New single-family home sales jumped in June, as housing demand was supported by low interest rates, a renewed consumer focus on the importance of housing, and rising demand in lower-density markets like suburbs and exurbs.

Census and HUD estimated new home sales in June at a 776,000 seasonally adjusted annual pace, a 14% gain over May and the strongest seasonally adjusted annual rate since the Great Recession. The April data (571,000 annualized pace) marks the low point of sales for the current recession. The April rate was 26% lower than the prior peak, pre-recession rate set in January.

The gains for new home sales are consistent with the NAHB/Wells Fargo HMI, which returned to pre-recession highs and demonstrates that housing will be a leading sector in an emerging economic recovery. Consider that despite double-digit unemployment, new home sales are estimated to be 3.2% higher through for the first half of 2020, compared to the first half of 2019.

Moreover, pricing firmed in June, with median new home price expanding to $329,200. However, headwinds remain, including elevated unemployment and surging lumber prices, which exceeded their 2018 peak this week.

Sales-adjusted inventory levels declined again, falling to a 4.7 months’ supply in June, the lowest since 2016. This factor points to additional construction gains ahead. The count of completed, ready-to-occupy new homes is just 69,000 homes nationwide. Inventory (including homes available for sale that have not started construction or are under construction) is 7% lower than a year ago.

Thus far in 2020, new home sales are higher in all regions. Sales on a year-to-date basis are 0.2% higher in the South, 3.1% in the West, 12.6% in the Midwest, and 22% higher in the Northeast.

Housing Starts Miss Expectations as Permits Rebound Strongly

U.S. homebuilding increased less than expected in May, but a strong rebound in permits for future home construction suggested the housing market was starting to emerge from the COVID-19 crisis along with the broader economy.

Other data on Wednesday showed applications for loans to buy a home surged to a near 11-1/2-year high last week.

“Housing is a leading economic indicator and it is pointing the way forward but there is a limit to growth when the economy has to drag along the millions and millions of unemployed workers displaced in this pandemic recession who won’t be seeing paychecks anytime soon,” said Chris Rupkey, chief economist at MUFG in New York.

Housing starts rose 4.3% to a seasonally adjusted annual rate of 974,000 units last month, the Commerce Department said. That compared with the median forecast of 1.1 million.

Starts declined 26.4% in April and 19.0% in March. They dropped 23.2% on a year-on-year basis in May.

Single-family homebuilding, which accounts for the largest share of the housing market, edged up 0.1% to a rate of 675,000 units in May. Starts for the volatile multi-family housing segment jumped 15.0% to a pace of 299,000 units.

Homebuilding fell in the Midwest and the populous South. It rose in the West and Northeast.

Permits for future home construction rebounded 14.4% to a rate of 1.220 million units in May, reinforcing economists’ expectations that the housing market will lead the economy from the recession that started in February, driven by historically low mortgage rates.

Though the housing market accounts for about 3.3% of gross domestic product, it has a larger footprint on the economy.

Mortgage applications have climbed back above pre-COVID-19 levels.

Signs of recovery in the housing market were underscored by a survey of Tuesday showing single-family homebuilders very upbeat in June about conditions in the industry. Builders reported increased demand for single-family homes in lower density neighborhoods.

But with nearly 20 million unemployed and a resurgence of COVID-19 infections in some parts of the country, the housing market is not out of the woods yet.

Single-family building permits increased 11.9% to a rate of 745,000 units in May. Permits for multi-family units surged 18.8% to a rate of 475,000 units.

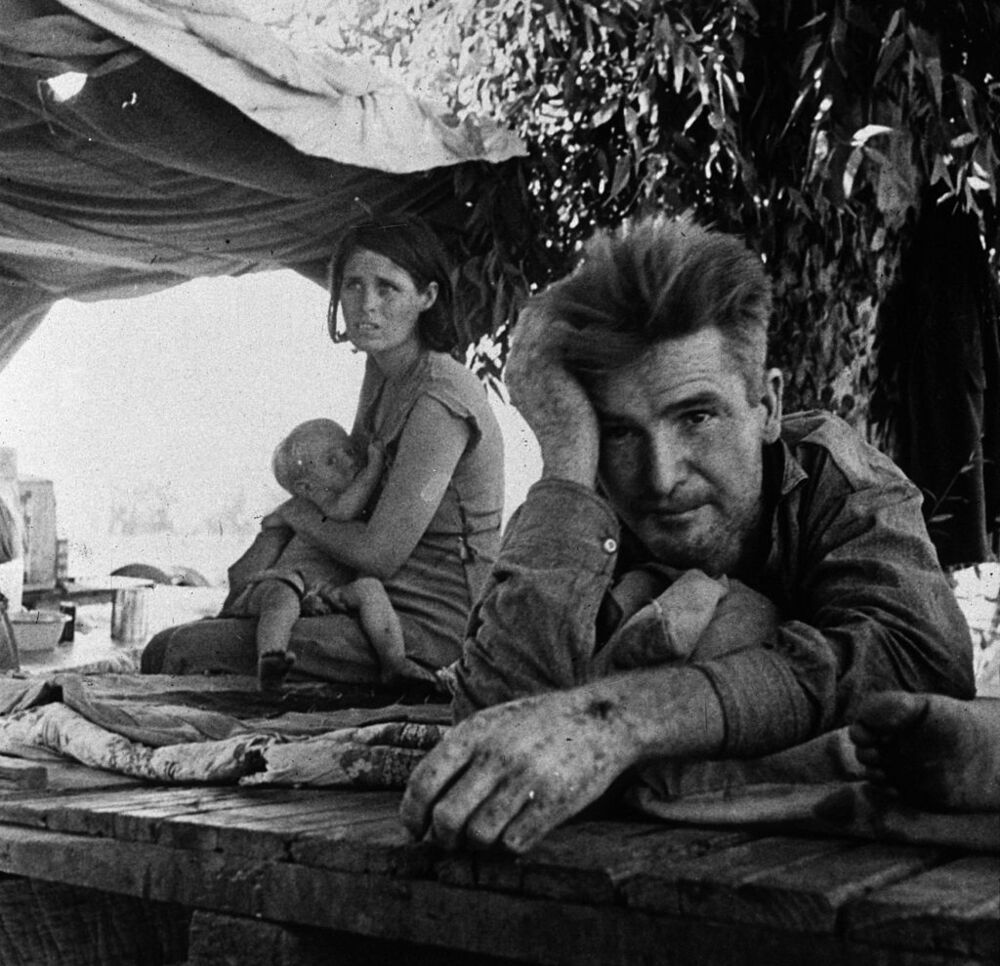

We’ve been there before. Photographer: Dorothea Lange/Hulton Archive

As the economic carnage from the coronavirus pandemic continues, a long-forbidden word is starting to creep onto people’s lips: “depression.”

In the 19th and early 20th centuries, there was no commonly accepted word for a slowdown in the economy. “Panic” was the term typically used for financial crises, while long slumps were commonly called depressions. Presidents such as James Monroe and Calvin Coolidge used the d-word to describe downturns during their administrations. There was even a slump in the 1870s that many referred to as the Great Depression at the time.

But then 1929 came, and there was no longer any doubt as to which depression deserved the modifier “great.” The crash hit the entire world, reducing economic output 15%. And it ground on mercilessly for years — by 1933, unemployment in the U.S. was at 25%. The Great Depression was so severe that governments permanently expanded their role in the economy.

