via reelseo.com

No organization cares about you. Organizations aren't capable of this.

Your bank, certainly, doesn't care. Neither does your HMO or even your car dealer. It's amazing to me that people are surprised to discover this fact.

People, on the other hand, are perfectly capable of caring. It's part of being a human. It's only when organizational demands and regulations get in the way that the caring fades.

If you want to build a caring organization, you need to fill it with caring people and then get out of their way. When your organization punishes people for caring, don't be surprised when people stop caring.

When you free your employees to act like people (as opposed to cogs in a profit-maximizing efficient machine) then the caring can't help but happen.

Welcome to the new Friday Email Review Series. If you’ve missed the reviews from the last few weeks, you can see all past Email Review blog posts here. Not sure what I’m talking about? Learn more about the free Email Review’s in this blog post.

Also, I’m always taking submissions. Be sure to fill out the webform and send in your email to be reviewed next week.

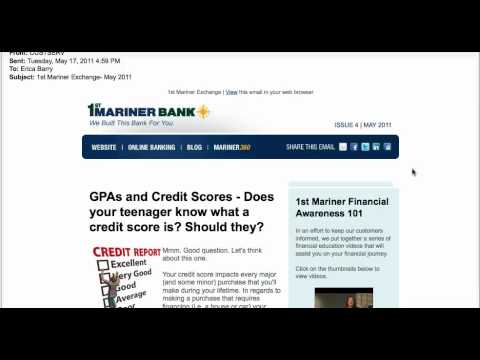

Today’s Email Review screencast is Blue Sky Factory client, 1st Mariner Bank. Be sure to follow them on Twitter (@1stmarinerbank) where they talk banking and engage with their followers. Also, they are quite active on Facebook, posting timely articles and other banking information.

The 5-minute Email Review screencast is below.

Having trouble seeing? Try going directly to YouTube.

7 Takeways & Suggestions For 1st Mariner Bank

The following points were all covered in the screencast above, but for those that like them written out, see below:

- Design For Images Off: Remember that most email clients have images off by default. 1st Mariner Bank does a great job designing this email to render nicely with images off. Once I enabled images, you’ll notice that the pictures enhanced the email, but were not critical to the overall design.

- A|B Test Subject Lines: The subject line that 1st Mariner Bank chose, 1st Mariner Exchange-May 2011, was a bit bland. That being said, it doesn’t really matter what I think. Let the data dictate the best subject line. Or, you could also use a combination of Google’s Wonder Wheel and their Adwords Keyword Tool in combination with an A|B test feature that most email service provider have (see some recent enhancements to Blue Sky Factory testing feature). Test. Test. Test.

- Preheader: It’s nice that they included a link to view the email online (in a browser), but don’t forget to use the preheader space for your call to action too! In this case, 1st Mariner Bank could have linked the text to their main article, increasing possible touch points (click-throughs) and driving subscribers back to their website. For more on preheaders, see slides 14-19 here.

- Share With Your Network (SWYN): First, it’s great to see 1st Mariner Bank including SWYN icons at the top of their email; however, don’t forget to give subscribers a reason to share. Why? What’s in it for me. Most specifically for this email, 1st Mariner Bank could have included the following text: “Hey Parents! Post this email to your teens’ Facebook Wall.”

- Balance: Nice balance between images, text, and links. Great touch to include a few clickable videos. By making them open in a new tab/window, 1st Mariner Bank is better able to track click-throughs.

- Test Calls To Action: I’d suggest that 1st Mariner Bank includes a few more options to click. Link the images as well and look to see how many subscribers click there. Also, try different wording on the links. Instead of linking “here” (hard to see), link more words in the sentence.

- Social Icons: I can see the icons to connect with 1st Mariner Bank on Facebook, LinkedIn, Twitter, their Blog, and Flickr. That’s great, but why? Why should I connect? What will I see on those social channels that I don’t already get in the emails?

As always, these are just my suggestions. I’m not privy to the background on this campaign, nor am I aware of any previous testing. So, take it for what it’s worth!

How about you? What did you think of this email? Do you agree with my comment? Please share below.

Want to have one of your emails reviewed for free? It’s simple. Just follow the directions here. Until next week!

DJ Waldow

Director of Community, Blue Sky FactoryAt Blue Sky Factory, we strongly believe that, if used properly, email marketing and social media go together like Batman & Robin. If effectively implemented, email marketing can power social media and social media can power email marketing.

Good news! We have an eBook that provides 16 tips to use email and social together.

What are you waiting for? Download the eBook now!

This entry was posted on Friday, May 27th, 2011 at 6:00 am and is filed under Email Review. You can follow any responses to this entry through the RSS 2.0 feed. You can leave a response, or trackback from your own site.

Tax breaks for property losses

Real Estate Tax Talk

We’ve all seen on the news that large portions of the country have been devastated by tornados and floods. Unfortunately, homeowners are not always fully insured — or insured at all — against losses due to such events. Fortunately, the Internal Revenue Service can help because uninsured casualty losses are tax deductible.

What is a casualty?

