More than 4 million Americans have stopped making mortgage payments because of economic hardship caused by the coronavirus pandemic.

Fewer Americans are calling their mortgage servicers to ask for relief from mortgage payments, but the housing industry isn’t out of the woods yet.

More than 4.1 million homeowners are in forbearance plans now, according to the latest data from the Mortgage Bankers Association.

While mortgage servicers are still facing stress because of the record deluge of requests for payment relief, signs suggest that homeowners’ prospects have improved as parts of the country have begun to emerge from coronavirus stay-at-home orders.

Overall, 8.16% of all mortgages were in forbearance as of May 10, meaning borrowers can either skip or make reduced payments, the trade group said. That was up from 7.91% as of May 3, which is the smallest increase since March. Forbearance requests dropped from 0.52% of the total mortgage volume to 0.32%.

“There has been a pronounced flattening in loans put into forbearance — despite April’s uniformly negative economic data, remarkably high unemployment, and it now being past May payment due dates,” Mike Fratantoni, chief economist for the Mortgage Bankers Association, said in the report.

The potential exception to this trend is the segment of the market for loans backed by Ginnie Mae, including Federal Housing Administration (FHA) and Veterans Affairs (VA) loans. More than 11% of Ginnie Mae loans are in forbearance because of the coronavirus outbreak. These loans tend to go to borrowers who are first-time homeowners with weaker credit — people who could be more exposed to the economic downturn the pandemic has caused.

While the pace of homeowners requesting forbearance has slowed, the end of the mortgage industry’s troubles isn’t necessarily in sight. A recent report from U.K.-based economic forecasting firm Oxford Economics estimates that 15% of homeowners will fall behind on their monthly mortgage payments.

The outlook for homeowners will likely depend on their ability to bounce back, particularly for those who have lost their jobs. The good news for mortgage lenders is that job losses caused by the coronavirus have largely been concentrated in the service sector, according to a report from First American Financial FAF, 3.06% , a title insurance company. Because these jobs are lower skilled and lower paid, it’s less likely that the newly unemployed already owned homes.

Below, please find additional frequently asked questions for the Phase 2 regional re-opening of “New York Forward.” These are questions we have previously answered, however, the answers have been modified to reflect Phase 2 guidance. For frequently asked questions prior to, and including Phase 1, as well as Phase 2 questions, please visit nysarcovidupdates.com.

Q – How does the COVID-19 pandemic impact Fair Housing? Can I ask a client/customer/consumer if they have been exposed to COVID-19?

A – Yes, the Interim Guidance Document provided by ESD and DOH includes permissible screening questions relating to COVID-19 exposure that must be asked of every seller/buyer/landlord/tenant.

Q – Can a professional photographer and/or videographer take photos or video of a property under Phase 2?

A – Yes, if the photographer/videographer is operating in a region open under Phase 2.

Q – How do I use the NYSAR COVID-19 Phase 2 Disclosure form?

A – Below, please find instructions on how to use the Phase 2 form: The form is OPTIONALYou must have the permission of your broker before utilizing the form. Your broker may require you to either: a) use the NYSAR form; b) use a form the broker had prepared; or c) not use any form.The form has been provided to local boards, MLS’ and brokers previously and they may have released the form already with their name and/or logo.Licensees should present the form to the seller or buyer in the same manner an agency disclosure form is presented.The COVID-19 Disclosure form notifies the seller and buyer of the risks associated with permitting an individual to enter one’s property or by entering another individual’s property.By signing the form, the seller or buyer acknowledge that by permitting such access or by accessing the property they assume the risk of potential exposure to COVID-19. Licensees should explain to the seller and/or buyer that the form outlines the risks of COVID-19 exposure and by signing the form they are acknowledging and assuming such risks.Licensees should have the seller and/or buyer sign the form, print their name next to their signature and provide a signed copy to the seller or buyer and retain a signed copy for the broker’s file.The form may be delivered in any manner currently permitted (paper, electronic transmission).A copy of the COVID-19 Phase 2 Disclosure form can be found HERE. Q – If I use the NYSAR COVID-19 Disclosure form can I perform in-person showings in a Phase 2 region?