Since the 1930s, economists and commentators have used the word “recession” to describe economic slumps, and none of them have been nearly as severe as the Great Depression. The only time this convention was really challenged was after the financial crisis of 2008. The global nature of the downturn, sparked by troubles in the financial industry, led many to draw parallels with the Great Depression. In the end, the term “Great Recession” stuck.

The economic damage from coronavirus, however, threatens to dwarf the 2008 downturn. More than 22 million people, or about 13% of the U.S. labor force, have already filed for unemployment:

Current forecasts are for the unemployment rate to reach 20% this month. Some predict it could go as high as 30% this year. That would eclipse even the Great Depression in severity.

So if severity alone is the criteria for a depression, this one will certainly deserve the moniker. President Ronald Reagan once quipped that “recession is when your neighbor loses his job; depression is when you lose yours.” There will be few people whose economic livelihoods are not hurt by the coronavirus.

But there are other possible criteria for deciding what gets labeled a depression. Besides severity, there’s duration; both the 1870s and the 1930s saw a decade of economic pain. Many hope that the economy will bounce back from the coronavirus in a so-called V-shaped recovery. It stands to reason that if the economy crashed because it was intentionally turned off by mandatory shutdowns, then letting people out of their houses will turn it back on.

Many of the economic relief measures now being implemented, such as the Paycheck Protection Program — which extends loans to small and medium-sized businesses that are forgiven if they retain their workers — have this sort of quick restart in mind. But while that’s a good idea, there are reasons to believe this downturn will not be over quickly.

First, there’s evidence that the main reason people are staying at home is not lockdowns but the threat of the virus itself. Data from online restaurant-reservation websites shows that in major cities, most of the decline in restaurant attendance happened before stay-at-home orders were issued. And polls indicate that most Americans are very wary of returning to their normal activities. This means that unless virus suppression regimes give people confidence that coronavirus isn’t a threat to their personal safety, they’re unlikely to come out and shop even if the government says there’s no need to worry. Because effective treatments probably won’t be available at least until the fall or later, that means many more months of business devastation except in the few competent and lucky places that get test-and-trace systems in place.

Next, there’s the global nature of the downturn. Gross domestic product is set to decline in almost every country. Some forecasters expect all economies to bounce back simultaneously, but a more likely scenario is that many countries will struggle to recover. That will hurt both U.S. export markets and international investors for years to come.

Finally, there’s the possibility of long-term financial market turmoil. In addition to severity and duration, a third common criterion for distinguishing depressions from recessions is that the former involves years of financial industry dysfunction and declines in lending.

The Federal Reserve is struggling mightily to preserve the solvency of U.S. banks and prop up asset markets, and so far it has succeeded. Interest rates are low, bank failures have not been widespread and stock markets have partly recovered:

But keeping banks on a government lifeline during years of business weakness, although better than the alternative of letting the financial system collapse, might still not equip the financial industry to do its traditional job of lending to productive enterprises. The threat of repeated coronavirus outbreaks, along with continued business failures, may make banks just as afraid to lend as they were after 2008.

Although the U.S. government can and should do its utmost to ensure that the coronavirus recession doesn’t check all the boxes for a depression, its powers to stop both the virus and the international slowdown are limited. Let’s hope this depression won’t last a decade, but an unprecedented slump followed by years of pain seems inevitable.

Megabank raises lending standards amid economic struggles to protect themselves

As the country struggles through the economic impact of the coronavirus, numerous mortgage companies have raised their lending standards to protect both borrowers and themselves. Now, one of the largest mortgage lenders in the country is joining that list.

JPMorgan Chase this week is increasing its minimum lending standards to require nearly all borrowers to have at least 20% down in order to buy a home. Beyond that, Chase is also raising its minimum FICO credit score to 700 on purchase mortgages.

Put simply, if a borrower doesn’t have a 20% down payment and a FICO score of 700 or above, they will likely not be able get a loan from Chase to buy a home. According to Chase, those lending standards also apply to refinances on non-Chase mortgages.

The bank will still move forward with refis under its previous lending standards if the loan is either serviced by Chase or in Chase’s portfolio, but for all other refis, it’s 700 FICO or look somewhere else.

It should be noted that the changes do not apply to Chase’s DreaMaker mortgage program, which makes loans available for low-to-moderate income borrowers with as little as 3% down and reduced mortgage insurance requirements.

According to Chase, the changes will allow the bank to spend more time on the loans it is working on and do the appropriate verifications to ensure the loan is the right move for all involved.

“Due to the economic uncertainty, we are making temporary changes that will allow us to more closely focus on serving our existing customers,” Chase Home Lending Chief Marketing Officer Amy Bonitatibus said in a statement.

With the changes, Chase becomes the latest lender to tighten its lending standards. Certain segments of the business, including government, non-QM, and jumbo loans, have dried up substantially as lenders pull back from loans that are seen as riskier than conventional loans. But as the crisis continues, lenders are beginning to change their conventional lending standards as well.

United Wholesale Mortgage, the second-biggest mortgage lender in the country, recently announced that it will require reverification of a borrower’s employment on the day their loan is scheduled to close. The purpose of that move is to ensure that borrowers are actually still employed when their mortgage closes.

“If people don’t have a job, I’m not going to put them in a bad position,” UWM CEO Mat Ishbia told his employees last week. “By doing this, we’re protecting borrowers, the company, and the country.”

But UWM wasn’t the only one making employment verification changes as COVID-19 pushes layoffs to record levels in the U.S. Fannie Mae and Freddie Mac recently announced that they changed the age of document requirements for most income and asset documentation from four months to two months. What that means is all income and asset documentation must be dated no more than 60 days from the date of the mortgage note.

The bottom line of all these changes is lenders are attempting to protect themselves and borrowers from getting into a mortgage that is not in the borrower’s or lender’s best interest.

And despite Chase being the biggest name to make changes like these so far, it likely won’t be the last lender to do so.

The changes to Chase’s lending policies were first reported by Reuters.

Homeowners in Italy are seeing many of their bills suspended – including mortgages – as the country deals with the coronavirus pandemic, and now other European nations are considering similar moves.

Is a “mortgage holiday” coming to America?

The short answer is: probably not. Most American mortgages are packaged into bonds with legal terms that dictate what the servicers who handle the billing can and can’t do. There are ways servicers can offer forbearance – an agreement to let borrowers either pay at a lower interest rate or suspend payments temporarily because of a hardship. But it’s on a case-by-case basis.

“Somebody owns those bonds,” said Mark Vitner, a senior economist with Wells Fargo. “Who is going to make those interest payments?”

Any missed or reduced payments typically have to be repaid, with interest. Sometimes, that means the loan will be re-amortized, so whatever you don’t pay now, you’ll be paying off over the remaining years of your loan, with interest.

America’s mortgage market is much bigger than Italy’s $423 billion of outstanding home-loan debt. The U.S. has about $11 trillion of mortgages on one- to four-family homes, according to Federal Reserve data. More than half of that is contained in bonds compiled and backed by Fannie Mae and Freddie Mac.

The Federal Housing Finance Agency, which oversees those government-controlled mortgage securitizers, issued a directive last week urging servicers to offer help to people who fall behind on mortgage payments because of the coronavirus pandemic.

