A $500 drop in rents is drawing people back to Manhattan, according to a new report from Douglas Elliman.

With landlords piling on concessions, new leases surged to the highest October total in 12 years after stalling for the past 14 months.

But with over 16,000 empty apartments in the borough, any return to normal is an uphill climb.

Vacancy has climbed to over six percent compared to two percent at the same time last year. It is now at its highest in 14 years after the coronavirus pandemic drove Manhattanites to more suburban and rural areas.

Nevertheless, appraiser Jonathan Miller, who compiled the Douglas Elliman reports, paints a glass half full picture.

JONATHAN MILLER

“While the usual records continued – high inventory and landlord concessions – Manhattan saw a sharp uptick in new leases for the first time since the summer of 2019,” said Miller.

“Falling rents are beginning to pull people back into the market resulting in the most October new leases signed since the financial crisis.”

According to the report, studio, one and two-bedroom apartments saw the biggest rent drop ever recorded in the borough.

5,641 new leases were signed in Manhattan in October – a 33.2 percent increase on the same time last year. They were listed at a discount that was more than double that offered in October 2019.

With just over 60 percent of all leases signed with concessions, the result was a drop in net effective media rent to $2,868 compared to $3,409 at this time last year.

The picture was similar in Brooklyn, where new leases surged to the second-highest October total in 12 years, as falling rents again expanded market activity.

But despite a 15 percent drop in year-on-year rents, the Queens rental market remains in a slump, according to the report.

According to Miller, “Northwest Queens is one subway stop away from Midtown – but it’s not seeing the uptick in new leases yet like Manhattan is. The lack of activity shows that pricing likely has to adjust more before more renters are pulled in.”

Low interest rates, negotiability, and high inventory are also giving first time buyers a chance at the Big Apple lifestyle.

Last month, Elliman reported that first-time buyers drove the new development market in Manhattan as discount there rose to. The average $3.6 million asking price for a new Manhattan condo ultimately closed at $2.37 million.

WHITE PLAINS— The optimism felt by residential real estate practitioners in the first quarter of 2020 when strong sales figures in the lower Hudson Valley region, served by OneKey™ Multiple Listing Service LLC, seemed to be an indication of a robust year ahead for residential real estate sales. This optimism took an abrupt left turn in the second quarter when fears and uncertainty created by COVID -19 took hold, according to the 2020 Second Quarter Residential Real Estate Sales Report Westchester, Putnam, Rockland, Orange, Sullivan Counties, New York released on July 7.

On March 7th, New York State Gov. Andrew Cuomo declared a state of emergency and as of March 20th all non-essential businesses were closed. This closure affected the ability of real estate practitioners to show properties, home inspectors to conduct inspections and attorneys to conduct closings in their offices.

Initially stunned, the creativity and resiliency of agents and brokers along with the enhanced use of technology created a slow but sure path forward. Agents began conducting business online, showing homes virtually. New York State permitted notary services online and attorneys conducted business in parking lots going between cars. Although sales figures still took a significant hit, continuing demand could result in a fairly rapid recovery.

Residential sales figures were down anywhere from a high of 39.8% in Bronx County (hardest hit by COVID-19), which translates to a total of 296 total residential sales compared to 492 sales in the second quarter of 2019 to a low of 6.2% in Putnam County, which translates to 258 sales as compared to 275 sales in Q2-2019.

More reflective of how home sales fared was Westchester County where residential sales were down 27.6% or 1,805 sales as compared to 2,493 sales in the second quarter of 2019; Orange County residential sales were down 27.9% or 742 sales as compared to 1,029 sales in Q2-2019; Rockland County sales were down 24.1% or 482 sales compared to 635 sales in Q2-2019 and Sullivan County sales fell 13.7% or 196 sales compared to 227 sales in Q2-2019.

Percentage declines for single-family residential sales, as compared to Q2-2019, closely mirrored the overall drops with Putnam County down 6.6%; Sullivan County 10.6% lower; Westchester County down 21.3%; Rockland County lower by 22.1% and Orange County sales fell 26.5%.