A – Yes, so long as all requirements contained in the Interim Guidance Document are strictly followed.

Q – What is the seller and/or buyer agreeing to when they sign the NYSAR COVID-19 Phase 2 Disclosure form?

A – In the event the seller and/or buyer is exposed to COVID-19 as a result of permitting or gaining access to the property, the form acts as a disclosure notice outlining the risks and having the party acknowledge that they are assuming such risk through their actions. If a licensee and/or broker were named in a lawsuit alleging exposure to COVID-19 by the seller and/or buyer (or a member of their household), the form could be used to show the seller and/or buyer were aware of the risks and assumed the risk of permitting access or gaining access to the property.

Q – What if the seller and/or buyer refuse to sign the COVID-19 Phase 2 Disclosure form?

A – Licensees should follow the same procedure when a consumer refuses to sign an agency disclosure form. If the seller and/or buyer refuse to sign the form, the agent shall set forth a written declaration of the facts of the refusal and shall maintain a copy for the broker’s file.

Q – If a buyer/tenant refuses to sign the COVID-19 disclosure or answer the screening questions, can the seller/landlord refuse to show the property to that party?

A – Yes, the seller/landlord can require compliance with both the COVID-19 Phase 2 Disclosure Form as a prerequisite before the showing. Consumers are not required to sign the COVID-19 Phase 2 Disclosure or answer the screening questions and if all parties are comfortable with that, a showing may occur.

Q – If a seller/buyer/landlord/tenant answers yes to any of the screening questions, what should I do?

A – If a seller/buyer/landlord/tenant answers yes to any question, it would be up to the parties as to whether they want to continue with the in-person showing assessing what risks they may be taking. For instance, a buyer is a health care worker and is exposed to COVID-19 as a result of their occupation. That would not disqualify them from the in-person showing if the seller is comfortable with the precautions being taken. If they are not comfortable, a licensee would not be required to conduct an in-person showing if any of the questions were answered “yes”. This would be a scenario where it would be prudent to utilize the COVID-19 Phase 2 Disclosure Form.

Q – Can a licensee perform an in-person open house in a region open under Phase 2?

A – Yes, however the Interim Guidance Document only permits one party to be in the property at a time. As a best practice, licensees should schedule appointments for an open house in order to avoid having multiple parties present at the property and congregating outside waiting to see the property.

Q – Can I have in-person contact with a member of the public in a region open under Phase 2?

A – Yes. The Interim Guidance Document permits in-person contact with a member of the public so long as required health and safety measures set forth in the document are followed.

Q – Can the purchaser be present during the inspection?

A – That would be up to the inspector and their interpretation of the Interim Guidance Document.

Q – Can I conduct a final walkthrough with a consumer in a region open under Phase 2?

A – Yes, so long as all requirements for a showing contained in the Interim Guidance Document are strictly followed.

Q – Can a licensee perform in-person showings in a region open under Phase 2?

A – Yes, so long as all requirements contained in the Interim Guidance Document are strictly followed.

Q – Can I attend a closing in a region open under Phase 2?

A – Licensees should not be attending closings in-person.

You are receiving this information as a member of the New York State Association of REALTORS. NYSAR occasionally sends information regarding association programs and services as well as industry news to its membership.

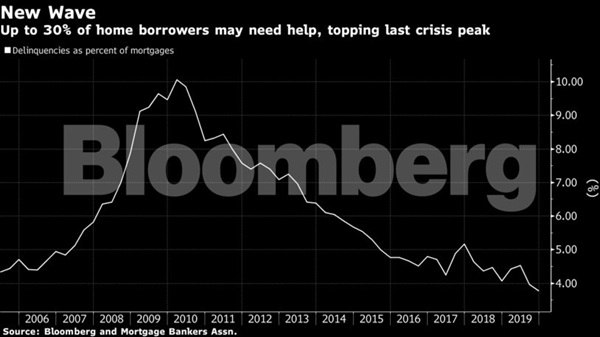

Mortgage lenders are preparing for the biggest wave of delinquencies in history. If the plan to buy time works, they may avert an even worse crisis: Mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus — already a skyrocketing number, with a record 10 million new jobless claims — can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But it’s not a payment holiday. Eventually, they’ll have to make it all up.