“To meet the needs of borrowers who may be impacted by the coronavirus, last week Fannie Mae and FreddieMac reminded mortgage servicers that hardship forbearance is an option for borrowers who are unable to make their monthly mortgage payment,” said FHFA Director Mark Calabria. “For borrowers that may be experiencing a hardship, I encourage you to reach out to your servicer.”

In addition, regulators such as the Federal Reserve on Tuesday urged U.S. banks such as Wells Fargo and JPMorgan Chase to work “constructively” with borrowers affected by the coronavirus outbreak, promising they won’t get dinged by examiners as long as the measures show good judgment.

Italy has been the nation with the biggest outbreak of COVID-19, the disease caused by the new coronavirus, outside of China. Italy has more than 15,000 cases, and more than 1,000 people have died, according to Johns Hopkins University.

While Italy is the only government to introduce a plan to suspend mortgage payments for people affected by the lockdown – and so far it’s only for the worst-hit areas of the nation – other European countries may follow suit, according to an S&P report.

“New monetary and fiscal stimulus measures are currently being launched daily and the Italian government is contemplating broadening the mortgage payment suspension scheme nationwide,” S&P said.

“Some banks and governments in other countries, including France, Spain, and the U.K., have mooted similar measures, although the potential scale of eligibility and level of uptake among borrowers could vary widely and are not yet known,” the report said.

The minority homeownership rate increased to 48.6 percent in the fourth quarter of 2019, up 0.8 percentage points from the fourth quarter of 2018, according to a new data release from the Census Bureau’s Housing Vacancies and Homeownership survey (CPS/HVS) (Figure 1). This is the highest it has been since the third quarter of 2011 (48.9 percent). This year-over-year gain is higher than the gain in the overall U.S. homeownership rate, which rose 0.3 percentage points to 65.1 percent in the fourth quarter of 2019 (a six-year high). A separate Eyeonhousing.org post covers the U.S. homeownership rate in more detail.

Breaking down the minority homeownership rate shows that the Hispanic homeownership rate gained the most in the fourth quarter, with a 1.2 percentage point increase to 48.1 percent (from 46.9 percent in the fourth quarter of 2018).

The black homeownership rate posted the second largest gain of 1.0 percentage points to reach 44.6 percent in the fourth quarter of 2019 (from 43.6 percent in the fourth quarter of 2018). This is the largest quarter gain in the black homeownership rate since the first quarter of 2017.

Meanwhile, Other households (Asian, Pacific-Islander, Native American, and other race households) experienced a decline in their homeownership rate, dropping 1.0 percentage points to 57.1 percent (from 58.1 percent in the third quarter of 2019). The Other homeownership rate has now declined for four consecutive quarters (year-over-year declines), which is in contrast to strong gains seen for this group between the second quarter of 2017 and the third quarter of 2018.

The white homeownership grew by only 0.1 percentage points to 73.7 percent in the fourth quarter (from 73.6 percent in the fourth quarter of 2018). The white homeownership rate has not declined year-over-year since the first quarter of 2017 (Figure 2).

Mortgage rates are still relatively low, and a healthy job market has helped to make homeownership more affordable. In fact, housing affordability was at a three-year high in the third quarter of 2019, according to the National Association of Home Builders’ Housing Opportunity Index (HOI). These factors are most likely contributing to the recent upticks in the overall and minority homeownership rates.

As 2019 saw historically low vacancy rates among multifamily housing, it also led to a rising cost of rent, too.

According to realtor.com, a report from Abodo said rental prices went up in 38 states, including Washington, D.C., in 2019. In the other 12 states, the cost of rent actually fell, but only slightly.

Nationally, median rents for one-bedroom units went up 4.1%, making monthly rent $1,078 at the end of 2019.

Prices for two-bedroom units went up 5.5%, making monthly rent $1,343.

In 2019, multifamily occupancy rates reached as high as 96.3%. The demand of multifamily housing keeps rising, as home prices are also continuing to climb.

According to realtor.com, rental prices surged the most in Utah. There, rent went up 3.78% in 2019, reaching $965 for a one-bedroom unit.

“In states like Utah, people are relocating for jobs,” Abodo said in its report. “Many folks are coming from California and other high-priced hubs. People need to find places where they can live and afford to live a lifestyle that they want.”

Renting cost the most in Massachusetts, where the average one-bedroom unit cost $2,218 a month.

Renting surged the most in Detroit, where cost of renting a one-bedroom went up 7.48%, making rent $886 a month.

“They’re seeing a housing boom,” Abodo continued. “There are more people moving there, which increases the demand for housing as the city begins to come back. New construction has actually started there, which is obviously going to cost more.”

The highest rents in the nation were, at no surprise, San Francisco and New York City. On average, renting a one-bedroom unit was $3,877 and $3,082 a month, respectively.

Renters in Montana saw the biggest price cuts in 2019. Rents fell 1.6%, to an average $745 a month for a one-bedroom unit.

Average prices fell the most in Dayton, Ohio, in 2019, falling 4.11%. This made renting a one-bedroom unit $758 a month. Toldeo, Ohio also had the best deal, where rents were just $517 a month for a one-bedroom unit.

The Town Board on October 15 held its first work session on the the Town’s 10 year Capital Plan which runs from 2020 through 2029; we also met with Planning Board Chair Deirdre Courtney-Batson to discuss the size, composition and number of subcommittees to develop a new Town Comprehensive Plan; 321 Bedford Road and 74 Main Street (Bedford Hills Community House); making headway in discussions with the NYC Department of Environmental Protection for Phase II for sewers; making headway for the possible acquisition of 56 acres which includes the Buxton Gorge for passive recreational use (trails).

NEW POSTS

Highlights of the October 15Town Board Meeting Work Session on 2020 Capital Plan At this first work session on the Capital Plan, Comptroller Abraham Zambrano provided a high level view of any proposed changes in the existing Capital Plan (including any project expansion), any new projects and any projects which may be deferred. We anticipate increasing the scope of renovations to the Bedford Hills Community House and carry out the work in 2020 rather than spreading it out over several years (neither a “gut” renovation nor additions are being considered). The architectural firm selected (see below) will incorporate recommendations and plans which are provided through the energy audit now under way, including the feasibility and cost effectiveness of geothermal/heat pumps. Approval of Geothermal Feasibility Study Other project changes include carrying out in 2020 and 2021 HVAC system replacements reaching the end of their useful lives (here, too, geothermal/heat pumps are under consideration); commuter lot improvements such (lighting, landscaping, etc.); roof and gas boiler replacement for the Recreation & Parks Department maintenance building; security systems for the Town House and 425 Cherry Street; IT upgrade/replacements; improvements to the commuter lots (lighting/landscaping); rooftop solar installations; hamlet center improvements (Bedford Hills and Katonah in 2020 following the completion of the sewer system); Todd’s Pond engineering study; further funding for tree maintenance and plantings; and an increase in funding for the work of the Cemetery Advisory Committee with work on our historic Town cemeteries . Some changes would be deferral until 2022 of a municipal parking lot in Bedford Village (Bedford Presbyterian Church, owner of the land which the Town would purchase for the vacant lot is not inclined to proceed at the time with sale of the property). We also are deferring improvements to the Crusher Road highway facility. The Board scheduled another work session on November 7 at which we’ll hone in further on the schedule, debt service which would result from the bond issuance. In this connection later in the meeting, the Board appointed Douglas Goodfriend of Orrick, as bond counsel, who would prepare bond resolutions first quarter of 2020 to implement the first two years of the Capital Plan. Please see Comptroller Abraham Zambrano’s Summary Memo