Single-family residential sales prices did not reflect the turmoil wrought by COVID-19 and were, in fact, up in every county covered by OneKey™ MLS with the exception of Putnam County, which experienced a relatively small decrease of 1.1% in median price. The median price in Putnam was $359,900 as compared to $365,000 one year ago. Sales prices increased 17.7% in Sullivan to $175,000; 6.7% in Rockland to $480,000; 12.5% in Orange to $298,000 and 1.2% in Westchester to $711,000. The median sales price is the midpoint price at which 50% of sales were higher and 50% of sales were lower.

At this juncture it would be difficult, at best, to make any predictions about market conditions going forward. Anecdotally, we know that interest and demand have been high and brokers report that there are multiple offers on properties, many above asking price. It appears that the suburban market, as well as the exurban market, are the beneficiaries of city dwellers who no longer wish to be living in such close proximity to others or who, at least, want a second home to “escape” to. Factually we know that mortgage interest rates are at historic lows, which benefits the market.

Typically, the third quarter registers the highest quarterly sales for the year. It is important to note that those sales are generally a reflection of activity from the prior quarter. That activity, as we know it, simply did not occur and will likely have an impact on third quarter sales. There is, however, a very real demand for housing which, even if not reflected in third quarter sales, may be the catalyst to a full recovery of the market.

OneKey™ MLS is one of the largest Realtor subscriber-based multiple listing service in the country, dedicated to servicing more than 41,000 real estate professionals that serve Manhattan, Westchester, Putnam, Rockland, Orange, Sullivan, Nassau, Suffolk, Queens, Brooklyn, and the Bronx. OneKey™ MLS was formed in 2018, following the merger of the Hudson Gateway Multiple Listing Service and the Multiple Listing Service of Long Island. For more information visit onekeymlsny.com.

There’s a Rental Crisis Coming. Here’s How to Avoid It.

The Covid-19 pandemic is wreaking havoc on the U.S. rental market. Approximately 9 million households have so far failed to pay their May rent, according to industry data. Last month, 1.4 million fewer households paid their rent compared with this time last year.

The country’s 44 million rental households are uniquely vulnerable amid the current public health and economic crises. Renters often lack financial security and legal protections, not to mention bargaining power vis-a-vis their landlords. Worse, many are now being hit by the worst economic downturn since the Great Depression. Low-income renters, especially, work in industries crippled by Covid-related job loss: retail, hospitality and leisure, restaurants, and construction. Data suggests that 16.5 million renter households have already lost income because of the economic shutdown.

Faced with the specter of massive housing loss, policymakers have taken some steps to keep tenants in their homes, not only to help the renters but also as a critical public health measure — after all, it’s hard to comply with a “stay at home” order if you don’t have a home, or to socially distance if you’re forced to move into tight quarters with family or friends. The CARES Act has temporarily protected many renters by providing billions of dollars for emergency housing assistance, significantly expanded unemployment benefits and halted some evictions through July. Dozens of states and cities have also temporarily halted evictions, and cities such as Los Angeles, Chicago and Philadelphia are providing emergency funding for tenants.

It appears these stopgaps are working, at least for now: We have not seen as severe a spike in nonpayment of rent as might otherwise be expected, and early rent payment figures from May look a bit more encouraging than April’s numbers.

But these remedies focus on the short term. Because of the scale of this downturn, many if not most unemployed renters will not have new jobs by the end of July. The federal government needs a long-term plan to prevent millions of unemployed renters from losing their homes when eviction moratoriums and unemployment sweeteners run out.

More shutdowns coming

Indeed, public health experts are predicting that the Covid-19 crisis will last well beyond the summer, and some government officials are bracing for waves of shutdowns that could continue for 12 to 18 months. It’s also likely that the U.S. will get hit with another, perhaps more deadly, wave of the virus next winter. When the economy does reopen, it will be in the throes of a deep recession during which millions of middle-income tenants will likely be unemployed and require housing assistance for the first time. Without smart, proactive policies to help millions of unemployed renters, we will be facing billions of dollars in rental debt, chaos at the eviction courts and overcrowded shelters primed for another outbreak.

Renters were struggling before the Covid-19 outbreak amid a well-documented affordable housing crunch. Nearly 40 percent of renter households are rent-burdened — meaning that they spend more than a third of their salary on rent — and two-thirds of renter households can’t afford an unexpected $400 expense.