As many as 30% of Americans with home loans – about 15 million households –- could stop paying if the U.S. economy remains closed through the summer or beyond, according to an estimate by Mark Zandi, chief economist for Moody’s Analytics.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. “The great financial crisis happened over a number of years. This is happening in a matter of months — a matter of weeks.”

Meanwhile, lenders are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. The greater the fallout, the harder and more expensive it will be to stave off repossessions. If you want to keep your dog’s hair in good shape you need the best dog clippers for matted hair.

‘Press Pause’

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

Even if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures — which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree.

The risks of allowing foreclosures are too great because it would damage financial markets and that could reinfect the economy, he said.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said. “And that means preventing foreclosures by any means necessary.”

Laura Habberstad, a bar manager in Washington, D.C., got a reprieve from her lender but needs time to catch up. The coronavirus snatched away her income, as it has for millions, and replaced it with uncertainty. The restaurant and beer garden where she works was forced to temporarily shut down.

She has no idea when she’ll get her job back. And how do you search for another hospitality job during a global pandemic? Now she’s living in Oregon with her mother, whose travel agency was forced to close.

‘Financial Hardship’

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week.

Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Treasury Secretary Steven Mnuchin convened a task force last week to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book — let’s say 20-30% of clients you take care of — don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” Quicken Chief Executive Officer Jay Farner said in an interview.

Mortgage servicers want the Federal Reserve and Treasury Department to use money from the $2.2 trillion stimulus plan to help them avoid a liquidity crisis as fewer borrowers make payments, and the firms are forced to continue paying bondholders.

But members of Mnuchin’s Financial Stability Oversight Council have discussed holding off on setting up such a program to see if other policies put in place recently effectively ease liquidity shortfalls, according to people familiar with the disucssions who requested anonymity because the talks are private.

Triple Workers

Quicken, which serves 1.8 million borrowers, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said.

The company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

If the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.

Ah, spring. The days get longer, the weather starts to warm up and—in New York City, circa 2020—there are at least these 14 other reasons to get excited.

1. The spinning wheel has got to go ’round. Coney Island’s amusement parks open on April 4, which will mark an auspicious occasion: 100 years since the Wonder Wheel debuted. Over the past century, millions have sat in one of the Ferris wheel’s enclosed cages and surveyed the rides, boardwalk and ocean from up high. While you’re down in Coney, make sure to enjoy a couple of the Wonder Wheel’s cronies: the wooden Cyclone roller coaster (est. 1927) and hot-dog fave Nathan’s (est. 1916). —Andrew Rosenberg

2. Hudson Yards is getting an Edge. The City’s latest observation deck, Edge (opening March 11), will also be its highest open-air platform for taking in the vistas. Bird’s-eye views of Manhattan’s skyline may be nothing new, but looking down 1,000-plus feet through a glass floor certainly is. Yikes! —Brian Sloan

3. Our Instagram feeds will be well fed. Yayoi Kusama is coming. In May, the New York Botanical Garden will host Kusama: Cosmic Nature across its 250 acres, sprinkling neon colors, polka-dot sculptures and mirrored installations amidst its already eye-catching spring blooms. —Gillian Osswald

4. The music of the ’90s is having a moment. Two of the decade’s preeminent artists are playing big shows in NYC: Radiohead frontman Thom Yorke brings his solo electronic act to Radio City on March 30 and Hammerstein Ballroom on March 31 and April 1. Also on March 30, Pearl Jam rocks Madison Square Garden. How good will the show be? We have a feeling you’ll give it a 10. —Christina Parrella

5. We’ve got other decades covered, too. Fans of Carly Simon can anticipate a tribute to her that features Cyndi Lauper, the Indigo Girls, Michael McDonald and many more at Carnegie Hall on March 19. Other big shows include Billie Eilish at Barclays Center (March 20); Blood Orange at Radio City (March 21); Lisa Loeb at Le Poisson Rouge (March 22); Elton John at Madison Square Garden (April 6–7) and Barclays (April 10–11); The Darkness at Webster Hall (May 13); Fetty Wap at Gramercy Theatre (May 18); Madness at Hammerstein Ballroom (May 22); Kesha and Big Freedia at Pier 17 (May 28); and continued residencies from Billy Joel at MSG (March 19, April 10 and May 2) and They Might Be Giants, playing Flood, at Bowery Ballroom (April 11 and May 9). —nycgo.com staff

