WHITE PLAINS—Home sale prices were up sharply in the third quarter in the four-county market area of the Hudson Gateway Association of Realtors, with the exception of Westchester County where sales prices were relatively flat as compared to a year earlier.

Sales volume was off marginally throughout the region, with overall third quarter sales down 5.2% in Westchester; 1.8% in Orange and 1.2% in Rockland, while Putnam County’s sales numbers were flat with an increase of 0.3%.

Market results were mixed depending on product type and location. Realtors interviewed by Real Estate In-Depth said that while some negative market influences, specifically the cap on SALT deductions, low inventory and higher interest rates, may be impacting some buying decisions, it is way too early to tell just what real impacts they will have on the market going forward.

Westchester County posted a third quarter median sale price for a single-family home of $679,000, which was slightly lower than the third quarter of 2017 ($680,000). The median sale price for a single-family home in Putnam was $360,000, up 5.9% from the third quarter of 2017; the median sale price in Rockland was $475,000, up 6.7% and the Orange County median was $275,000, up 7.8%.

Hudson Valley Home Sales—Third Quarter 2018

County Change from 2017 Putnam +0.3% Rockland -1.2% Orange -1.8% Westchester -5.2%

Paul Breunich, president and CEO of William Pitt and Julia B. Fee Sotheby’s International Real Estate, said in connection with the Westchester County market that the declining sales numbers, while noteworthy, are not a sign of a troubled market. He insisted that the market appears to be in transition and that most market observers expect home sales to fall between 4% to 6% for the year countywide.

“The market is in an adjustment period and is in flux,” Breunich said. “With what is going on in the economy—the stock market, GDP, (low) unemployment and consumer confidence through the roof, that is all pointing to a very strong, healthy real estate market, but that is not being reflected in our marketplace, yet.”

Breunich said that he is concerned about consumer market perceptions of a severe downtown in Westchester home sales based on erroneous sales numbers released recently by a local brokerage firm that garnered national media coverage.

“These news stories have contributed toward an exaggerated negative narrative about the state of the real estate market in Westchester, spreading misinformation and miseducating consumers,” Julia B. Fee Sotheby’s stated in its third quarter market report on Westchester County. “The actual picture is dramatically different, according to our own analysis, and varies greatly by town and price range.”

He noted that the market is seeing a decline in sales, but not double digits as was erroneously reported in the press. He also said that some locations are stronger than others both in terms of home sales volume and pricing.

“You have to look at the reality of it,” Breunich said. “The market is still down five to six percentage points. That is not something to pull the fire alarm on about, but it is something to be aware of.”

He added that the federal tax reform law and the cap on SALT deductions might be having some impact on demand. However, there are other factors that influence demand, such as high consumer confidence and the strong economy, for example, and the market is working through all the factors, both positive and negative.

While bullish on the future of the Westchester County residential market, Breunich said the real estate market is no longer booming, but is in transition. He said it is too early to tell the true impact of federal tax reform and added that the first indications of its effect on the market will likely show up in the next six months or so when people file their taxes in the spring of 2019.

Joseph Rand, managing partner of Better Homes and Gardens Rand Realty, said the federal tax reform might be having a small impact on the very high end of the market where the loss of deductibility for mortgage interest and local taxes hits the hardest.

He noted that price appreciation was more pronounced in the lower‐priced markets.

In terms of the loss of the SALT deductions, he said, “We’re talking about a marginal, not a major, impact. Prices aren’t rising at the rate they are in the lower‐priced markets, they’re basically flat, not falling.”

A plus for the marketplace is that inventory levels are starting to respond to rising prices, noting that for the first time since 2012, inventory levels went up in the third quarter.

Rand noted the what is happening region wide is that after years of decline, single-family inventory was higher in almost every county in the region, stabilizing near that six‐month level that usually signals a balancing market. This market phenomenon occurs when demand is strong, and supply stays steady (or goes down) and prices go up. In response to the rising prices, eventually new inventory comes onto the market, he explained.

“Going forward, we believe that the appetite in the market can handle both the impact of tax reform and this increased inventory while still driving continued price appreciation,” Rand said. “With strong economic conditions, relatively low‐interest rates (and the specter of rate increases on the horizon), and pricing still at attractive 2004‐05 levels, we expect a robust market through the end of the year.”

Brokerage network Westchester Real Estate Inc. in its third quarter market report on Westchester County also discussed the positive and negative economic and regulatory forces affecting the housing market.