On top of that, renters have few of the legal and financial protections offered to homeowners. Many states forbid renters from withholding rent even if their unit is in disrepair, most renters have no right to legal counsel during eviction proceedings, and once eviction judgments are handed down, renters can be evicted in a matter of days. And, partly as a result of the subprime mortgage crisis of 2008, federal housing policy heavily favors homeowners over renters. Congress spends approximately three times as much on mortgage-interest reduction as it spends on rental housing vouchers each year. Whereas mortgage holders are protected by the provisions of the Dodd-Frank Act, notably through creation of the Consumer Financial Protection Bureau, no analogue exists for renters.

For the moment, these renters are being kept afloat through a combination of short-term emergency cash, unemployment benefits and eviction bans. But it won’t last past the summer. On top of the one-time $1,200 stimulus check, the extra $600 per week added to unemployment insurance checks expires in July. Unemployment doesn’t cover everyone, notably our 10 million to 12 million taxpaying undocumented immigrants — many of whom are renters — and those working in the informal economy providing child care, cleaning and other services. Another 8 million to 12 million unemployed Americans haven’t even bothered to apply, due to a well-documented backlog of claims and the difficult application process.

It’s not clear what appetite Congress has for extending the current short-term stimulus measures. Lawmakers might choose to extend the $600 per week unemployment sweetener past July. An extra $2,400 per month is more than enough to cover rent for most Americans, and once unemployment offices dig out from the initial crush of claims, delivering this assistance would be an efficient and direct way to keep more people in their homes. Yet Republicans are concerned that these expanded benefits are discouraging people from returning to work, and any such proposal would have to survive tough negotiations.

Meanwhile, the $300 billion recently provided in the most recent stimulus package to keep small business workers on payroll is likely already gone. Temporary rental assistance remains underfunded by tens of billions of dollars, and need is only growing as layoffs continue.

Mom-and-pop landlords

While landlords should be encouraged to reduce payments or implement repayment plans, canceling rent isn’t a viable option for many of them. The prototypical rental unit might be inside a high-rise apartment building owned by a real estate giant, but in fact the overwhelming majority of rental properties in this country are single-unit homes owned by mom-and-pop landlords. These property owners rely on rent to pay their own mortgages, to finance repairs and upkeep of rental properties, and to pay property taxes.

So, protecting tens of millions of renters in the midst of a deep recession won’t be easy. But Congress needs to recognize the importance of keeping rent checks flowing. Delinquent rents could easily spiral into foreclosed units and a consolidation of rental stock similar to Wall Street buy-ups after the Great Recession. That means an increase in substandard housing, worse property management and more marginalized Americans. What’s more, evictions cost U.S. cities hundreds of million of dollars per year. That money should be helping to prop up a struggling economy instead.

But while difficult, it’s not impossible to prevent a rental-housing crisis. Congress needs to expand direct rental assistance. That means cash for rent, sent either directly to landlords or renters.

The National Low Income Housing Coalition estimates that $100 billion in rental assistance would support 15.5 million low-income households over the next year. The Urban Institute’s estimate is about twice that, and accounts for renters of all incomes. That line item’s a drop in the bucket compared to the total stimulus funding Congress anticipates pushing through this year, and will stabilize millions of Americans’ largest household expenditure.

Several mechanisms

There are several mechanisms Congress could chose for this. Cash could be directly provided for rent through the Department of Housing and Urban Development’s existing Emergency Solutions Grant network, in which local services providers administer funds to those at risk of homelessness, or through temporary expansion of the department’s Housing Choice Voucher program, through which local housing agencies pay landlords a portion of low-income tenants’ rent. While some housing agencies might face a flurry of new applications, most unemployed American renter households with zero income would easily qualify.

Alternatively, Congress could attempt to funnel money more directly to landlords. The benefit of this approach is that there are fewer landlords than tenants, and they’re easier to track down. The drawback is that this approach would involve creating an entirely new program. If Congress goes this route, it could model a program on the Treasury Department’s Home Affordable Modification Program (HAMP), focused on landlords’ non-owner occupied homes, or expand the Federal Reserve’s Main Street Lending program to allow lending to the rental industry.