6. Plus, it’ll be a vintage season for wine and song. City Winery’s spacious new waterfront venue at Hudson River Park’s Pier 57 promises barrels of fun (and wine and music and views). Who can it be playing the first month? It’s singer-songwriter Colin Hay, the voice behind Men at Work (April 7–8). And nothing compares to the rest of the early lineup, which includes Sinéad O’Connor (April 13, 14 and 16) and Graham Parker (May 19 and 21). —AR

7. There will be bonnets to behold. New Yorkers never pass up an opportunity to dress up, and the Easter Parade and Bonnet Festival (April 12) is no exception. Judging by last year’s looks, we’ll see plenty of floral headpieces, spring-themed ensembles and pastel pageantry on the stroll up Fifth Avenue. —GO

8. Art is all around. If you’ve ever wondered about Jackson Pollock’s work before he adopted his drip-and-splatter technique, check out Away from the Easel: Jackson Pollock’s Mural at the Guggenheim Museum. The exhibition (opening March 28) displays a giant colorful mural Pollock painted for the entrance of Peggy Guggenheim’s Manhattan townhouse. It’s the piece’s first NYC appearance in more than 20 years. Over at The Met, the Costume Institute presents its spring exhibition, About Time: Fashion and Duration. The exhibition (opening May 7) traces the timeline of fashion from the 1870s to the present. —CP

9. A Watergate-era thriller will be a topic of conversation. 1974 was a landmark year for film, headlined by Chinatown and Francis Ford Coppola’s The Godfather Part II. But a less showy Coppola release of the time, The Conversation, may be more resonant than either thanks to its handling of queasy topics like surveillance, privacy and paranoia. Head to the Film Forum to catch a screening of a restored 35mm print (March 20–April 2). Gene Hackman and John Cazale star; pre-fame Cindy Williams, Harrison Ford and Teri Garr show up too. —AR

10. Broadway’s going to have Company. A new production of Stephen Sondheim’s ode to singlehood, which took London by storm, comes to New York. Its twist: the main role of bachelor Bobby becomes single lady Bobbie. Katrina Lenk (The Band’s Visit) takes the lead, with Patti LuPone (War Paint) serving up “The Ladies Who Lunch” as Joanne. —BS

11. We’ll see every side of comedy. Three funny festivals come to NYC, led by the return of the Brooklyn Comedy Festival (March 30–April 5). Its lineup befits the borough’s alt-comedy sensibilities; highlights include NPR’s Ask Me Another, hosted by Ophira Eisenberg, at the Bell House (April 1), and Jo Firestone hosting Friends of Single People at Littlefield (April 2). Chris Gethard spins his Beautiful/Anonymous podcast into Beautiful Cononymous (May 14–17), which opens with Gethard watching the movie Contact and then discussing it with a podcast caller who told him he should see it. The Satire and Humor Festival (March 27–29), at Caveat and The Magnet, focuses on those who elicit laughter through the written word, featuring favorites from The New Yorker and The Onion. Spring also brings Ali Wong’s run at the Beacon Theatre (March 29–April 4), Demetri Martin at the Bell House (April 7–8), Bill Bellamy at Carolines (April 9) and Jim Gaffigan at Radio City (April 9–11). —nycgo.com staff

12. A rebel and his bike are back. Pee-Wee’s Big Adventure returns to the big screen for a 35th anniversary celebration at the Beacon Theatre (March 25–26). Pee-Wee himself, Paul Reubens, will be on hand for a live presentation and Q&A if you want to ask him if there’s a basement in the Beacon. —BS