Honoring Assistant Chief James Fayette Lawrenceof the Katonah Fire Department Deputy Chief Dean W. Pappas was on hand to participate in paying tribute to Katonah Fire Department Assistant Chief James Fayette Lawrence. Sixty years ago, on October 6, 1959, he gave his life in the performance of his firematic duties: and today, remains the only Katonah Firefighter to have died in the line of duty. Chief Lawrence was responding to a bush fire at the Ramsey Hunt Estate on Mount Holly Road and, while fighting the fire with other Katonah Volunteer Firefighters, became entangled in a fallen 4,600 volt high tension line. His fellow firefighters pulled him off the line with pike poles and attempted to revive him.Despite over 45 minutes of heroic effort, Chief Lawrence died at the age ofthirty nine. Chief Lawrence’s sacrifice was yet another indication of his community commitment and dedication as a lifelong resident of the Hamlet of Katonah. The Town Board presented to Deputy Chief Pappas a proclamation honoring the memory of Chief Lawrence, a man who was driven purely by his love and devotion to everyone around him and whose kindness and bravery in the face of danger always made an impact on this community and will continue to inspire others.

Work Session on Preparing a New TownComprehensive Plan The Town Board’s meeting with Planning Board Chair Deirdre Courtney-Batson started with a work session to discuss the role of each subcommittee and skill sets and experience sought for individuals to be appointed. We moved to an Executive Session to discuss those interested in being appointed. I anticipate we’ll make appointments at the November 7 Town Board meeting. For further information on the subcommittees please see my previous discussion.

Update and Report of Cemetery Advisory Committee Cemetery Committee chair Jenny Weisburger presented a report to the Town Board on the work of the Committee and Friends of the Bedford Burying Grounds. Over several years the Committee and the Friends of the Burying Grounds have made significant strides in repairing gravestones and reconstructing walls. She explained another one of the Cemetery Committee project that is to explore the potential to provide new interment plots that are associated with the increasing trend of cremation. The Cemetery Committee discussed with consultants that the focus of expansion be on cremation burials as opposed to full, traditional burials. The proposed expansion of the cemetery would be low impact on Bedford’s historic cemeteries while benefiting Bedford residents who intend that their ashes be buried here.

Congratulations on Appointments to theComplete Count Committee The 2020 United States Census is of critical importance to the Town of Bedford; its data affects funds available for our schools, housing, seniors, low and moderate income populations, sales tax revenue, grant awards; business decisions; redistricting; emergency planning; fire departments; hospitals and much more. The Town Board of the Town of Bedford recognizes the critical importance of ensuring that the 2020 United States Census counts every single individual in the Town of Bedford. We congratulate the following appointees to the Census Committee: Jodi Kimmel (Chair)(Fox Lane Middle School)Joe Ruppenstein (Veterans Committee)Joanne Marcus (Senior Committee)Noya Guerrero (Community Center of Northern Westchester)Rev. Merle McJunkin (Antioch Baptist Church; Non-Resident associate member).

Proposal of FBS for Parking ViolationsManagement Services. The Town Board approved FBS Justice Solutions proposal to the Town Board for parking violations management services. FBS will provide the necessary handheld equipment and related software that will integrate parking enforcement and the Court’s need to manage such enforcement. Based on the Town’s current needs, it was recommended that the Town Board approved engaging FBS to provide services that will facilitate the management of the parking enforcement. The Board authorized proceeding with FBS’ option plan under which the Town purchases equipment. Proposal 2

Town Board Decision Not to Proceed with proposal of Homeland Towers for a cell tower at the Town property at 425 Cherry Street. At its meeting on October 7, after careful consideration of a number of issues, the Planning Board determined that it must recommend against the use of the Town property at 425 Cherry Street as the location to the Town Board a proposed Homeland Towers cell tower. In particular, the Planning Board found that, based on the visual analysis provided by the applicant, a 150’ tower at either of the two proposed locations at 425 Cherry, would have an unacceptable visual impact on the heart of the hamlet of Bedford Hills. The Board approved the Planning Board’s recommendation not to proceed with the Homeland Tower’s proposal.

Proposed Architect for Facility Assessment ofBedford Hills Community Center Deputy Supervisor Lee Roberts, Councilwoman MaryAnn Carr and I have been working with Recreation and Parks Superintendent Chris Soi, BuildingInspector Al Ciraco and Director of Energy and Sustainability Mark Thielking regarding improvements to the Bedford Hills Community House. Chris Soi requested the Town Board select an architectural firm to perform an assessment and study to establish a scope of work and project budget for the proposed capital improvements to the Bedford Hills Community House. Based on the pricing provided in the proposal of architects KG&D, the Board approved $14,500.00 to perform the study which would be funded from the existing Bedford Hills Community House Capital Project account. There will be a “gut” renovation, however, the scope of work will include among other components: interior development, renovations to multiple facilities and exterior restoration. The Board approved the implementation and completion of the study, and not at this time additional architectural services. This study is a critical step as the Town Board is considering Bedford Hills Community House capital improvements in formulating the 2020-2029 Capital Plan. The study will be completed in early/mid November. Letter of Intent KGD Proposal

EARLY VOTING STARTS OCTOBER 26 For the first time in history, New Yorkers have a choice: Vote Early October 26 through November 3at Mount Kisco Town HallORVote on Election Day, November 5at your regular polling place.It’s simple:Town of Bedford voters may vote earlyOctober 26 through November 3 atMount Kisco Town Hall, 104 Main Street

Bedford Public Works Dept. PAVING NOTICE UPDATE

Public Notice to all residents regarding Road Paving in Bedford NY for October 2019. The Town of Bedford plans on several days of road paving. Work will begin Monday, Oct. 7, 2019 and last through Friday, Oct. 18 (inclusive.) We will NOT be paving Saturday, Oct. 12, Sunday, Oct. 13, or Monday, Oct. 14 (Columbus Day). Roads to be paved at this time include:CHURCH STREETSUNSET DRIVE (Bedford Hills off of Main St.)SEMINARY ROADDAVID’S WAYDAVIDS HILL ROAD (The paved hill) Commuters could experience temporary disruptions to traffic and access as paving operations commence. Residents are asked to refrain from parking on these streets as paving proceeds. The precise scheduling of work depends upon weather conditions and the proper operation of paving equipment. Therefore your patience and understanding are appreciated. Keep in mind that it is possible that rain events or paving equipment issues may push back the paving schedule a day or two. Paving will be preceded.by road milling on Cherry Street and Sunset Drive as well as the milling of some key cuts to the intersections and to some driveways where key cuts are considered beneficial. If you have any further questions regarding this matter, please feel free to contact Bedford Public Works Department at 914-666-7669.