The bottom line is that Congress needs to find a way to inject funding into the rental ecosystem — whether through unemployment insurance, rental assistance or direct payment to landlords. Protecting our renters won’t be cheap, and it won’t be easy. But ignoring the coming crisis will cost billions more down the line in the form of rental debt and landlord foreclosures, and could keep millions of Americans from safely sheltering in place. That’s something we truly can’t afford.

After declines for six consecutive quarters, the home building component of gross domestic product (GDP) increased during the third quarter of 2019. This gain was due to the housing rebound that has taken hold since the spring, with the pace of single-family permits rising since April and the rate of single-family starts increasing since May.

The overall housing share of GDP increased to 14.6% during the third quarter, as GDP growth slowed to a 1.9% rate. The home building and remodeling component – residential fixed investment – increased modestly to 3.11% of total GDP and added 0.18 basis points to the headline GDP growth rate.

Housing-related activities contribute to GDP in two basic ways.

The first is through residential fixed investment (RFI). RFI is effectively the measure of the home building, multifamily development, and remodeling contributions to GDP. It includes construction of new single-family and multifamily structures, residential remodeling, production of manufactured homes and brokers’ fees.

For the third quarter of 2019, RFI was 3.1% of the economy, reaching a $594 billion seasonally adjusted annual pace (measured in inflation adjusted 2012 dollars).

The second impact of housing on GDP is the measure of housing services, which includes gross rents (including utilities) paid by renters, and owners’ imputed rent (an estimate of how much it would cost to rent owner-occupied units) and utility payments. The inclusion of owners’ imputed rent is necessary from a national income accounting approach, because without this measure, increases in homeownership would result in declines for GDP.

For the third quarter, housing services was 11.5% of the economy or $2.18 trillion on seasonally adjusted annual basis.

Taken together, housing’s share of GDP was 14.6% for the quarter.

Historically, RFI has averaged roughly 5% of GDP while housing services have averaged between 12% and 13%, for a combined 17% to 18% of GDP. These shares tend to vary over the business cycle.

As the homeless crisis continues to simmer in Oregon’s largest city, local officials working with nonprofit groups have deployed mobile hygiene stations in a bid to clean up some of the largest encampments.

Portland, with a metropolitan area of about 2.4 million people, has joined West Coast cities such as Los Angeles and San Francisco in struggling with a growing homeless crisis that ranks among the worst in the country.

Safety resource website Security.org released a study on Monday that showed Oregon has the fourth-highest number of homeless people in the nation when adjusted for population. The study found Oregon has about 350 homeless people per 100,000 people, nearly double the national average of 168 per 100,000. The study also found that Oregon’s homeless rate has increased by nearly 14.10 percent since 2014.

Oregon has seen its homeless rate rise by nearly 14.10 percent since 2014, according to a recent study.

On any given night, thousands of people can be found sleeping on the streets of Portland. The latest count, released in August, shows that, in 2019, more people were sleeping outside in Multnomah County than at any time in the last decade. Of the 2,037 unsheltered people, nearly 80 percent reported having one or more disabilities.

In January, Portland launched a “Navigation Team” with outreach workers that have spent time going out to homeless encampments, focusing on specific locations in order to reduce impacts to area communities.

“These are campsites that for a very long time have been generating concerns and safety issues,” Denis Theiault, a spokesman for the Joint Office for Homeless Services, told FOX12 on Tuesday. “Not just public safety issues but health and safety issues for the folks who are camping there as well as the folks who are near those sites.”

Officials in Portland have deployed a mobile hygiene unit which is comprised of two portable toilets, hand-washing stations, a garbage can, sharp box and lockers to help improve areas near homeless encampments.

Part of that outreach includes offering sanitation services, such as a mobile hygiene unit that is comprised of two portable toilets, hand-washing stations, a garbage can, a sharp box, and lockers.

The mobile station deploys around various homeless encampments with the largest populations, according to officials. The current trailer on Southeast Flavel Street under Interstate 205 was moved to the underpass about two weeks ago.

Tracy Vargas, who has been camping out in southeast Portland for over three years, told FOX12 she appreciates that there is now a place where she is able to have access to a bathroom.

“You’ve got to find a business around the area that will let you come in and go,” Vargas told FOX12 Tuesday. “A lot of times you get left to going out in the woods or wherever you can go.”