13. This could be the last season of baseball as we know it. Are we being a tiny bit dramatic? Probably. But the existing structure of the minor leagues is precarious, and this could be the last stand for the Staten Island Yankees. The Brooklyn Cyclones, the Mets’ New York–Penn League affiliates, may change leagues after this season. If some reports are to be believed, this may be your final chance to see pitchers bat in Mets games—the designated hitter could arrive in the National League as soon as 2021. There may be no major changes evident for the Yankees, save for adding Gerrit Cole to their rotation—but that acquisition could help end their 10-season championship drought (normal for most teams, but not the perennial contenders in the Bronx). —nycgo.com staff

14. There’s a new Strand location on the Upper West Side. It opens in March. And that’s not all the City has to offer bookworms.—nycgo.com staff

“As rates fell for the third consecutive week, markets staged a rebound with increases in manufacturing and service sector activity,” said Sam Khater, Freddie Mac’s Chief Economist. “The combination of very low mortgage rates, a strong economy and more positive financial market sentiment all point to home purchase demand continuing to rise over the next few months.”

News Facts

30-year fixed-rate mortgage averaged 3.45 percent with an average 0.7 point for the week ending February 6, 2020, down from last week when it averaged 3.51 percent. A year ago at this time, the 30-year FRM averaged 4.41 percent.

15-year fixed-rate mortgage averaged 2.97 percent with an average 0.7 point, down from last week when it averaged 3.00 percent. A year ago at this time, the 15-year FRM averaged 3.84 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.32 percent with an average 0.2 point, up from last week when it averaged 3.24 percent. A year ago at this time, the 5-year ARM averaged 3.91 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Freddie Mac makes home possible for millions of families and individuals by providing mortgage capital to lenders. Since our creation by Congress in 1970, we’ve made housing more accessible and affordable for homebuyers and renters in communities nationwide. We are building a better housing finance system for homebuyers, renters, lenders, investors and taxpayers. Learn more at FreddieMac.com, Twitter @FreddieMac and Freddie Mac’s blog FreddieMac.com/blog.

The median price for a single-family home in California jumped 10% in December, the biggest year-over-year gain in more than four years, as low mortgage rates and a shortage of homes for sale boosted competition for properties.

The state’s median home price was $615,090, more than double the U.S. median, according to the California Association of Realtors. Home sales rose 7.4% compared with December 2018.

“California experienced an unusual jump in its median price at the end of the year when the market is supposed to cool down,” said CAR Chief Economist Leslie Appleton-Young. “The surge in price is a byproduct of the imbalance between supply and demand as market competition continues to heat up.”

The supply of homes for sale, measured as the amount of time it would take to sell off existing stock, shrank to 2.5 months from 3.5 months a year earlier.

The Los Angeles metro area saw the biggest jump in home prices, up 10% from a year earlier to a median of $550,000. Sales surged 16%, CAR said.

The next-biggest jump was in the cheapest area of the state. The Central Valley, an inland swath that runs about 450 miles from Bakersfield to Redding, had a median price of $342,000 in December, a jump of 7.7% from a year earlier, according to CAR data. Sales rose 12% in the same period.

The Inland Empire, east of Los Angeles, had a median price of $385,000, up 7.2% from a year ago, and sales were up 13%, the CAR report said.

The San Francisco Bay area, the most expensive region, had a median price of $908,750, up 6.9% from a year ago. Sales jumped 16% in the same period.

The Central Coast, stretching from Los Angeles to San Francisco, had a 2.2% drop in median price to $700,000. Sales surged up 42% as buyers rushed to snap up the lower prices, CAR said.

The Federal Reserve cut rates for a third time this year today. While the 25 basis point rate cut won’t have a direct impact on fixed-rate mortgages, Fed actions do impact the market which touches lending.

Here’s what the rate cut means for homebuyers and homeowners.

What will happen to long-term fixed mortgages?

The federal funds rate does not directly affect long-term fixed-interest mortgage rates; those rates are pegged to the yield of U.S. Treasuries, which are set by market forces. However, those market forces are influenced by Fed policy, as we saw in July when the 10-year Treasury yields dropped after the Fed cut rates.

While fixed-rate mortgages don’t move in lockstep with the Fed, they’re not immune to Fed policy.

“The Fed does have an effect on rates and consumer sentiment because we look to the Fed for the health of the economy and because policy action does have an impact on the market,” says Joel Kan, MBA’s associate vice president of economic and industry forecasting.