The firm concluded that with those forces factored it, it believes, “Westchester properties will always remain in high demand based on our proximity to NYC and fantastic quality of life. While we may see pullbacks or shifts at times, our housing market possesses innate strength and resilience. Prices are not decreasing, home sales are still strong, and Westchester’s real estate market is just fine!”

Residential construction goods input prices reversed course in September, increasing 0.2% after declining each of the prior two months, according to the latest Producer Price Index (PPI) release by the Bureau of Labor Statistics. The index for inputs to residential construction has risen 5.2% in 2018 and is 10.2% higher than it was in January 2017.

Gypsum prices also reversed trend in September, falling 0.1% (seasonally adjusted) after a combined increase of 6.1% over the prior two months. Since the start of the year, the price index for gypsum products has increased 1.0% per month, on average.

From January to September of 2017, prices paid for gypsum products rose 7.2%. The index has increased 8.1% over the same period in 2018.

The September PPI release continued to capture decreases in prices paid for softwood lumber that began in mid-June. However, even after accounting for the most recent price movements, the average price paid for softwood lumber in 2018 remains the highest on record according to Random Lengths data—18.7% above the prior record set in 1997.

The index for prices paid for OSB (and waferboard) decreased for the second consecutive month (-5.2%, not seasonally adjusted). Prices are down 16.4% since July and have declined in five of the past 12 months.

The index for ready-mix concrete (RMC) prices increased 0.4% (seasonally adjusted), reversing a four-month trend of price declines. After an uncharacteristically large monthly increase in March—when the index rose 3.3%–the PPI for RMC has fallen back in line with its long-run trend.

September 2018 marked the first time in eight months that U.S. multifamily rents did not increase. The $1,412 national average for the month represented a $1 drop from August and a 3.1% year-to-date increase; year-over-year rent growth remained unchanged at 3%, according to a survey of 127 markets by Yardi® Matrix.

The report presents an overall bright outlook for the multifamily sector. A slight decline in rents is normal at the start of fall, it says, “When rent growth traditionally begins to hibernate for winter.” Strong demand countering the steady wave of new supply is another positive sign. “Long-term demand for rentals is likely to remain high for a variety of demographic and social reasons,” the report notes.

Year-over-year rent growth leaders for September were Orlando, Fla.; Las Vegas; Phoenix; Tampa, Fla.; and California’sInland Empire.

View the full Yardi Matrix Multifamily National Report for September 2018 for additional detail and insight into 127 major U.S. real estate markets.

With the current stock market bull run reaching nearly 10 years in length, it’s understandable that many investors are nervous about the end of the party coming sooner than later.

However, as UBS notes in its latest report, there is also growing concern about another prominent bubble that’s been in the works since the aftermath of the financial crisis.

Large amounts of easy money have fueled real estate bubbles in the world’s major cities – and the Swiss investment bank now sees the property markets in six global cities as being at risk.

THE BUBBLE INDEX

In the 2018 edition of the bank’s Real Estate Bubble Index, here are the major cities around the globe that are in or near bubble territory:

Any city with a score over 1.5 is considered at “Bubble Risk”, and right now those include two cities from Canada, one from Asia, and three from Europe.

Hong Kong (2.03) tops the index this year, leaping past Munich (1.99), Toronto (1.95), and Vancouver (1.92) which all remain at bubble risk themselves. Amsterdam and London are the two other cities that score higher than a 1.5 on the rankings.

It’s also very important to note that there are four cities that score just under the 1.5 threshold: Stockholm (1.45), Paris (1.44), San Francisco (1.44), and Frankfurt (1.43).

A COMING CORRECTION?

Investor and writer Howard Marks has noted in recent months that the wider market is in its “8th inning”, and the same case could be made for real estate.

Historically, investors have had to be alert to rising interest rates, which have served as the main trigger of corrections.

– UBS Report

According to UBS, the cracks are already starting to show at the top end of the market, with housing prices declining in half of last year’s list of bubble cities. Some of the worrying factors include rising interest rates, as well as growing political tensions as the crisis of affordability makes it harder for average people to live in these global financial centers.

Here is annualized growth in percent over the last year, as well for the last five years for cities in the index:

As you can see, some of these cities have had negative growth over the last 12 months, including New York, Toronto, Sydney, London, and Stockholm.

CHARTING SPECIFIC MARKETS

In Hong Kong, you need to work 22 years to afford a 645 sq. ft (60m²) apartment, when that took just 12 years just a decade ago. In recent years, Hong Kong’s ascent to becoming one of the biggest real estate bubbles has become very evident, especially when juxtaposed with Singapore:

In Canada, the two cities in the index are starting to go in alternate directions, although recent signs also point to a potential slowdown in Vancouver:

Finally, the U.S. market – which felt the pain of the housing crash in the late 2000s – is home to zero cities in the bubble risk category, according to UBS.