COMMUNITY EVENTS CALENDARWEEK OF 10.18-10.26Click here

OTHER NEW POSTS

HELP WANTED – Part-time Interns! The Supervisor’s office is seeking a few high school studentsto intern a few hours a week through the fall. Community service hours will be honored while learning about local government. Take photos, get web skills, learn about your town! This is a fun position that will give you a broad range of experiences.Please send an email to pcohen@bedfordny.gov

Attention Residents ofBedford Central School District I first wish to thank members of the community for contacting me and meeting with me to discuss their concerns about possible school closures. We are extremely concerned about the impacts, and will be actively engaged in the discussions. Part of what I intend to do is to help get the word out of forums and meetings which BCSD is holding regarding its facilities plan. Please try to attend and participate. It is critical to the education of our children and our community generally. From the BCSD flyer on community forums for long-range facilities plan: “Bedford Central School District invites all members of the community to attend one of our open community forums about the district’s developing Long-Range Facilities Plan.” These forums encourage Bedford citizens to share their thoughts, hopes, and ideas for the future.”

HOURSSat/Sun: 12 PM through 5 PMMon/Wed/Fri: 8 AM through 4 PMTue/Thu: 12 PM through 8 PM

You also may call Town Clerk Boo Fumagalli at 914-864-3868 or e-mail her at lfumagalli@bedfordny.gov

The 2020 Census – JOBS! DID YOU KNOW? There are jobs available right now for the 2020 Census. 2020 census.gov/jobs or call 1-855-JOB-2020 The U.S. Census Bureau is recruiting thousands of people across the country – especially field jobs ascertaining addresses and census takers. Hours are flexible and the pay rate is quite competitive at $21.00 per hour for a census takerin Westchester County And as a resident getting paid for your work, if you are assigned to Bedford, you will be helping your town get a complete count.

REMINDER

It’s Leaf Blowing Season –Change Over in Rules Affecting Hamlet Zones

Saturday October 19The Annual 5th GradePancake Breakfast 7:30am-11:30am

Bedford HillsElementary School123 Babbitt Road Bedford Hills All are welcome. Proceeds to fund the5th Grade Class Trip.

ART STROLL – OCTOBER 19 FROM 5PM -8 PM

OCTOBER 20 FREE RABIES VACCINES FOR WESTCHESTER PETS Westchester County residents can bring their dogs, cats and ferrets in for free rabies vaccinations on Sunday, October 20 from 11:30 a.m. to 3:30 p.m. at the Humane Society of Westchester, 70 Portman Road in New Rochelle. Walk-ins are welcome; no appointments are needed. Call 914-632-2925 for more information. Cats and ferrets must be in carriers and dogs must be on a leash. Aggressive dogs must be muzzled. No examinations will be given and all pets must be supervised by an adult. “Vaccinating your pet against rabies will protect your pet and your family in case your pet has contact with a rabid or potentially rabid animal,” said Westchester County Health Commissioner, Sherlita Amler, MD. Under New York State law, dogs and cats must receive their first rabies vaccine no later than four months after birth. A second rabies shot must be given within one year of the first vaccine, with additional booster shots given every one or three years after that, depending on the vaccine used. Owners who fail to get their pets vaccinated and keep the vaccinations up-to-date may be fined up to $2,000. Rabies is a fatal disease that spreads through the bite or saliva of infected animals. Those animals most commonly infected are raccoons, skunks, bats and foxes. However, domestic animals such as cats and dogs are also at risk because they can easily contract rabies from wild or stray animals. BOOSTER INFO: A pet that is up-to-date with its rabies vaccinations would only need a booster dose of vaccine within five days of the pet’s exposure to a known or suspect rabid animal. Animals not up-to-date with rabies vaccinations would be quarantined or euthanized following contact with a rabid or suspect-rabid animal. SIGNS OF RABIES: A change in an animal’s behavior is often the first sign of rabies. A rabid animal may become either abnormally aggressive or unusually tame. It may lose fear of people and become docile, or become excited and irritable. Infected animals sometimes stagger, spit and froth at the mouth. Adults should encourage children to avoid touching unfamiliar animals, and to immediately tell an adult if they have been bitten or scratched by an animal. All animal bites or contacts with animals suspected of having rabies must be reported to the Westchester County Health Department at (914) 813-5000. After hours, callers should follow instructions in the recorded message for reporting public health emergencies 24 hours a day. To learn more about rabies and its prevention, visit the Health Department’s website at www.westchestergov.com/health, like us on Facebook at facebook.com/wchealthdept or follow us on Twitter @wchealthdept.

SAVE THE DATES!

The Bedford Hills Neighborhood Associationinvites you to The 1st Annual

Bedford Village: Update on Proposal for a New Firehouse/ Emergency Services Department Bedford Village Fire Commissioner Heather Feldman has provided me the following update… As was shared last week, we will use this space to address FAQs as they arise. Please email any questions to: NFC@bedfordfire.com and note we may edit the question for space and clarity. Q. Some communities (Katonah, Pound Ridge, Bedford Hills) split their emergency services into two departments – Fire and Emergency Medical. Why do we not have the same two-pronged structure in Bedford?A. Since our founding in 1923, the Bedford Fire Department has provided both fire and emergency medical response from a single site, and a dedicated ambulance to cover medical calls since the 1950’s. We have always believed that the community is best served from a single location so to fully leverage financial and operational efficiencies. If we were to split out our EMS agency, the Bedford Village community would then have to manage and maintain two separate properties and two buildings, engage two separate corps, identify two separate administrative bodies, and fund two separate department budgets. Moreover, having both fire and EMS volunteers integrated into a single department allows for greater professional familiarity among the corps, resulting in a more coordinated crisis response. Simply put, the BVFD model minimizes costs and maximizes service. Q. I’ve heard that an exercise room for the first responders is being considered for the new building. Can you explain the rationale behind that decision? It seems very indulgent!A. New York State requires Fire Districts to provide their first responders access to physical fitness facilities. These guidelines allow our volunteer firefighters and EMTs to attain the strength, agility, and stamina needed to handle the myriad crises that they confront each day. The vast majority of modern firehouses have in-house fitness equipment. Having this resource on site helps keep our volunteers at the firehouse, reducing emergency response times. Additionally, there is an economic advantage to providing this important professional development resource — currently, the BVFD spends approximately $15,000 of taxpayer funds per year to cover the costs of gym memberships of our volunteer corps. Putting an exercise room in a 75-year facility will save money over the long term.

*Each week, we will look forward to addressing a question about the revised project that has emerged.Please email your questions to: NFC@bedfordfire.com and please note we may edit the question for space and clarity.

Sharing the Road for Motorist & Cyclists There is nothing better than getting out to enjoy a ride on a clear, crisp autumn morning. But there needs to be a partnership of shared responsibility of both the cyclist and motorist to keep everyone safe. Responsibility of the cyclist: Wear a helmet.Be visible. Reflectors, lights, and reflective clothing help motorists see you. Follow traffic laws. Cyclists must follow the same traffic laws as motorists. Be predictable. Give motorists a sense of your direction and provide signals to show motorists your intentions to turn. Share the road. Try to stay as far to the right side of the roadway as safety allows. Do not impede traffic. Cyclists may ride a maximum of two abreast as long as normal traffic flow is not impeded.Be alert and try to anticipate potential conflicts before they occur. Responsibility of the motorist: Be Patient. Only pass a cyclist when there is adequate site distance to do so without impacting oncoming traffic.Share the road. When passing a cyclist, be sure to provide a minimum of three feet of buffer between you and the rider.Right hand turn awareness. Avoid cutting off a cyclist by making a right hand turn in front of them.Lookout for cyclists. When entering a roadway, don’t just check for cars, keep an eye out for cyclists too. Working together will keep everyone safe and we can all enjoy the beautiful roads of Bedford.