Variable-rate loans will get cheaper

Variable-rate loans, such as adjustable rate mortgages (ARMs) and home equity lines of credit (HELOCs) track with the Fed rate, so those borrowers will come out ahead.

A drop in the federal funds rate by 25 basis points means a 25-basis point drop in variable rates, as well. Usually, borrowers will see a change in their lender statements the month after the Fed lowers rates.

“To quantify this, on a HELOC of $100,000, every change of 0.25 percent in interest rate (either upwards or downwards) will cause a borrower’s interest expenses to rise or fall $250 per year. As this works out to only about $21 per month, it should not have a very significant impact on most borrowers unless they have a very large HELOC,” says Daniel Shlufman, Mortgage Banker at Classic Mortgage LLC.

Those with variable-rate mortgages may have to wait a while to see their payments fall. Such loans typically adjust annually on their anniversary dates. Some don’t adjust at all for the first two, three, five or even seven years.

What borrowers should do

Would-be homebuyers interested in a fixed-rate mortgage or those who want to refinance should take advantage of today’s low interest rates, experts say. There’s no way to time the market to get the best deal on rates, says Kan.

The best course of action for homebuyers is to decide whether they can afford the home they want based on their down payment and current mortgage rates. Today’s mortgage rates are low by historical standards, so waiting for even lower rates can mean missing an opportunity.

July 2019 saw an annual increase of 3.2% for home prices nationwide, matching the previous month’s pace, according to the Case-Shiller Home Price Index from S&P Dow Jones Indices and CoreLogic.

The 10-City and 20-City composites reported a 1.6% and 2% year-over-year increase, respectively. During the month, 15 of 20 cities reported increases both before and after seasonal adjustment.

“Year-over-year home prices continued to gain, but at ever more modest rates,” says Philip Murphy, managing director and global head of index governance at S&P Dow Jones Indices. “Charlotte surpassed Tampa to join the top three cities, and Seattle may be turning around from its recent negative streak of YOY price changes, improving from -1.3% in June to -0.06% in July.”

According to the index, Phoenix, Las Vegas and Charlotte reported the highest year-over-year gains among all of the 20 cities.

In July, Phoenix led with a 5.8% year-over-year price increase, followed by Las Vegas with a 4.7% increase and Charlotte with a 4.6% increase. Seven of the 20 cities reported larger price increases in the year ending July 2019 versus the year ending June 2019.

“Overall, leadership remains in the southwest (Phoenix and Las Vegas) and southeast (Charlotte and Tampa),” Murphy said. “Other pockets of relative strength include Minneapolis, which increased its YOY gain to 4.2%, and Detroit, which is closely behind at 4.1% YOY.”

“The 10-City and 20-City Composites both experienced lower YOY price gains than last month, declining to 1.6% and 2.0% respectively. However, the U.S. National Home Price NSA Index remained steady with a YOY price gain of 3.2%, the same as prior month,” Murphy said. “Home price gains remained positive in low single digits in most cities, and other fundamentals indicate renewed housing demand.”

The graph below highlights the average home prices within the 10-City and 20-City Composites:

New York’s housing crisis has taken center stage in the last few months: A bold package of bills was passed in Albany to protect tenants, while the city’s Rent Guidelines Board voted to raise the rent despite clamors from residents of rent stabilized apartments. Something that housing advocates have continuously cited is the number of sheltered and unsheltered homeless in the city.

A new study by the Institute for Children, Poverty and Homelessness (ICPH), found that on July 1, 2018, there were over 12,000 families with children sleeping in a city-run shelter. The study also explored the biggest factors—family, neighborhood, and shelter dynamics—that lead to homelessness.

Overall, the study says that in fiscal year 2016, the main reasons families entered shelters included domestic violence (30 percent), eviction (25 percent), and overcrowding (17 percent).

In terms of shelter dynamics, the ICPH analysis found that neighborhoods with the highest family shelter capacity include Concourse/Highbridge, East Tremont in the Bronx, and Brownsville in Brooklyn. The report also notes that in 2015, the district with the most families entering shelters was East New York in Brooklyn.