Whether it is a bubble or not, many people agree that San Francisco’s housing situation is still a crisis. In the Bay Area hub, 60% of all rental units are in rental-controlled buildings, and the median single-family house price is a hefty $1.7 million.

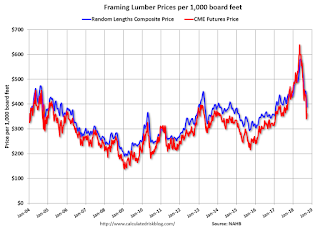

Here is another monthly update on framing lumber prices. Lumber prices declined further in September from the recent record highs, and are now down year-over-year.

This graph shows two measures of lumber prices: 1) Framing Lumber from Random Lengths through October 5, 2018 (via NAHB), and 2) CME framing futures.

Right now Random Lengths prices are down 12% from a year ago, and CME futures are also down 12% year-over-year.

There is a seasonal pattern for lumber prices. Prices frequently peak around May, and bottom around October or November – although there is quite a bit of seasonal variability.

From the largest publicly traded production firms to small local companies, home builders are at the epicenter of many of today’s most pressing political issues. Across the U.S., residential building pros deal with some of the country’s biggest challenges and opportunities: immigration, taxes, environmental regulations, banking, and Wall Street reform, to name just a few.

Home building’s reach into so many aspects of the nation’s economic health makes the industry a powerful force in U.S. political affairs, and housing issues impact the country in myriad ways, says Jim Tobin, the NAHB’s executive vice president for government affairs and chief lobbyist. “There are home builders in every district in every state. We’re important to the tax base. We offer jobs,” he says. “And our members are community leaders who aren’t just providing shelter, they’re providing stability and community leadership.” (Click here for a list of the top political issues facing builders this year.)

November’s midterm elections will help to shape these issues, and the stakes are high: Up for grabs is the entire House of Representatives, a third of the Senate, and 36 governorships. In what many political insiders consider a bellwether year for U.S. politics, home builders plan to make their voices heard. A recent BUILDER poll found that nearly 99% of respondents said they plan to vote in the upcoming elections, and more than three-quarters of them said home building–related issues will play a large role in their decisionmaking.

Before U.S. builders hit the polls they’ll have to sort through the current political climate, with its rampant party extremism, constantly changing balances of power, robust regulatory environment, and Supreme Court upheaval. In such uncertain times, many will look for guidance from the NAHB, which has long lobbied on behalf of the industry and, in 2016, began to support and endorse political candidates for Congress. (It does not endorse candidates at local or presidential levels).

Tracking the Industry Founded in 1942, the NAHB’s mission is “to protect the American dream of housing opportunities for all, while working to achieve professional success for its members who build communities, create jobs, and strengthen our economy.” The association’s members construct about 80% of the new homes built in the U.S. every year, and the federation has more than 800 state and local associations throughout the country.

NAHB lobbies on topics from forest management to energy policy, and it issues statements on initiatives from tariffs and codes to Supreme Court justice changes. Staff members also keep tabs on what’s going on in government agencies that deal with housing—a total of 160 federal housing programs administered by 20 different entities at a cost of over $160 million each year, according to independent educational nonprofit Restore Accountability.

The association has a seat at the table at nearly every level of the legislative process, all the way up to the executive office. For instance, when President Donald Trump recently signed an executive order telling the EPA and Army Corps of Engineers to rescind or revise the Waters of the United States (WOTUS) rule, then-NAHB chairman of the board Granger MacDonald was by his side. In fact, it’s said that politicians ignore the home building industry at their peril; one Fox News announcer recently quipped that he’d rather have the NAHB with him than against him.

Tobin and his team of 10 lobbyists and 20 government affairs staffers are the soldiers who navigate the tricky terrain in the nation’s capital, working with regulatory agencies such as HUD and the EPA, the White House, and the judiciary on behalf of NAHB’s members. Keeping track of so many issues is no small task, Tobin says. “So many things impact the ability to develop housing in America,” he says.

Tobin starts his day by absorbing what’s driving the news cycle—sometimes a statement from House Minority Leader Nancy Pelosi, often a presidential tweet. After internal strategy meetings at the NAHB’s National Housing Center in downtown D.C., just a few blocks from the K Street hub where Beltway lobby shops have traditionally clustered, Tobin treks over to Capitol Hill or the White House for meetings with members of Congress who could either sign or block legislation on everything from banking regulations to environmental protection. On any given day, Tobin’s team can be tracking 100 different bills.