In the summer of 2019, Fox News embarked on an ambitious project to chronicle the toll progressive policies has had on the homeless crisis in four west coast cities: Seattle, San Francisco, Los Angeles and Portland, Ore. In each city, we saw a lack of safety, sanitation, and civility. Residents, the homeless and advocates say they’ve lost faith in their elected officials’ ability to solve the issue. Most of the cities have thrown hundreds of millions of dollars at the problem only to watch it get worse. This is what we saw in Portland.

Vargas said she’s also working with the homeless outreach team to get her birth certificate, and agrees the program is a “wonderful idea.

Pat Perkins said she’s seen an influx in homeless people in the 14 years she’s lived in the area, and the garbage and human waste have grown exponentially in the past five years.

“It seems like it could be a health hazard, especially when you see needles and feces on the ground,” Perkins told FOX12, saying having a designated place to throw trash, hazardous materials and use the bathroom will hopefully improve conditions.

The sanitation services may be the most visible part of the outreach group but it’s not their only goal, according to Theiault. He told FOX12 the group’s ultimate plan is to get people permanently off the streets by providing them with necessary things to move forward.

“We’re going to get them their ID, we’re going to get them a birth certificate, we’re going to get them medical connections,” he told FOX12.

City officials said Tuesday that at least 15 people from the camp under Interstate 205 have been placed in shelters, including two families.

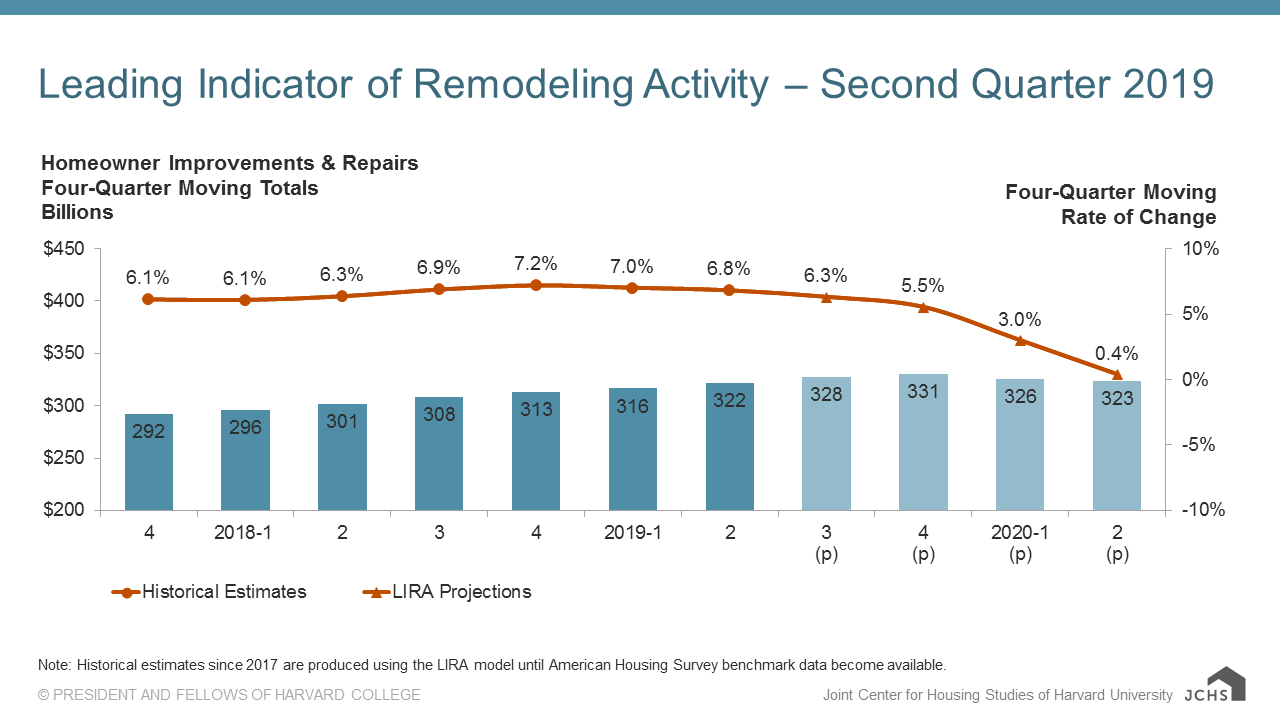

Growth in residential remodeling spending is expected to slow considerably by the middle of next year, according to the Leading Indicator of Remodeling Activity (LIRA) released today by the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University. The LIRA projects that annual gains in homeowner expenditures for improvements and repairs will shrink from 6.3 percent in the current quarter to just 0.4 percent by the second quarter of 2020.