Autism Registry formsAn Autism registry has been implemented on the Bedford Police Department website. The Bedford Central School District has been given access to the forms to distribute to students and parents. You can also download the forms here.

UPDATE for AT&T Cell Service CustomersOther Internet Service Issues?My thanks for the post on the Katonah Parents Facebook group alerting me to the AT&T cell service outage (the mention of my name on KPFG triggered an e-mail notification to me – it worked!). And thanks as well to those who e-mailed us with the specifics. We were in touch with AT&T Wireless on Wednesday and Thursday who contacted their field team. Yesterday, I was put in contact with an AT&T representative higher up in the food chain. I don’t know whether she was responsible for the service restoration or whether it was in the works anyway. In any case I now have a person I can go to other than those lower down who we went to earlier this week when you folks alerted us to the problems. So please do let us know if you have any continuing or future service problems and we’ll do our best to get it taken care of. Thanks for your patience. And going forward, for anyone having service issues, here are some numbers: Customer Service for Verizon /Fios: 1 800 922 0204 Customer Service for Optimum/ Altice: 718 860 3513 Customer Service for AT&T (cell phone service): 800 288 2020 We’ll try to help after you’ve exhausted your options with customer service support. Please feel free to contact Phyllis Cohen at pcohen@bedfordny.gov or me and provide the following: NameAddressAccount numberPhone number(s)E-mail addressDescription of the issue (dates of intermittent or lack of service, etc.)

PRIOR POSTS OFCONTINUED RELEVANCE (cont).

The I-684$13 Million Paving Project Front row (l to r:) Lee Roberts, Kate Galligan, Kitley Covill, Chris Burdick, Shelley Mayer, Andrea Stewart Cousins, Marie Therese Dominquez, Peter Harkham, MaryAnn Carr. Back row: Don Scott, David Buchwald, Lance MacMillan.\

On Thursday, September 12, I joined State Senator Shelley Mayer, State Senate Majority Leader Andrea Stewart-Cousins, State Senator Peter Harckham and Assemblyman David Buchwald in a press conference celebrating the I-684 paving project at long last coming to fruition. We were honored to be joined by New York State Department of Transportation Commissioner Marie Therese Dominguez. READ MORE

Agreement with NYS Department of Environmental Conservation for $1 Million Grant for Sewer ProjectREAD MORE

Adoption of New Local LawRegulating Sale of Vape Products The Town Board held a public hearing to implement a settlement of litigation against the Town which resulted in an injunction against the Town barring enforcement of our existing vape law. READ MORE

Reminder – No Knock Registry Law We are receiving reports of unscrupulous, deceptive and fraudulent tactics of door to door salesman. Please be reminded that the Town Board amended its solicitation law to provide a No Knock Registry. It prohibits such solicitation to the homes of residents who complete a request to be listed on a “no knock registry”. The law does not infringe upon political, educational or religious activities. READ MORE

New Collective Bargaining Agreementwith our Office Workers The negotiating teams of the Town of Bedford and the Teamsters 456 – White Collar Unit, which represents the Town’s office workers, met several times starting on January 25, 2019 to negotiate a new Collective Bargaining Agreement (CBA) for the period January 1, 2019 through December 31, 2022. READ MORE

SENIOR NEWS

Become of member of your Bedford Playhouse. Discounted membership for ages 62+ Sign up here

Living Green

Leaf Discount ProgramExtended untilJanuary 2, 2020READ MORE

Thanks to a grant from New York State Energy Research & Development, homeowners in the towns of Bedford, Lewisboro and Pound Ridge now have a unique opportunity to determine whether heat pumps might provide a more comfortable home while saving on energy bills. Heat pumps draw from either the ambient air (air source pumps) or the earth (geothermal pumps). Geothermal provides a constant temperature of about 54 degrees allowing for heating in the winter and cooling in the summer. The program is spearheaded by Energize NY, in partnership with Sustainable Westchester, Abundant Efficiency and NYSERDA, provides homeowners in the three towns the opportunity to learn whether these new renewable energy choices are right for you. Energize has launched an ambitious community outreach program to introduce homeowners both to the technology and reputable, certified heating and cooling and energy efficiency experts who offer the latest clean energy technologies including air source and geothermal heat pumps and energy efficiency improvements. The contractors are Bruni & Campisi (914-269-6760), Healthy Home Energy & Consulting, Inc. (9144-242-9733) and Dandelion Energy (833-436-4255) On Thursday, June 26, the Heat Smart team was on hand for the community to explain the program (together with service Tacos). Like to know more? Please click on this link https://www.heatsmartny.com/westchester or call 914-302-7300 x1 There is no cost or obligation to learn whether Heat Smart is right for you. Our thanks to Lauren Brois, Bedford 2020, the contractors and the Heat Smart campaign team for an excellent presentation.

Beaver Dam Yard Waste and Compost Facility The Town of Bedford Beaver Dam Compost Facility processes recyclable wood waste and leaves from the Town and provides beneficial reuse of the waste as compost and mulch. The facility provides an extremely cost effective method for this recycling as well as an environmental benefit of local recycling with minimal transportation requirements. It is open for residents to dispose of recyclable wood waste (logs and branches up to 6” diameter, brush, and leaves), as well as pick up wood mulch and leaf compost. This service is free to Town of Bedford residents between 7:30 AM and 3:00 PM Monday to Friday, excluding Town holidays. With Spring clean-up and planting season here, you may find these services helpful. I encourage you to review the updated information by clicking on Beaver Dam Compost Facility on the Town’s website.

“The master’s tools will never dismantle the master’s house,” penned poet and activist Audre Lorde. Pulled from a 1984 essay, the quote summarizes her larger argument that mainstream academic frameworks are incapable of permitting the disruption of their own status quo. “They may allow us temporarily to beat him at his own game, but they will never enable us to bring about genuine change,” wrote Lorde.

Over the last few months, several Democratic presidential hopefuls—namely Sen. Kamala Harris (Calif.), Sen. Elizabeth Warren (Mass.), and South Bend, Ind. Mayor Pete Buttigieg—have released housing proposals that utilize a curious vector to implement their respective remedies for historical discrimination: redlining maps.

Redlining was the practice of outlining areas with sizable Black populations in red ink on maps as a warning to mortgage lenders, effectively isolating Black people in areas that would suffer lower levels of investment than their white counterparts. The Democratic candidates hope that the contours of these old maps—once used by the government-sponsored Home Owners’ Loan Corporation (HOLC) from 1933 to 1977—offer the blueprint for closing the racial homeownership gap and increasing prosperity among largely Black and Brown Americans who were robbed of wealth for generations under redlining’s legal discriminatory policy.

Redlining was the practice of outlining areas with sizable Black populations in red ink on maps as a warning to mortgage lenders, effectively isolating Black people in areas that would suffer lower levels of investment than their white counterparts.

In each plan, redlining maps are used to determine eligibility for beneficiaries, to differing degrees:

Harris’s plan would invest $100 billion in assistance for down payments and closing costs, to be made available to those who have lived in government or rental housing for 10 or more preceding years in a formerly redlined area that is low-to-moderate income today. Grantees must also earn less than a maximum annual family income.

