demand has declined in response to current economic conditions. The good news is that the pending economic stimulus is on the way and will provide support for both consumers and businesses.”

News Facts

30-year fixed-rate mortgage averaged 3.33 percent with an average 0.7 point for the week ending April 2, 2020, down from last week when it averaged 3.50 percent. A year ago at this time, the 30-year FRM averaged 4.08 percent.

15-year fixed-rate mortgage averaged 2.82 percent with an average 0.6 point, down from last week when it averaged 2.92 percent. A year ago at this time, the 15-year FRM averaged 3.56 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.40 percent with an average 0.3 point, up from last week when it averaged 3.34 percent. A year ago at this time, the 5-year ARM averaged 3.66 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

National home prices continued to increase over the first month of 2020, prior to coronavirus outbreak. Price growth will certainly decline as future months’ data is recorded.

The S&P CoreLogic Case-Shiller U.S. National Home Price Index, reported by S&P Dow Jones Indices, rose at a seasonally adjusted annual growth rate of 6.2% in January, faster than a 5.3% increase in December. It was the highest gain since February 2018. On a year-over-year basis, the S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index posted a 3.9% annual gain in January, up from 3.7% in December. Going forward, national home prices are expected to increase at a slower pace due to the 2020 downturn.

Meanwhile, the Home Price Index, released by the Federal Housing Finance Agency (FHFA), rose at a seasonally adjusted annual rate of 4.1% in January, following a 9.1% increase in December. On a year-over-year basis, the FHFA Home Price NSA Index rose by 5.2% in January, after an increase of 5.4% in December.

In addition to tracking home price changes nationwide, S&P also reported on the site of vpnicon the home price indexes across 20 metro areas. In January, local home prices varied and their annual growth rates ranged from -3.6% to 13.0%. Among the 20 metro areas, eight metro areas exceeded the national average of 6.2%. Seattle, Las Vegas and Phoenix had the highest home price appreciation in January. Seattle reported a 13.0% increase, followed by Las Vegas with an 8.5% increase and Phoenix with an 8.3% increase. Home prices in two metro areas declined in January. They were Chicago (-3.6%) and New York (-1.2%).