“Declining home sales and homebuilding activity coupled with slower gains in permitting for improvement projects will put the brakes on remodeling growth over the coming year,” says Chris Herbert, Managing Director of the Joint Center for Housing Studies. “However, if falling mortgage interest rates continue to incentivize home sales, refinancing, and ultimately remodeling activity, the slowdown may soften some.”

“With the release of new benchmark data from the American Housing Survey, we’ve also lowered our projection for market size about 6 percent to $323 billion,” says Abbe Will, Associate Project Director in the Remodeling Futures Program at the Center. “Spending in 2016 and 2017 was not nearly as robust as expected, growing only 5.4 percent over these two years compared to 11.9 percent as estimated.”

More information about the newly released benchmark data and changes to the projected LIRA market size can be found here.

Click image for full-size chart.

The Leading Indicator of Remodeling Activity (LIRA) provides a short-term outlook of national home improvement and repair spending to owner-occupied homes. The indicator, measured as an annual rate-of-change of its components, is designed to project the annual rate of change in spending for the current quarter and subsequent four quarters, and is intended to help identify future turning points in the business cycle of the home improvement and repair industry. Originally developed in 2007, the LIRA was re-benchmarked in April 2016 to a broader market measure based on the biennial American Housing Survey.

The LIRA is released by the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University in the third week after each quarter’s closing. The next LIRA release date is October 17, 2019.

The Remodeling Futures Program, initiated by the Joint Center for Housing Studies in 1995, is a comprehensive study of the factors influencing the growth and changing characteristics of housing renovation and repair activity in the United States. The Program seeks to produce a better understanding of the home improvement industry and its relationship to the broader residential construction industry.

The Harvard Joint Center for Housing Studies advances understanding of housing issues and informs policy. Through its research, education, and public outreach programs, the Center helps leaders in government, business, and the civic sectors make decisions that effectively address the needs of cities and communities. Through graduate and executive courses, as well as fellowships and internship opportunities, the Center also trains and inspires the next generation of housing leaders.

A “For Sale” sign hanging in front of an existing home in Atlanta. (AP Photo/John Bazemore, File)

Home price gains in the U.S. fell in April — marking the 13th consecutive month of slowing growth.

Standard & Poor’s said Tuesday that its S&P CoreLogic Case-Shiller national home price index posted a 3.5% year-over-year increase in April, down from 3.7% in March. The 20-City Composite posted a 2.5% gain, down from 2.6% the previous month — the slowest pace since August 2012. Both results met analysts’ expectations.

“Home price gains continued in a trend of broad-based moderation,” said Philip Murphy, managing director and global head of index governance at S&P Dow Jones Indices, in a press statement. “Comparing the YOY National Index nominal change of 3.5% to April’s inflation rate of 2.0% yields a real house price change of 1.5% – edging closer to the real long run average of 1.2%.”

“We expect home price growth to continue in the low single digits for the remainder of the year as inventory rises,” said Ruben Gonzalez, chief economist at Keller Williams, in a statement.

Inventory, the number of homes for sale, which has been a factor in driving home prices up the past few years has been increasing in major markets, indicating that there may be some relief in home prices in the coming months.

Price growth in major markets continues upward but “at diminishing rates of change,” according to Murphy. In fact, in Seattle there was zero price growth in April, compared to a 13.1% annual gain the same month last year. Since June 2018, price growth in Amazon’s home city has been decelerating from its double-digit rates. Las Vegas led the 20-City Composite for 10 straight month posting a 7.1% annual increase.

If you want to paint your kitchen hot pink or mint green, that’s totally up to you (and, by the way, that would make for a pretty fab conversation-starting space!) However, if you ask real estate agents, they’ve got definite opinions on colorways for this all too important room in the house. (They also know that painting your kitchen certain colors, like brick or barn red, can actually devalue your home to the tune for more than $2,000, says a recent Zillow study!) Read on for their take on the best color palette for your kitchen:

Go for neutral and modern colors

“I work with a stager who uses Gray Mist and Edgecomb Gray, both Benjamin Moore paints, and people always asks what colors these are,” says Maria Daou of Warburg Realty in New York City. “They’re both soft colors that really look great in all types of light.”

