A working paper just released by the Federal Housing Finance Agency (FHFA) attempts to determine the reasons why mortgages given to first-time homebuyers perform more poorly than those given to repeat buyers. The Marginal Effect of First-Time Homebuyer Status on Mortgage Default and Prepayment was written by Saty Patrabansh of FHFA’s Office of Policy Analysis and Research.

Given that homeownership is generally considered a societal benefit and that many government policies focus on incentivizing first-time buyers the author says it is important to understand whether first-time buyers as a group are likely to default at higher rates than repeat buyers both in order to anticipate that an increase in the rate of first-time homeownership could lead to increased foreclosures and negatively affect communities and because, if they do not default at higher rates it is important they not be treated as more risky buyers.

Earlier studies that touched on various aspects of first time homeownership and loan performance have generally used data from FHA guaranteed loans and were not designed specifically to study first-time buyers. The FHFA study developed a modeling approach specifically to discuss first-time buyer loan performance based on data on Fannie Mae and Freddie Mac (the GSEs) originated mortgages. The study sought answers to two questions: (1) do first-time homebuyer mortgages perform worse than those of repeat homebuyers? And (2) do any differences persist when borrower, loan, and property characteristics known at the time of origination are held constant?

Differences in overall loan performance between first-time and repeat homebuyers could be driven by differences in borrower, loan or property factors. Each of these can be refined into sub-factors. Borrower factors can be further classified as sophistication, endurance, and intentions. A sophisticated or experienced borrower may find ways to keep mortgages current when faced with trigger events such as going “underwater” on a loan while a less sophisticated buyer make lack that ability. Likewise an experienced borrower may have a greater tendency to default strategically when events appear to warrant it. To the extent first-time buyers are less experienced or sophisticated than repeat buyers they can be expected to default at a higher rate and prepay at a lower rate.

Borrower financial endurance can determine the borrowers’ capacity to withstand a trigger event such as by refinancing. Borrower intentions may determine if homeowners default strategically without a trigger event or fail to refinance even with the capacity to do so.

Loan factors can further classified as those of the product or the institution, Subprime and non-traditionalproducts could default at a higher rate; mortgages with prepayment penalties are less likely to be refinanced. Loan institutions such as guarantors and services affect performance by their programs and policies.

Property characteristics can have sub-factors such as property quality (properties in poorer condition can tax borrower financial strength) and property location (economic conditions may affect one location more than others.) To the extent that first-time homebuyers chose certain loan products, property quality, or location to a greater degree than repeat buyers may impact their loan performance as a group.

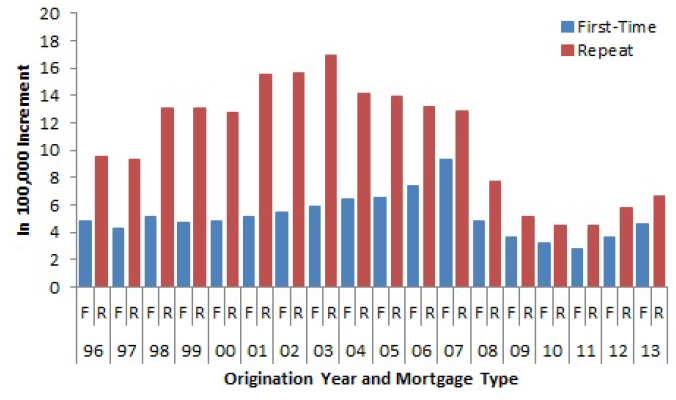

First-time homebuyers are younger as a group than repeat homebuyers and the difference in median age between the two groups steadily increased from 6 years in 1996 to 10 years in 2012. First-timers are more likely to borrower as individuals, perhaps because they are unmarried, and earn a median monthly income that was lower by about $700 compared to repeat buyers in 1996 and by around $2,000 less in 2012. Their median credit scores and the loan-to-value (LTV) ratios of their loans were lower as well. Their payment to income ratios averaged 2 to 4 points higher than repeat buyers but their debt-to-income (DTI) ratios were comparable.

read more…

http://www.mortgagenewsdaily.com/07102015