New York Real Estate Predictions 2018

There’s no shortage of doom and gloom talk about a US housing crash that would take NYC down with it. In fact the recent reports of high foreclosure rates in Queens, Bronx and Staten Island are a little alarming. They’re not quite as negative though as those in other cities.

The 3rd quarter market performance was less than stellar, the worst in many years.

Yet the Trump tax bill may just rectify the foreclosure carnage even as it slowed sales and lowered property prices as investors and buyers waited it out. The wait might be over now.

Overall home prices rose above $1,000,000 and condo prices fell 11% to an average of $2,689,147. It’s the high end properties that got hit hardest. At the lower end, NYC has a full blown housing shortage.

With income averaging about $60,000 per year in New York City, it’s difficult for many to buy homes averaging $680,000. It’s estimated that to buy a home in NYC, you need an income of $100,000. New York State’s economy was a sluggish under performer in 2016, however in the last 12 months NYC has gained 68,000 jobs. In November alone, NY State grew 26,000 new jobs.

The US economy persistently grows and improves despite the terrible debt and trade deficits left by the Obama administration. The Trump Administration new Tax bill are being viewed as positive and have quietened talks of housing market and stock market crashes.

Bar any issues with trade relations, and President Trump’s recent visit to China is a good start, all should go nicely with the US housing scene and help New York recover further. It could be said that NY’s inability to create new housing has made it too expensive to live their. That scares away business and makes buyers suspicious of a NY housing crash.

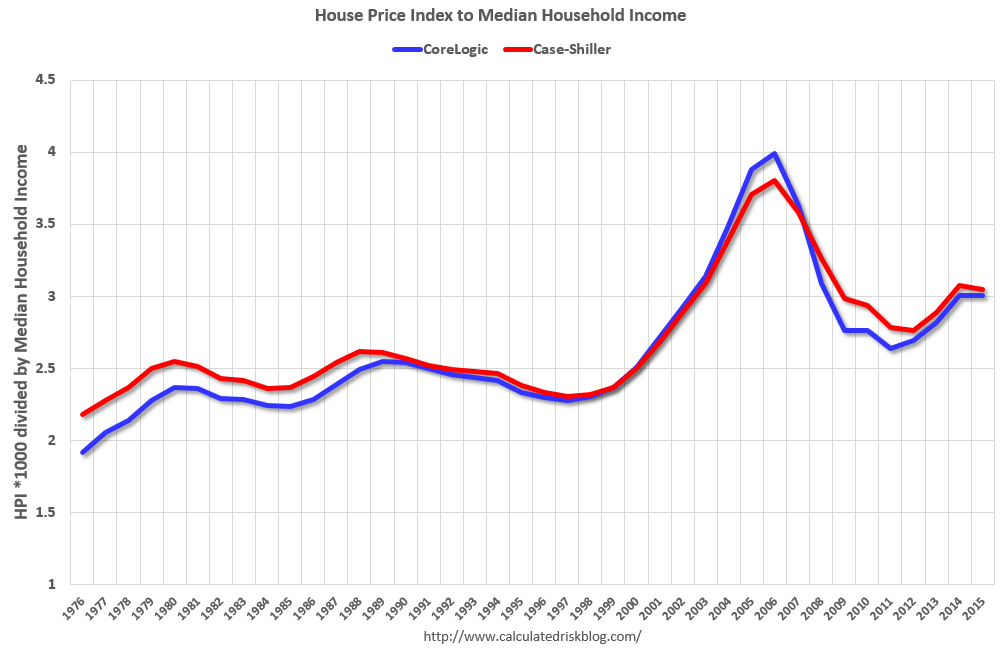

This chart below from the Case Shiller Home price index shows NYC’s real estate is stable and optimistic.

NYSAR New York Real Estate Update December

Here’s the latest New York housing stats published by NYSAR, shows the typical US housing data, that supply of affordable homes has dropped 1%, sales are down 2.5%, and average prices are up 7% from last year.

You could say that just like the San Francisco market and Los Angeles market, and all major city markets across North America, the New York housing market is under pressure. The NYC forecast is for more of the same, but at least, the market here isn’t like it is in Seattle, the Bay Area, or Los Angeles county.

It’s pretty far fetched that New York’s real estate performance could deviate too much from the US national forecast. A crash isn’t favored by the stats.

Is 2018 the right year to invest in rental income property? Contrast the stock market to investing in real estate.

Some Experts are Talkin’ Crash while Others Aren’t

There are enough media and realty pundits talking about a real estate market crash in New York soon. CNBC called from one back in the spring, but it’s not happening. Prices in Manhattan, Brooklyn, Queens, have kept rising slowly.

A Tale of Two Markets?

It’s softening in the high end luxury sector where DOM is lengthening and prices have dropped almost 1% during 2016 according to one report. But demand at the lower end has stayed strong.

New York State Realtor Association is Optimistic

NYSAR reiterated NAR Chief Economist Lawrence Yun’s keynote speech at the 2016 REALTORS® Conference & Expo in Orlando, Florida. Yun explained that younger buyers are likely to drive growth in residential markets in the years ahead as the economy stays on a positive track and interest rates stay relatively low.

Here’s the 3rd quarter market report from NYSAR. New listings are down from the previous quarter, avg/med prices are up and number of months supply has dropped 29%.

Here’s an exerpt from NYSAR’s latest new report:

“Looking ahead, the modest closed sales increases in September and the third quarter may signal that the continued decline in available homes is starting to impede closed sales growth,” MacKenzie said, noting the 20.7 % decline in homes on the market at the end of the third quarter compared to the same period in 2015. “Buyers, who are trying to take advantage of otherwise favorable market conditions, are finding fewer choices available to them causing them to delay the purchase of their next home.”

The year-to-date (Jan. 1 – Sept. 30) sales total of 95,453 was 11% above the same period last year. There were 38,629 closed sales in the 2016 third quarter, up 2.8% from the 2016 third quarter total of 37,575. September 2016 closed sales increased 2.1%compared to a year ago to reach 11,780.

The New York Building Congress Forecast 2017 to 2018

Calls for $127.5 Billion in Total Spending Through 2018. 2016 was a record year for housing sales and jumped past the $40 billion mark for the first time. NYBC also forecasts a total of 147,100 jobs in NY’s 5 boroughs in 2016, an increase of 8,900 jobs from 2015 but will fall a few percent to 142,600 jobs in 2017 and 138,100 in 2018.

These screen caps are from HUD’s Comprehensive Housing Market Analysis of New York City, NY. New York’s economy was rolling along nicely.

Is that forecasted softening in employment enough to cause a crash?

The Building Congress’s outlook for new home construction is 27,000 new units and $13.1 billion of residential spending in 2017, and 25,000 units and $12.7 billion in spending in 2018. That’s down significantly from the 36,000 units built in 2015. With nowhere to live we can expect residents new and old to bid on resale stock and that should keep home prices level.

Donald Trump did make an election promise to cut government spending and tax the wealthy and that could make an impact, yet it appears private demand is what is driving the economy right now.

Removal of the Dodd Frank noose and easing of mortgage lending should create more demand for homes in New York, Los Angeles, Boston, Seattle, Houston, SF Bay Area, Miami, and well, every US city. If land development regulations are eased, it will allow for more home construction and help to ease the auctions atmosphere that has rocketed them upward.

It’s a health forecast with strong demand, stable mortgage rates, looser rules on financing, and a government bent on creating jobs in 2018 to 2020. Full speed ahead.

read more…