Warren’s plan would offer down payment assistance to first-time homebuyers in formerly redlined areas or low-income areas that experienced other forms of legal segregation, qualifying them for a grant applicable to a home anywhere in the country. The proposal is billed as a “first step towards closing the racial wealth gap,” and would be paid for by an estate tax.

Mayor Buttigieg’s plan proposes the Community Homestead Act, which would purchase abandoned properties in select cities and allow residents to acquire them. Eligible grantees include residents who earned less than the area median income over the last five years and either have resided in the area for at least three years, or have resided in any historically redlined or racially segregated area for at least three years.

However, based on our analysis of who lives in these formerly redlined districts today, Lorde’s quote should be considered when it comes to these proposed remedies.

The University of Richmond’s Mapping Inequality project has digitized scans of the HOLC redlining maps held in the National Archives. Examination of the maps, numbering over 200, reveals that approximately 11 million Americans (10,852,727) live in once-redlined areas, according to the latest population data from the Census Bureau’s American Community Survey (2017). This population is majority-minority but not majority-Black, and, contrary to conventional perceptions, Black residents also do not form a plurality in these areas overall. The Black population share is approximately 28%, ranking third among the racial groups who live in formerly redlined areas, behind white and Latino or Hispanic residents.

While still a tremendously large population, the approximately 3 million Black residents in redlined areas account for just 8% of all non-Latino or Hispanic Black Americans. Given the demographic shifts that have occurred since the federal government started using color-coded maps to assess mortgage risk, and the relatively small share of the Black population currently living in these areas, proposals that center on these past tools to redress discrimination probably won’t “dismantle the master’s house.”

THE PAST STILL HAUNTS US

Together with racially restrictive housing covenants that prohibited Black Americans from buying certain properties, redlining prevented generations of families from gaining equity in homeownership or making improvements to homes already owned. These unjust practices form part of a long history of discrimination, which has contributed to the disparities in homeownership and wealth still observed between the Black and white populations of the country today.

Redlined neighborhoods are generally located near the center of urban areas, where Black people were concentrated when the government generated the maps used today for the Harris, Warren, and Buttigieg proposals. But since then, transformational demographic shifts have spread different populations throughout metropolitan areas and increased the size of those areas overall. To assess the relative residual social patterns across redlined communities today, we compare the aggregate of the census block groups that fall within the redlined areas of each city to the remaining non-redlined areas in the same cities, and measure ways the two areas differ.

These localized comparisons show that in cities with a history of redlining, the redlined areas today generally remain more segregated and more economically disadvantaged, with higher Black and minority shares of population than the remainder of the city. Additionally, they have lower median household income, lower home values, older housing stock, and rents which are lower in absolute terms (but often higher as a percentage of income). Similar studies have confirmed these trends for other social characteristics, as well as a clear correlation showing more positive current-day outcomes for areas that were “greenlined.”

The selected characteristics in the group of the ten most populous redlined areas diverge less sharply than in the remaining smaller areas, suggesting that for smaller areas, the residual effects of redlining are perhaps felt more clearly.

This top-heavy slant of the population distribution poses an issue for policymakers who wish to use HOLC maps to address the legacy of past discrimination, as it is not the case that half of the homeownership and wealth gaps can be attributed to disparities among Black and white residents of those ten cities alone. Furthermore, Black-majority suburbs are on the rise, which are heavily underrepresented in HOLC maps due to their focus on urban centers.

WHO NOW LIVES IN ONCE-REDLINED AREAS?

In some places, redlined areas track with conventional perceptions. For example, in Birmingham, Ala., the redlined portion has a much higher concentration of Black residents than the rest of the city, as well as lower incomes and property values. Formerly redlined Birmingham is majority-Black, and a large share of the Black citizens of Birmingham reside in formerly redlined areas.

The racial history of Birmingham is one of sustained aggression against the Black population. The persistence of demographic patterns in formerly redlined Birmingham is a testament to informal and formal enforcement of spatial placement by local, state and private forces. In cities throughout the South with a similar demographic makeup and history of racial violence, policies of targeted assistance in redlined areas could prove useful in closing the local racial homeownership and wealth disparities. However, at the regional and city level across the country, we find wide variations in the demographic makeup of who lives in formerly redlined areas (both in absolute numbers and relative to the cities in which they are found).

Some redlined areas have a lower Black share of population than the rest of the city

Theoretically, if the effects of redlining had faded completely over time, demographics and socio-economic outcomes between redlined areas and the surrounding city would be indistinguishable. Of course, this is not the case, but the degree to which the Black versus non-Black population of a given redlined area matches the area around it varies greatly across cities. Of the 174 principal cities in the comparison, 114 showed a statistically significantly higher concentration of Black population in the redlined areas than the rest of the city. In 26 more, the concentration was higher but not statistically significant.

Six of the 34 cities which inverted this trend (a redlined area with a lower Black share of the population than the rest of the city) are among those 10 large cities which are home to half the redlined population: Detroit, Baltimore, Milwaukee, Boston, Los Angeles, and Philadelphia. Each of the six have sizeable Black populations, and Black people form the largest racial group in Detroit, Baltimore, and Philadelphia. And despite a demographic shift, the redlined portions of these cities still exhibit negative economic outcomes.

Clearly, these areas have suffered from a legacy of divestment, and deserve attention from policymakers. But a strategy to close the racial wealth gap that focuses mainly on these now-diversified locations risks overlooking Black neighborhoods elsewhere.

Some redlined areas, especially in the West, have a small Black population relative to white or Latino or Hispanic residents

Los Angeles is home to the third-most populous formerly redlined area, encircling over 620,000 people. Today, 70% of this group is Latino or Hispanic, 12% is white, and 6% is Black.

In 1930, nine years before the HOLC map was produced, census data showed that the whole city’s population was 88% white, 8% Mexican (the closest proxy to the Latino or Hispanic population from the time), and 2% Black. Even so, language from the original HOLC map makes explicit reference to Black neighborhoods. An excerpt from a map encompassing today’s central Los Angeles neighborhood of Jefferson Park derisively writes:

This is the “melting pot” area of Los Angeles, and has long been thoroughly blighted. The Negro concentration is largely in the eastern two thirds of the area. Original construction was evidently of fair quality but lack of proper maintenance is notable. Population is uniformly of poor quality and many improvements are in a state of dilapidation. This area is a fit location for a slum clearance project. The area is accorded a “low red” grade.

While redlined areas in Los Angeles largely did and still do encompass far more Latino or Hispanic residents than Black residents, property appraisals and neighborhood assessments were constantly undertaken from a distinctly anti-Black point of view. However, the demographic reality of redlined Los Angeles today means that policies implemented here to close the Black homeownership gap would miss the target population. Of course, the country experiences a Latino or Hispanic homeownership gap as well, which merits intentional consideration from policymakers. But Latino or Hispanic Americans should not be merely an incidental benefactor of policy directed at addressing historic discrimination against Black people.

Some redlined areas are too small to be a useful target for policy

Dallas is a city with a long history of intense discrimination. Today, Dallas remains segregated along lines of race and income, but the HOLC map is surprisingly small. In the 80 years since the map was drawn, the city has grown five-fold. Today, the city of Dallas hosts over 1.3 million residents (including roughly 300,000 Black residents) but has a redlined population of just over 28,000. Policies to address redlining specifically would have little effect on racial homeownership and wealth disparities in Dallas.