A “casualty” is damage, destruction, or loss of property due to an event that is sudden, unexpected, or unusual. Deductible casualty losses can result from many different causes, including, but not limited to:

- Earthquakes,

- Fires,

- Floods,

- Government-ordered demolition or relocation of a building that is unsafe to use because of a disaster,

- Landslides,

- Sonic booms,

- Storms, including hurricanes and tornadoes,

- Terrorist attacks,

- Vandalism, including vandalism to rental property by tenants, and

- Volcanic eruptions.

One thing all the events in the list above have in common is that they are sudden — they happen quickly. Suddenness is the hallmark of a casualty loss. Thus, loss of property due to slow, progressive deterioration is not deductible as a casualty loss.

For example, the steady weakening or deterioration of a building due to normal wind and weather conditions is not a deductible casualty loss.

When casualty losses are deductible

In the case of a home used solely for personal purposes, a casualty loss may be deducted only if:

- You itemize deductions,

- Each casualty loss exceeds $100, and

- The total of all casualties suffered during the year exceeds 10 percent of your adjusted gross income after subtracting $100 from each loss suffered.

Losses to business property are not subject to the above limitations.

Amount of casualty loss deduction

How much you may deduct depends on whether the property involved is completely destroyed or partially destroyed, and whether the loss was covered by insurance. If more than one item is damaged or destroyed, you must figure your deduction separately for each.

If your property is personal-use property or is not completely destroyed, the amount of your casualty or theft loss is the lesser of:

- Your property’s adjusted basis (usually its cost, increased or decreased by improvements and/or depreciation), or

- The decrease in fair market value of your property due to the casualty.

If your property is business or income-producing property, such as rental property, and is completely destroyed, and the fair market value of the property before the casualty is less than the adjusted basis of the property, then the amount of your loss is your adjusted basis.

The role of insurance

You may take a deduction for casualty losses to your property only if — and only to the extent that — the loss is not covered by insurance. If the loss is fully covered, you get no deduction. You can’t avoid this rule by not filing an insurance claim.

If you have insurance coverage, you must timely file a claim, even if it will result in cancellation of your policy or an increase in your premiums. If you don’t file an insurance claim, you cannot obtain a casualty loss deduction.

You must reduce the amount of your claimed casualty loss by any insurance recovery you receive or reasonably expect to receive, even if it hasn’t yet been paid. If it later turns out that you receive less insurance than you expected, you can deduct the amount the following year.

If you receive more than you expected and claimed as a casualty loss, the extra amount is included as income for the year it is received.

Disaster areas

Casualty losses are generally deductible in the year the casualty occurs. However, if you suffer a deductible casualty loss in an area that is declared a federal disaster by the president, you may elect to deduct the loss for your taxes for the previous year.

This will provide you with a quick tax refund since you’ll get back part of the tax you paid for the prior year. If you have already filed your return for the prior year, you can claim a disaster loss against that year’s income by filing an amended return.

You can determine if an area has been declared a disaster area by checking the Federal Emergency Management Administration (FEMA) website at http://www.fema.gov/news/disasters.fema.

A great deal more useful information about deducting casualty losses may be found at the IRS website at www.irs.gov.

via inman.com

Chappaqua NY Mortgage rates ease again to new 2011 low

Demand for Chappaqua NY purchase loans up slightly from year ago

Rates on fixed-rate mortgages dropped slightly this week, hitting new lows for the year, Freddie Mac said in releasing the results of its latest Primary Mortgage Market Survey.While lower rates often trigger applications for refinancing, purchase loan demand also picked up last week and was slightly stronger a year ago, a separate survey by the Mortgage Bankers Association showed.

Freddie Mac’s survey showed rates on 30-year fixed-rate mortgage averaged 4.6 percent with an average 0.7 point for the week ending May 26, down from 4.61 percent last week and 4.84 percent a year ago.

Rates on 30-year fixed-rate mortgages hit an all-time low in Freddie Mac records dating to 1971 of 4.17 percent during the week ending Nov. 11, 2010, before climbing to a 2011 high of 5.05 percent in February.

Rates on 15-year fixed rate mortgages averaged 3.78 percent with an average 0.7 point, down from 3.8 percent last week and 4.21 percent a year ago. Rates on 15-year mortgages hit an all-time low in records dating back to 1991 of 3.57 percent in November.

For 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) loans, rates averaged 3.41 percent with an average 0.5 point, down from 3.48 percent last week and 3.97 percent a year ago. The 5-year ARM hit a low in records dating to 2005 of 3.25 percent in November.

Rates on 1-year Treasury-indexed ARM loans averaged 3.11 percent with an average 0.5 point, down from 3.15 percent last week and 3.95 percent a year ago.

Looking back a week, the MBA’s weekly Mortgage Applications Survey showed applications for purchase loans climbed a seasonally adjusted 1.5 percent during the week ending May 20 compared to the week before. Purchase loan applications were up 3.1 percent from the same time a year ago.

Demand for refinancings was also up slightly, to the highest level since Dec. 10. Requests for refinancings accounted for 66.8 percent of all mortgage loan applications, the highest share since Jan. 28.

In a May 18 forecast MBA economists said they expect rates on 30-year fixed-rate mortgages to rise to an average of 5.5 percent during the final three months of this year, and continue a gradual rise to an average of 5.9 percent during the fourth quarter of 2012.