Al Diaz/Miami Herald/TNS via Getty ImagesDonald Trump addresses NAHB members in Miami Beach, Fla., during his 2016 presidential campaign.

“Everything is almost a No. 1 priority when it comes up,” Tobin says. NAHB staff looks at every piece of legislation and change in regulations as soon as it is released and takes immediate action, no matter how unlikely it is to become law. If a bill were introduced to cut the mortgage-interest deduction in half, for example, Tobin’s team would be on it. “There’s no way that bill would make it through Congress, but we will take that bill with one co-sponsor, send a letter, lobby against it, and make sure there are several nails in that coffin so it never sees the light of day,” Tobin explains.

Although many might imagine Tobin having lunch or dinner meetings with members of Congress, those haven’t really been a thing since the 1990s, when a wave of reforms prohibited lobbyists from buying a senator or representative lunch—or anything else, for that matter. Meals at Capitol Hill meeting place Charlie Palmer Steak have been replaced by fundraising events, where Tobin says he can “access members of Congress to talk about current events, what you’re working on, in a smaller setting.”

These days, texts and messages are most congressional staffers’ preferred method of communication, Tobin says, and it better be quick. “You have to boil it down to a page, or a half page. People are busier and attention spans are shorter today,” he says. “Nothing will ever replace shoe-leather lobbying and relationships, but with the fast pace of Capitol Hill and a greater flow of information, Hill staff may not have the time to take a meeting, so you need to know how to get your points across.”

Every two years, Tobin and his staff prepare for shifting sands in Washington, D.C. If Democrats take over the House in the upcoming elections as some predict, Tobin’s staff will need to know the priorities of the new leadership and discern how they fit in with the NAHB’s agenda. “We’re always war gaming what the next two years are going to be based on what the current situation looks like,” he notes.

NAHB works closely with the Mortgage Bankers Association and the National Association of Realtors—a trifecta that Tobin calls “the big three of housing”—and sometimes with the National Multifamily Housing Council, the Associated General Contractors of America, and the U.S. Chamber of Commerce (the latter being the biggest spender on federal lobbying, paying out $22.9 million in the first quarter of 2018, according to Roll Call). “Sometimes we’re opposite them,” Tobin says. “But at the end of the day, if we can find like-minded associations to join the coalition, the more the merrier.”

Grassroots Efforts NAHB’s lobbying efforts are determined by senior officers who represent the nearly 2,500 members who serve on the association’s board of directors, in turn representing NAHB’s 140,000 members. NAHB relies on its members to provide relationships with elected officials, which is why it created the Bringing Housing Home program to develop opportunities for its members to meet with congressional delegations. Local NAHB leaders are encouraged to schedule meetings with their senators and representatives during congressional recesses. NAHB members held hundreds of these meetings across the nation this spring and summer.

“There’s an old saying that most people don’t approve of Congress, but they approve of their member of Congress,” says Michael Everngam, vice president of BUILD-PAC, NAHB’s political action committee that serves to raise and distribute funds for pro-housing candidates. “I think that saying goes a long way. When we do have major issues come up, members are more likely to get involved and talk to their member of Congress because they’ve been involved along the way.”

Courtesy Kevin WoodwardHome builder Kevin Woodward (third from left) and other NAHB members meet with Tennessee U.S. Rep. Scott DesJarlais (fifth from right).

Home builder Kevin Woodward has seen the importance of one-on-one political involvement. Early in his career, the managing partner for Legacy Homes in Nashvillerealized that laws and regulations could make or break his industry and saw that the only way to have any control over them was to get involved in the political process. For decades, Woodward has been part of lobbying efforts, serving twice as state president of the NAHB in Nebraska and three times in Tennessee. He has also been on numerous NAHB committees and is currently the third vice chair of the NAHB’s BUILD-PAC, meaning he will be chair in two years.

If Woodward has learned anything during his experience, it’s that nurturing relationships in the cities and districts where he lives is his most important contribution. “If we don’t participate at a local level, we’re never going to get anything done at a national level,” Woodward says. “What I have done and encourage others to do is meet with local officials, state legislators, and national legislators. Build relationships that will eventually blossom into the ability to reach out to them, so when you call them, they’ll actually answer.”

NAHB offers an advocacy app with an interactive congressional directory to keep members informed of housing news, statistics, and talking points on key issues, but most use “the old-fashioned way of communication—texts, phone calls, and emails—for our calls to action,” Woodward says. When issues come up, NAHB Board of Trustees members send a directive to state leaders, who disseminate the information and enlist help from members.