Washington, D.C. is noticeably absent from discussions of redlining. The reason is simple, and reveals one of the most intractable problems with using these maps to guide policy implementation: We simply do not have any record of a redlining map drawn for 1930s Washington. While it is difficult to imagine the District—long known as “Chocolate City”—being spared from a nationwide effort targeting Black residents, it is not hard to find examples of place-based discrimination that happened in the nation’s capital in the 20th century and continue today. Discriminatory lending at the local level does not require a federally commissioned map, but it helps.

If the 2020 presidential candidates and other federal policymakers wish to close the homeownership and wealth gaps, efforts cannot be considered complete without including the city of Washington. Without a map to guide them, a new system must be devised for implementing policy there. And if that can be accomplished for Washington, then it can be accomplished nationwide.

Other places which display this pattern: all but some 200 cities nationwide, including nearly every suburb and rural area.

ONCE-REDLINED AREAS ARE NO LONGER A PROXY FOR BLACK AMERICA

Redlining was a federally created—but locally implemented—form of discrimination. As such, redlined areas, and the cities in which they are located, vary widely in size, demographics, and location. Moreover, the racial makeup of the population in redlined areas has grown and evolved dramatically over the last eight decades, and the effects of the practice have spread beyond the confines of the original maps.

The practice of redlining was explicit in its targeting of Black Americans. While Latino or Hispanic residents, low-income white residents, noncitizens, communists, and other populations the federal government deemed “risky” were often included in redlining, they were not targeted in the same manner as Black residents. Today, neighborhoods that fall within once-redlined areas are more likely to have a higher concentration of Black residents, as well as lower incomes, lower home values, and other negative economic characteristics relative to the rest of their cities.

However, proposals that base their remedies primarily on formerly redlined areas paradoxically do not redress the main racial group that was explicitly targeted, exclude important Black neighborhoods and communities, and would skew impact toward a handful of large cities. Place-based discrimination—the practice of divesting in neighborhoods wholesale on the basis of race—has had adverse effects on both people and place. Policymakers should be intentional in ensuring that their proposed solutions can address both.

Consequently, redlining—the master’s tool—will prove to be insufficient in dismantling the legacy of racial inequities in homeownership and wealth in the United States.

METHODS

We define formerly redlined areas as those geographies marked “Hazardous” or “Fourth Grade” and thus outlined in red via the University of Richmond’s Mapping Inequality project. We define cities as census “Places” and choose principal cities as our unit of comparison, rather than metropolitan areas, to better account for the general centrality of redlined areas around urban cores. Principal cities are defined by the U.S. Census Bureau. Population totals and characteristics are tabulated by aggregating all census block groups whose population-weighted centroids fall within any redlined area (including those areas outside of contemporary principal city limits), estimating aggregated medians and margins of error by linear interpolation. Block groups are the smallest geography for which the American Community Survey provides estimates for the latest dissemination period (2017). However, not all socio-economic characteristics which are available in the ACS at the census tract level are available for block groups. Block groups offer a finer approximation of the irregular geographies of redlined areas, at the expense of accessing fewer ACS estimates. As this analysis is based largely on demographic totals, which are available at the block group level, we choose to make the best possible geographic approximation instead of a broader socio-economic snapshot. Because we examine whether the complicated boundaries of these geographies should be followed closely today, we therefore deem it necessary to estimate the most accurate interpretation of those boundaries possible. At time of writing, 2010 population totals for census blocks are available (and would provide a finer resolution of irregular redlining geographies than block groups), but these figures are nine years old and do not include any socio-economic characteristics. After the 2020 census, block level population data will allow for finer demographic analysis of redlined areas using up-to-date figures. All margins of error and significance tests are calculated at a 90% confidence interval.

17VIEW GALLERYLocation: Irvington, N.Y.Price: $4.5 millionSize: 11,653 square feet, 8 bedrooms, 10 full and 2 half bathrooms

Though it barely qualifies as what most financial mortals might consider downsizing, Hollywood veterans Michael Douglas and Catherine Zeta-Jones have slightly reduced their considerable residential footprint in New York State’s fancy-pants Bedford. Selling a more than 15,000 sq. ft. Bedford Corners mansion for almost $20.5 million and concurrently snapping up a not quite 12,000 sq. ft. Gatsby-esque manor house about 20 miles away, in Irvington, for exactly $4.5 million.

Douglas and Zeta-Jones bought the more than 13-acre Bedford Corners spread about five years ago for $11.25 million. They sold it in what appears to have been a clandestine, off-market deal to a mysterious corporate entity. It links back to the impossibly posh Sherry Netherland building on Manhattan’s Fifth Avenue. Situated in the coveted Guard Hill area, the palatial estate is anchored by a stately 26-room residence that dates to the late 1800s. At the time of their purchase, it offered eight bedrooms and 18 bathrooms plus an extensive spa facility with not just one but two indoor swimming pools, check this if you’re interested in a Custom Pool Resurfacing. The property additionally included a two-unit cottage for guests or staff, a car brought from buy here pay here near me, collector’s garage and a full array of equestrian facilities.

The lavish living couple’s only somewhat smaller but far less expensive new digs, dubbed Long Meadow, meanders over 12 bucolic and largely wooded acres that roll down to the Hudson River. Just 25 miles outside Manhattan and built in the early 1930s, the 22-room stone-accented red brick Georgian mansion sits at the head of a long, gated driveway with eight bedrooms and 10 full and two half bathrooms. Listing details disclose the baronial three-story behemoth also has a total of seven fireplaces, an 11-zone heating and cooling system, a four-car garage and annual taxes that top $150,000.

An elegant columned portico leads to gracefully proportioned and intricately detailed living spaces that include a formal and living and dining rooms, both with an antique limestone fireplace and the latter sporting candy apple red lacquered walls that reflect light tossed off from a delicate crystal chandelier. There’s also double-height wood-paneled library flooded with natural light through massive arched windows, a casual lounge with wet bar and a fully updated center island kitchen with commercial-grade appliances and marble countertops. A stone-floored loggia opens to a massive stone-paved terrace that is partly shaded by a black and white striped awning and offers a stunning tree-framed view across the Hudson River, while the mansion’s eight bedrooms include a two-bedroom guest suite and a spacious owners suite that comprises a large bedroom and separate sitting room, a dressing room and a glitzy bathroom with a jetted tub next to a white marble fireplace.

The mansion’s lowest level opens the estate’s rolling grounds and contains an indoor swimming pool, fitness room, recreation/games lounge and, outside, a summer kitchen. Marketing materials indicate the estate offers “enormous untapped potential” to add an outdoor swimming pool and cabana, tennis court and guest cottage. As noted by The Hudson Independent, Houlihan Lawrence Realtors had both sides of the deal.

The Douglas-Zeta-Joneses have long and famously presided over an international portfolio of luxury homes that have made them regular fodder for property gossip columns around the globe. In addition to a sprawling co-operative apartment in a prestigious apartment house overlooking Central Park on New York City’s Central Park West and a large house in Zeta-Jones’ hometown of Swansea, Wales, the couple have long owned a walled compound in Bermuda that came up for sale earlier this year at $19 million but is no longer listed on the open market, although it’s unclear if it’s been sold. The couple’s 10-bedroom compound on the Spanish island of Majorca, which is co-owned by Douglas’s ex-wife Diandra Douglas, was also set out for sale earlier this year and is still available at a whopping $32.5 million.