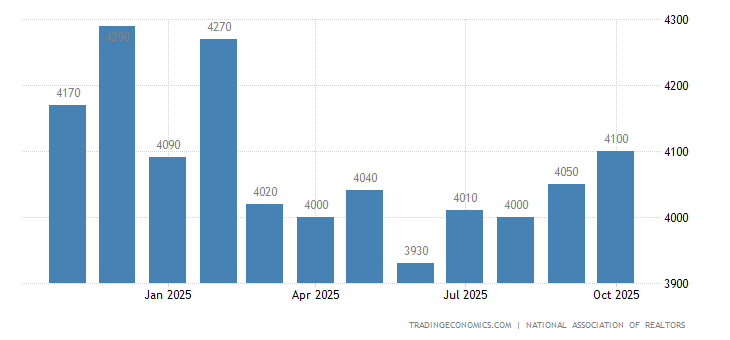

The Federal Housing Finance Agency (FHFA) found that house prices across the nation rose 16% from April 2020 to April 2021.

From March to April, house prices across the nation rose 1.8%, surpassing the previous month’s 1.6% increase.

Three regions — the Pacific coast, the western states and New England — saw more pronounced year over year increases. The FHFA index tracks seasonally-adjusted, purchase data from Fannie Mae and Freddie Mac.

In the mountain division, which includes Colorado, New Mexico, Idaho, Wyoming, Utah, Nevada, Arizona and Wyoming, house prices rose 21% year over year. In the pacific division, encompassing Washington, Oregon and California, prices rose 18%. In Maine, Vermont, New Hampshire, Massachusetts, Connecticut and Rhode Island, house prices also rose 18%.

“House prices recorded another monthly and annual record in April,” said Dr. Lynn Fisher, FHFA’s deputy director of the division of research and statistics. “This unprecedented price growth persists due to strong demand, bolstered by still-low mortgage rates, and too few homes for sale.

Mortgage rates rose above 3% for the first time in 10 weeks last week. Mortgage applications are still on the rise, however.

House prices have risen during the past year as a result of elevated lumber prices, a lack of available homes and increased demand for homes.

Lockdowns early in the pandemic led many to work from home and divide their living space into home offices. Those who were able to bought homes with more space, better suited to the pandemic remote work trend.

That has led to astonishing price increases in markets like Seattle, where the median home-sale price rose more than 26% year-over-year to a record $737,800 in May 2021. Tech employees there, faced with working remotely from cramped apartments, instead hunted for homes with more space.

“I’ve never seen anything like this housing market,” a Seattle-area Redfin agent said.

read more…

housingwire.com/articles/