“They’re just a phenomenal government affairs staff at NAHB,” Woodward says. “They may send us a directive, and we’ll say, ‘Well, why?’ But they’re the experts in the field, and if they send us down a path, they have a reason. They’re in it 24/7/365. We’re involved much less. My job is to build houses.”

For example, when the NAHB asked local leaders in the spring to recruit members of Congress to sign a letter urging the Trump administration to restart lumber trade talks with Canada, Woodward sprang to action. He called all nine of Tennessee’s U.S. representatives and its two senators, then he called local members around the state who know key legislators, asking them to make calls and report back. If they didn’t, he called again—and his tenacity paid off. Seven of Tennessee’s nine representatives, including politically invaluable House Ways and Means member Diane Black, signed the letter. “Two we knew would not,” Woodward says. “That’s just politics.”

Pro-Housing Outreach While NAHB’s government affairs office steers the ship in Washington, members back home truly drive the organization, says vice president for intergovernmental affairs Karl Eckhart, who oversees NAHB’s grassroots efforts. When members asked for more ways to support pro-housing candidates aside from BUILD-PAC, the association delivered. In 2016, NAHB made its first endorsements of 139 congressional candidates—94% of whom won their races—and launched the Defender of Housing Award for U.S. senators and representatives who have offered unwavering support for the housing sector. NAHB members have given 268 awards so far.

“We want our endorsements and the award to be meaningful,” Tobin says. “We want members of Congress who don’t get an award or endorsement to come to us and say, ‘What do I have to do to get that award? Let’s find areas where we can work together.’”

The criteria for what constitutes a pro-housing candidate takes many factors into consideration, and the selection process is intense. Woodward and other state leaders spend hours scouring candidates’ records and talking with people about congressional members and candidates before they offer a Defender of Housing award, donation, or endorsement.

“When we examine the housing bona fides of a candidate or a member of Congress we look for people that, first and foremost, are supportive of housing and creating conditions for greater housing affordability,” Tobin explains. “We’re looking for people who have relationships with their local home builders and meet regularly to discuss housing issues back home in their communities. We back candidates that support and promote policies of increasing ownership and rental opportunities, reducing regulatory costs, and creating an economic environment where small businesses can be successful. Housing is a bipartisan, middle-of-the-political-spectrum issue. Candidates that work to advance common-sense, bipartisan solutions to complex issues tend to earn NAHB’s support.”

A candidate’s chance of being elected also comes into play, Woodward says, because you want funding to go to candidates who will be in a position to help advance the association’s agenda. “Our PAC money is not a secret,” he says. “Anybody can find out who we give it to. If you keep throwing money at the wrong place, you’re never going to be able to succeed.”

One politician who has earned NAHB’s support is Rep. Keith Rothfus, a PennsylvaniaRepublican who was recently named a Defender of Housing. In Rothfus’ district, the home building industry employs 130,000 people and drives other industries such as raw materials, design services, and furniture sales, and he’s fierce about making sure home builders can do business unencumbered. He’s a vocal opponent of over-regulation, particularly when it comes to community banks, and as vice chairman of the Subcommittee on Financial Institutions and Consumer Credit and a member of the Financial Services Committee, he has some sway.

Rothfus is constantly in touch with builders, real estate agents, community bankers, and other stakeholders in the home building industry in his district, and he consistently votes the pro-housing party line. “It’s very important that we continue to have feedback from the various players,” he says. “It’s very important for us to stay in touch and hear their pressure points as they continue to offer jobs to people.”

Beyond Party Lines As influential as the home building industry is in Washington, it’s not immune to the fact that money talks. Completely funded by donations from more than 2,700 members, the association’s BUILD-PAC has more than $3 million to spend this election cycle, and Tobin plans to use every dime. The Center for Responsive Politics, which tracks PAC spending, shows that as of Aug. 21, BUILD-PAC had contributed $979,000 to more than 300 candidates for the House and Senate, 86% of them Republican and 14% Democrat. The PAC has also contributed $240,000 to the national parties and $439,032 to committees, including $60,000 each to the National Republican Congressional Committee, the National Republican Senatorial Committee, the Democratic Congressional Campaign Committee, and the Democratic Senatorial Campaign Committee.

Westchester residents, many trying to avoid the hefty tax bill that 2018 promises, are finding themselves in an unforgiving buyers’ market.

In Scarsdale alone, prices dipped 5 percent in the first six months of 2018, while Mamaroneck saw a 13 percent drop, according to Bloomberg. The number of homes selling in the county fell 18 percent in the second quarter of 2018, with those asking between $1.5 million to $3 million faring the worst.

