If you wanted to buy every single home in the country, all at once, you’d need to be prepared to spend more than $25 trillion, according to Zillow.

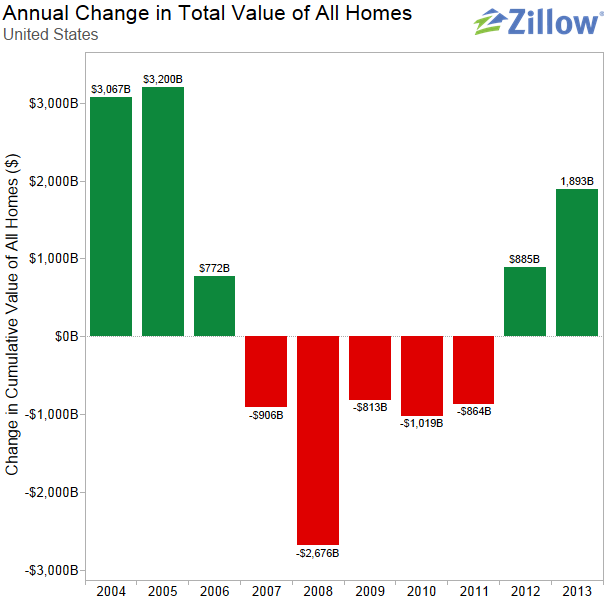

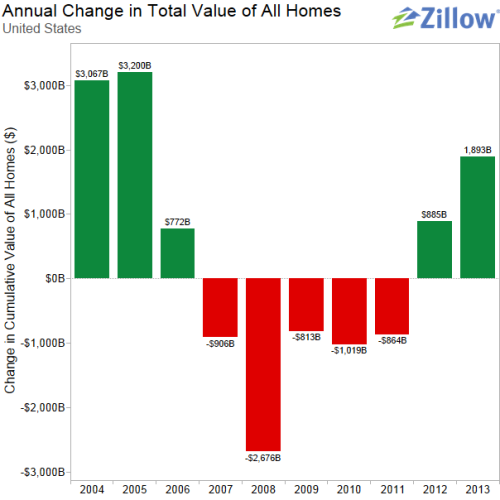

The overall cumulative value of all homes in the U.S. at the end of 2013 is expected to be approximately $25.7 trillion, up almost $1.9 trillion, or 7.9 percent, from the end of 2012. Gains were calculated by measuring the difference between cumulative home values as of the end of 2012 and anticipated cumulative home values at the end of 2013.

The gain in cumulative home values is the second annual gain in a row, after home values fell every year from 2007 through 2011. Between 2007 and 2011, the total value of the U.S. housing stock fell by $6.3 trillion. Over the past two years, U.S. homes have gained back $2.8 trillion, or about 44 percent of the total value lost during the recession.

“In 2013, the housing market continued to build on the positive momentum that began in 2012, after the housing market bottomed. Low mortgage rates and an improving economy helped bring buyers into the market, boosting demand and driving prices up,” said Zillow Chief Economist Stan Humphries. “We expect these gains to continue into next year, though at a slower pace. The housing market is transitioning away from the robust bounce off the bottom we’ve been seeing, toward a more sustainable, healthier market. This will result in annual appreciation closer to historic norms of between 3 percent and 5 percent.”

Real estate in the United States is hugely valuable. The $25.7 trillion total value of the country’s entire housing stock is more than the combined gross domestic products (GDP) of China and the U.S. in 2012. Homes in the New York and Los Angeles markets alone account for more than $4 trillion in combined value.

The chart below shows how much the total housing stock in each of the country’s 30 largest metros is expected to be worth at the end of this year.

| METRO | Projected Value, All Homes Year-End 2013 | Projected Home Value Gain/(Loss) 2013 | Home Value Gain/(Loss) 2012 |

| United States | $25.7 trillion | $1.89 trillion | $885 billion |

| New York, NY | $1.9 trillion | $123.1 billion | ($3.5 billion) |

| Los Angeles, CA | $2.2 trillion | $323.1 billion | $117.8 billion |

| Chicago, IL | $687.5 billion | $58.6 billion | ($8 billion) |

| Dallas-Fort Worth, TX | $339.5 billion | $18.7 billion | $17.8 billion |

| Philadelphia, PA | $540.5 billion | $19.5 billion | ($6.7 billion) |

| Houston, TX | $307.2 billion | $18.7 billion | $6.4 billion |

| Washington, DC | $890.3 billion | $64.5 billion | $26.1 billion |

| Miami-Fort Lauderdale, FL | $646.8 billion | $83.3 billion | $49.5 billion |

| Atlanta, GA | $332 billion | $39.1 billion | $869.5 million |

| Boston, MA | $568.5 billion | $45.6 billion | $20.1 billion |

| San Francisco, CA | $987.2 billion | $159.2 billion | $87.7 billion |

| Detroit, MI | $247.2 billion | $33.5 billion | $19.6 billion |

| Riverside, CA | $370.1 billion | $71.5 billion | $20.1 billion |

| Phoenix, AZ | $383.5 billion | $36.1 billion | $59.6 billion |

| Seattle, WA | $427.8 billion | $43.6 billion | $22.7 billion |

| Minneapolis-St Paul, MN | $281.4 billion | $25.4 billion | $18 billion |

| San Diego, CA | $507.5 billion | $71.5 billion | $32 billion |

| St. Louis, MO | $170.5 billion | $2.4 billion | $4.6 billion |

| Tampa, FL | $204.5 billion | $25.7 billion | $10.2 billion |

| Baltimore, MD | $302.7 billion | $14.5 billion | $2.4 billion |

| Denver, CO | $265.1 billion | $21.9 billion | $18.6 billion |

| Pittsburgh, PA | $131.2 billion | $6.6 billion | $2.8 billion |

| Portland, OR | $216.7 billion | $22.8 billion | $10.1 billion |

| Sacramento, CA | $236.9 billion | $40.7 billion | $16.4 billion |

| San Antonio, TX | $107 billion | $1.9 billion | ($3.5 billion) |

| Orlando, FL | $149 billion | $21.3 billion | $8.7 billion |

| Cincinnati, OH | $115.7 billion | $5.7 billion | $420.5 million |

| Cleveland, OH | $105.4 billion | $3.3 billion | $942.1 million |

| Kansas City, MO | $115.6 billion | $2 billion | $1.9 billion |

| Las Vegas, NV | $146.7 billion | $31.4 billion | $10.8 billion |

2. Crooked photos of the inside or outside of the home. Most everyone has a photo editor that will automatically straighten your photo. Use it.

2. Crooked photos of the inside or outside of the home. Most everyone has a photo editor that will automatically straighten your photo. Use it.