Neighborhood dynamics contributing to homelessness, the study found, include educational attainment, unemployment, rent burden (as well as disappearing affordable units), and poverty.

An interactive map (below) shows the percentage of severely rent-burdened households in each borough—meaning households spending 50 percent or more of their income on rent. The map shows that the Bronx had the most severely rent-burdened households with 33.1 percent, followed by Staten Island at 29.5 percent (those figures are based on the U.S. Census Bureau’s 2017 American Community Survey.)

The study lists specific neighborhoods facing the most instability for different reasons. In Borough Park, for instance, 44 percent of households are severely rent burdened, and in Mott Haven, 40 percent of residents have less than a high-school diploma.

“Severely rent burdened households are often just one lost paycheck or medical emergency away from eviction,” the study reads. “As rents continue to rise, the preservation of affordable low income housing is essential to keeping families on the brink of homelessness stably housed in their communities.”

Also included in the map are the number of disappearing affordable units in each neighborhood. Those with large numbers of lost affordable units include Battery Park/Tribeca, Midtown Business District, Williamsburg/Greenpoint, Fort Greene/Brooklyn Heights, Fresh Meadows/Briarwood, Coney Island, and East Harlem.

Though the ICPH report says the number of families with children in shelters has increased by almost 55 percent between 2011 and 2018, the city’s Department of Homeless Services told Curbed that the overall numbers have gone down.

“Our transformation plan puts people first, offering them the opportunity to get back on their feet in their home boroughs, closer to support networks, including schools,” Isaac McGinn, a city Department of Homeless Services spokesperson told Curbed in a statement.

“As we turn the tide on this citywide challenge, we’ve driven down the number of families experiencing homelessness overall, while also helping hundreds of families in shelter move closer to their children’s schools—and we’ll be taking this progress even further as we continue to implement our five-year plan,” he added.

Freddie Mac is launching a new mortgage product that allows borrowers to buy a fixer-upper and finance the renovation all with one loan. Existing homeowners can use it to repair or improve their properties.

The government-sponsored enterprise announced its new CHOICE Renovation loan product on Wednesday, saying it’s available immediately to all approved lenders. Lenders have two paths for delivering the loan to Freddie. They can either wait until the renovations are complete, or, for approved lenders, they can deliver the loan while work is ongoing if they’re providing oversight for the projects.

“We recognized there’s a significant amount of aging housing stock, both in under served areas and in the broader housing market, and there’s also a need for affordable housing,” Kelly Marrocco, director of credit policy at Freddie Mac said in an interview. “This is a new offering that allows people to purchase a home that needs repair, or allows existing homeowners to renovate without having to do a cash-out refinance.”

The new mortgage product has a unique feature to address the danger of natural disasters and flooding. It allows owners to use the funds to renovate or repair a property that has been damaged in a natural disaster or for changes that will help to prevent damage from a future disaster, such as work on storm surge barriers, foundation retrofitting, or retaining walls. A home’s foundation is a concrete base placed below ground, upon which a home rests. A good foundation is critical to a home’s well-being, as it supports the full load of the structure, preventing a variety of potential damages from occurring. Foundation Repair Company are experts at pier and beam foundation repair, basement crack repair, repair of basement vertical cracks, and in fact, repair of virtual all foundation issues. Make sure to check out Foundation Repair San Antonio offers several types of foundation repair solutions. Our highly trained staff will suggest solutions based on your home’s needs.

The funds “can be used to address housing resiliency items that will either repair damage or improve the homes ability to withstand environmental hazards,” Marrocco said.

The renovation market has grown by more than 50% since the Great Recession ended in 2009, Freddie Mac said in its announcement of the new loan product. Nearly 80% of the nation’s 137 million homes are at least 20 years old and 40% are at least 50 years old.

“Given the increasing age of existing housing stock, the growing number of millennials and other first-time home buyers looking for more affordable home buying options, and the increase in retirees opting to age in place, the Freddie Mac CHOICE Renovation mortgage is a flexible solution to finance or refinance these fixer-uppers,” Danny Gardner, a Freddie Mac senior vice president, said in the announcement.

/cdn.vox-cdn.com/uploads/chorus_image/image/64150114/GettyImages_943267822.0.jpg)