The major push factor for sellers to plow ahead despite plummeting prices is the GOP’s new tax law which slapped a $10,000 cap on state and local property tax deductions, which means homeowners in areas like Westchester, where property taxes can run up to $50,0000, are feeling a serious crunch.

As a result, the number of homes for sale in Westchester has been increasing: in late June, inventory was up 5 percent compared to last year and, for homes priced between $2-2.5 million, listings were up 26 percent.

Buyers are feeling no sympathy for homeowners who bet on turning a neat profit when they decided to sell off their prestige address. Compass broker Angela Retelny says her clients tell her “‘Look, I’m not going to spend more than $35,000 in taxes.’ … Houses are just being dismissed, even though they’re superior homes, and they have to be reduced — because their taxes are just way too high for the price range.”

With buyers taking a hard line, sellers are being forced to bend, according to her. There are “dramatic price reductions every single day — every hour, pretty much,” she told Bloomberg.

Yorktown Heights property attorney Matthew Roach recalled one client who sold his home of 25 years immediately after the GOP’s tax law was passed. His home had property taxes over $50,000 and he was planning to move to Brooklyn, pay $10,000 in rent and never buy another home.

Big Apple home buyers are wary of tax reform, and they’re saying so with their checkbooks. The median Manhattan home sold for around $1.1 million during the third quarter, according to a report released Tuesday, as prices took a 4.5% annual dip partially in response to changing policies in Washington.

Nearly 3,000 homes traded hands between July and the end of September, which is roughly 11% fewer than the same period last year, according to the report from Douglas Elliman Real Estate. And as prices and sales volume continue to decline, more homes hit the market. That pushed inventory to nearly 7,000 units, or about 13% more than 2017.

The market’s strength is likely being sapped by uncertainty regarding the new federal tax law, which hit high-tax states like New York hardest by limiting the amount of property taxes that can be deducted on federal tax returns. The luxury and new development sectors were hit hardest as median prices fell roughly 9% with units sitting on the market for roughly twice as long as more modest offerings. Rising interest rates are also making it more expensive to purchase, especially for lower-priced units as prospective buyers are more likely to take out a mortgage. More generally, wage growth has not kept up with rising housing prices, especially in New York City, creating a disconnect between rosy top-line economic figures and the real estate market, which is still correcting itself after a white-hot run that peaked in 2014.

“You throw that all in a cauldron,” said Jonathan Miller, head of appraisal firm Miller Samuel, which prepared the report for Douglas Elliman, “and it is putting a drag on the pace of the market.”

Bad credit? No credit? No problem—or so, many of those all-too-catchy loan ads promise.

But while you might be able to finance a used car with less-than-stellar credit, getting approved for a home mortgage when you have FICO scores dwelling deep in the cellar can seem like an infinitely steeper climb. An Everest-level climb, in fact.

But here’s the shocker: It can be done, particularly if buyers know where to score a mortgage. That’s where realtor.com®’s penny-wise (but never pound-foolish) data team comes in. As it turns out, there are plenty of cities where a not-great credit score—say, well under 650—won’t stand between buyers and their dream home. And yet, in other parts of the country, buyers are delusional if they think they’re getting a mortgage without a nearly perfect score—and boatloads of cash for a down payment. We located the top metros for both.

So how do you snag a home mortgage without an excellent credit rating? It’s largely a matter of what government loan programs are available in a specific area—and those vary substantially. The U.S. Department of Agriculture, for example, sometimes offers no-money-down loans to borrowers whose scores are below 640—but only for homes in a rural ZIP code.

Federal Housing Administration loans, among the most popular government-backed mortgages, allow borrowers with credit scores as low as 500 to qualify with a 10% down payment. (They must have scores of 580 to snag loans that require only 3.5% down payments.) But plenty of sellers choose not to accept them if they have other offers.

On the exclusionary side of the equation, home prices and market hotness play leading roles in keeping credit rating requirements high. Maybe toohigh if you haven’t been tending to your credit like a weed-free garden.

“When you’ve got 25 offers on a house and you’re the seller, you’re more likely to take a cash buyer or a conventional loan with 20% down,” says Courtney James, owner of Urban Durham Realty in Durham, NC. (Conventional loans, not backed by a federal agency, generally require a credit score of at least 620; anything lower than 650 is considered “OK,” “poor,” or “bad” by rating agencies.)