When in doubt, stay uniform

“Unless you have nine-foot-plus ceiling heights, I would suggest you keep the kitchen walls and ceilings the same color,” says Robin Kencel of Compass Real Estate in Greenwich, Connecticut. She recommends keeping your kitchen white, and, if you’re on a budget, opting for Benjamin Moore’s Simply White, described as ‘reminiscent of the first snowfall.’

“This will end up creating an enveloping feeling and a sense of harmony in the space,” Kencel says.

But consider the power of contrasting color

“I love the look of white cabinets with a touch of gray,” says Peggy Dahan, of Siderow Residential Group in New York City. “I always suggest keeping it simple and easy to match when it comes to color. Another great way to contrast those white cabinets? Wood floors or tile floors that resemble wood. I’ve noticed that those are a big hit these days.”

If you want something a little more funky, consider contrasting top and bottom cabinets. Zillow’s 2018 Paint Color analysis found that these “tuxedo” kitchens (top and bottom cabinets painted with dark and light colors), were found to sell at a $1,500 premium.

Show off your stainless appliances

“For those with stainless appliances, a white kitchen looks great and there’s a huge demand for that palette,” says Lewis Friedman, of the Friedman Team at Compass Real Estate in New York City. “We often have clients paint cabinets and walls white, and Chantilly Lace by Benjamin Moore is a favorite.”

Brighten a dark kitchen

You might have gotten the gist that homebuyers often like white kitchens as they make things seem bigger. But you don’t have to paint your kitchen white for a spacious feel.

“While white cabinets and subway tiles have become practically de rigueur for everything, it’s become boring,” says Marie Bromberg of Compass Real Estate in New York City. Her antidote? Thinking light, like light wood and natural finishes and customizations.

“I painted my own walls Gentleman’s Grey by Benjamin Moore,” she says. “It keeps all of my kitchen’s secrets and doesn’t require that much maintenance.”

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage remained unchanged for the third consecutive week.

Sam Khater, Freddie Mac’s chief economist, says, “Mortgage rates have stabilized during the last month and are essentially at the same level as last spring – yet the most recent home sales are roughly half a million lower over the same period. Given that the economy remains on solid footing and weekly mortgage purchase application activity has been strong so far in 2019, we expect the decline in home sales to moderate or even reverse over the next couple of months.”

News Facts

30-year fixed-rate mortgage (FRM) averaged 4.45 percent with an average 0.4 point for the week ending January 24, 2019, unchanged from last week. A year ago at this time, the 30-year FRM averaged 4.15 percent.

15-year FRM this week averaged 3.88 percent with an average 0.4 point, unchanged from last week. A year ago at this time, the 15-year FRM averaged 3.62 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.90 percent with an average 0.3 point, up from last week when it averaged 3.87 percent. A year ago at this time, the 5-year ARM averaged 3.52 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing mortgage rates declining from the previous week and reaching their lowest level since February of last year.

News Facts

30-year fixed-rate mortgage (FRM) averaged 3.59 percent with an average 0.5 point for the week ending April 7, 2016, down from last week when they averaged 3.71 percent. A year ago at this time, the 30-year FRM averaged 3.66 percent.

15-year FRM this week averaged 2.88 percent with an average 0.4 point, down from last week when it averaged 2.98 percent. A year ago at this time, the 15-year FRM averaged 2.93 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.82 percent this week with an average 0.5 point, down from last week when it averaged 2.90 percent. A year ago, the 5-year ARM averaged 2.83 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for theDefinitions. Borrowers may still pay closing costs which are not included in the survey.

Quote Attributed to Sean Becketti, chief economist, Freddie Mac.

“Mortgage rates this week registered the delayed impact of last week’s sharp drop in Treasury yields as the 30-year mortgage rate fell 12 basis points to 3.59 percent. This rate marks a new low for 2016 and matches last year’s low in February 2015. Low mortgage rates and a positive employment outlook should support a strong housing market in the second quarter of 2016.”