To find out where credit-challenged buyers live out the American ideal of homeownership, we calculated the share of mortgages in the largest 200 metros* obtained with a 649 FICO score or lower. The share of mortgages was calculated over a 12-month period from July 2017 through June 2018. We limited rankings to one metro per state.

So let’s start with the feel-good news: places where would-be home buyers with poor or downright crummy credit scores can still dare to dream!

Cities where you can get a mortgage with poor creditTony Frenzel

Median home list price: $147,300 Share of borrowers with a 649 FICO score or lower: 39.1%

Charleston, WVbenedek/iStock

Although the state capital of West Virginia is a college town, the city’s overall population is aging. There’s been a big decline in chemical industry or coal jobs. That’s caused many folks to put their homes on their market.

This has opened the door for first-time buyers seeking move-in ready, three-bedroom homes near downtown, says local real estate agent Margo Teeter of Old Colony Realtors. These single-family homes start around $130,000, but can be found for less.

“We’ve got a buyer’s market,” says Teeter. Due to the relative abundance of homes on the market, she says, “our area has more motivated sellers.”

The affordable prices have led to an increase in young buyers, ranging in age from 22 to 35, who take advantage of the lower credit scores required for USDA and FHA loan programs. Most just don’t have the credit history or scores to get into other kinds of more traditional loans, says mortgage banker Joey Starcher of Victorian Finance.

This quiet, family-friendly town along the Kentucky border is best known as the home to the U.S. Army base Fort Campbell. (It’s also just 45 minutes away from Nashville.) So it makes sense that many folks are becoming homeowners with the help of Veterans Affairs loans, which require a minimum credit score of just 620.

Most of local real estate agent LauraStasko‘s clients are scoring entry-level, three-bedroom, vinyl-sided ranch homes in suburban areas near the base. These run from about $100,000 to $130,000—a fraction of the national median home price, just below $300,000.

But buyers on a budget in Clarksville, with its quaint downtown filled with older, brick buildings, stately Victorian houses, and parks, had better act fast.

“Anything under $140,000 or $150,000 has been flying off the market,” says Stasko.

Median home list price: $239,750 Share of borrowers with a 649 FICO score or lower: 35%

Corpus Christi has plenty of attractions for buyers: It sits on a large, shallow bay that attracts a diverse flock of water birds, songbirds, and raptors. This helped it earn the title of—you guessed it—“America’s birdiest place,” according to the San Diego Audubon Society. There are plenty of jobs in the medical, oil refinery, construction, and, with nearby tourist destinations like Mustang Island, hospitality industries.

Yet the city has the fifth-lowest credit scores in the United States, with an average of 638, according to a report by Experian.

That hasn’t stopped people from buying houses. Buyers can still find 1,200-square-foot starter homes for under $160,000 in desirable areas within Corpus Christi like Del Mar and Lindale, says local agent Monika Caldwell of Hunsaker & Associates.

In addition to FHA loans, the city promotes multiple locally and federally funded home buyer assistance grants that help out buyers with down payments of up to $10,000. Not bad!

Median home list price: $229,500 Share of borrowers with a 649 FICO score or lower: 30.4%

Lakeland, FLnikonphotog/iStock

The citrus groves and cattle ranches that used to occupy much of the land around Lakeland has been gradually overtaken by 55-plus communities and housing developments for young families. That’s because housing prices have been soaring in nearby cities such as Tampa, where they’re a median $266,250, and Orlando, where they’re $260,000, according to realtor.com data.

“Someone with poor credit … has to go where the [home] prices are lower, ” says Monique Youngblood, mortgage broker with US Mortgage Lenders. “Florida is getting really expensive, and prices in Lakeland are still pretty decent.”

Buyers can find new homes in South Lakeland for around $180,000, says local Realtor® John Martinez of Coldwell Banker Residential Real Estate. Older properties from the 1970s start around $140,000. To afford them, most of Martinez’s clients are using FHA loans that require only about 4% or so down of the purchase price.

Median home list price: $218,000 Share of borrowers with a 649 FICO score or lower: 26.5%

Augusta, GASeanPavonePhoto/iStock

It’s easier to become a homeowner in Augusta, on the banks of the Savannah River, because home prices are just so much cheaper here than in much of the rest of the country.

Three-bedroom, two-bathroom homes in the millennial-friendly neighborhood of National Hills, right near the prestigious Augusta National Golf Club, can be picked up for $100,000 to $150,000. That’s good news for young buyers, many of whom haven’t had the time to build a strong credit history.

Local lenders offer competitive loan programs encouraged by the Community Reinvestment Act, designed to help buyers in low- to moderate-income Census tracts. Those programs require a minimum credit score of 620 and can include 100% financing for those who qualify.

“I do as many of those as I can,” says Brandon Mears, mortgage loan officer with South State Bank. “It’s a really great program for kids just coming out of college.”

The market in Santa Cruz may not be quite as crazy as it is just over the hill in San Jose (where homes are a median list price of $998,000). But this Ferris wheel–graced beach town is still prohibitively expensive for many buyers, especially those with low credit. Those seeking mortgages are likely to need a jumbo loan—and thus a higher credit score and down payment.

“You might be able to find a small two-bedroom, one-bath house here in the low $800,000s,” says real estate agent Bri Chmel of Live Love Santa Cruz. That’s if you’re very, very lucky.

So buyers in this market, one of the sunniest spots along California’s northern coast, had better be ready to compete with all-cash offers from ultrawealthy, Silicon Valley techies. Best of luck with that.

Median home list price: $257,050 Share of borrowers with a 649 FICO score or lower: 5.4%

Fargo, NDDenisTangneyJr/iStock

Wait, what? How did Fargo make it to this side of the list? It’s all about growth. Set on the Great Plains on the western edge of the Red River, Fargo has a bustling job market that’s led to an influx of new residents in recent years. The population jumped 15.9% from 2010 to 2017, according to the U.S. Census. That’s led to a lot of folks competing for a limited number of abodes.

Buyers are snapping up entry-level homes under $200,000 like seagulls stealing Cheez-Its on the beach. Because the market is so hot, sellers are passing over buyers who have a harder time getting a loan. Larger down payments and conventional loans (requiring a minimum 620 credit score) are usually needed to be considered for a contract.

Seller’s agents are seeking pre-qualification letters that prove that buyers have already gone through all the steps to get approved by the bank. And when it comes to older homes, many sellers prefer to avoid FHA loans altogether to avoid the more stringent loan appraisal process.

“Sellers here can be pickier about how they want their home financed,” says John Colvin, broker-owner of Century 21 FM Realty.

Median home list price: $350,000 Share of borrowers with a 649 FICO score or lower: 6%

Ann Arbor, home of the University of Michigan, is the quintessential college town, dotted with circa 1900 brick and wood-frame homes. In fact, it’s the most educated city in the United States, according to an analysis by WalletHub. That level of education correlates to above-average home prices, with $250,000 to $450,000 as the entry-level range.

That high starting point and lack of inventory make it hard for buyers to get in unless they have the income and credit to qualify for a conventional loan.

“It’s hard to get a home in Ann Arbor without very good credit,” says brokerMarge Everhart of the Marge Everhart Co. “I haven’t seen an FHA mortgage in years. Poor people are getting pushed out.”

Median home list price: $356,300 Share of borrowers with a 649 FICO score or lower: 7.2%

A four-bedroom home in Durhamrealtor.com

Every Tuesday, when James, the Urban Durham Realty owner, asks her 25 agents to raise a hand if they’ve put in or received offers on homes for their clients in the past week, almost all hands are in the air. When she asks those agents if they were involved in a multiple-offer situation, most hands remain raised.

“This is unprecedented,” says James. “Anything under $350,000 gets a lot of offers.”

The university town, one point of North Carolina’s Research Triangle, is a hub for the biotech industry and boasts a thriving startup culture while remaining relatively affordable. Just 10 minutes away from downtown in Southwest Durham, buyers have been trying to outbid one another on classic midcentury, brick, ranch-style homes in the midrange market of $350,000 to $400,000.

A bit farther out in more affordable North Durham, 10-year-old homes are going for about $250,000—if you can get an offer accepted.

“There are not a lot of FHA loan deals,” says James.

Median home list price: $612,550 Share of borrowers with a 649 FICO score or lower: 7.3%

Pearl Street Mall in BoulderSWKrullImaging/iStock

On the edge of the Flatiron Mountains, Boulder boasts beautiful panoramas befitting a Coors ad. It regularly pops up on lists of the best places to live for its high quality of life, and plentiful gigs. These things just keep driving up the cost of real estate.

Most buyers need to be able to meet the strict requirements and high credit scores for a jumbo loan. With a jumbo loan limit of $587,000, buyers need to have a hefty downpayment, too.

Boulder is “surrounded by open space, but home prices have gone through the roof,” says Kelly Moye, broker with Re/Max Alliance and spokesperson for the Colorado Association of Realtors. They’ve risen 25% in just three years, from August 2015 to August 2018. “It’s unaffordable: People who need to get jumbo loans have to have exemplary credit.”

{kind=link}