The million-dollar home is no longer such a rare species.

The number of U.S. homes valued at $1 million or more increased by 400,702 this year, the largest annual rise since the housing price recovery began in 2012, according to a new study by real estate research firm Trulia. Slightly more than 3 million homes nationally, or 3.6% of the total, are worth at least $1 million, up from 3.1 percent last year and 1.5 percent in 2012.

Not surprisingly, many of the freshly minted million-dollar units are in California, which already boasts the most in the country. The San Jose and San Francisco metro areas have the largest shares of $1 million homes and also notched the biggest increases over the past year.

Meanwhile, 29 cities and towns joined those with a median home value of $1 million or more this year, bringing the total to 201. Nineteen municipalities joined the million-dollar club last year.

They include San Jose, California, whose median value rose from $930,900 to $1.09 million; Fremont, California ($966,000 to $1.13 million); Burbank, California ($845,700 to $1.01 million); Newton, Massachusetts ($977,200 to $1.07 million); and Shelter Island, N.Y. ($903,500 to $1.15 million)

Trulia Senior Economist Cheryl Young attributed the big jump to widespread home price increases in recent years, with the median national home price climbing 7.6 percent the past year to $220,100. The median, or midpoint, of all home prices is up 45.3 percent since 2012. Housing demand has been strong while supplies are low, driving values higher.

“Home values have been escalating… And at about $1 million, there’s even greater appreciation,” she says.

Of the roughly 15,100 larger neighborhoods around the country analyzed by Trulia, 838 have median Neighborhood Values of $1 million or more and about two thirds of those are in California. Nearly 30 percent of California’s neighborhoods have a median home price of at least $1 million, the most by far of any state. New York, Florida and Washington followed.

The 10 metro areas that posted the largest increases in share of $1 million homes the past year:

San Jose, California

Share of million-dollar homes, October 2017: 55.7 percent

Share, October 2018: 70 percent

San Francisco

Share of million-dollar homes, October 2017: 67.3 percent

Share, October 2018: 81 percent

Oakland, California

Share of million-dollar homes, October 2017: 24.9 percent

Share, October 2018: 30.7 percent

Honolulu

Share of million-dollar homes, October 2017: 16.2 percent

Share, October 2018: 19.8 percent

Orange County, California

Share of million-dollar homes, October 2017: 17.2 percent

Share, October 2018: 20.2 percent

Los Angeles

Share of million-dollar homes, October 2017: 17.5 percent

Share, October 2018: 19.6 percent

San Diego

Share of million-dollar homes, October 2017: 11.8 percent

Share, October 2018: 13.8 percent

Seattle

Share of million-dollar homes, October 2017: 11.4 percent

Share, October 2018: 13.3 percent

Ventura County, California

Share of million-dollar homes, October 2017: 8.9 percent

Share, October 2018: 10.5 percent

Long Island, N.Y.

Share of million-dollar homes, October 2017: 8.8 percent

Seattle is known for its hip neighborhoods, soaring home prices, and being home to Amazon.com Inc., the world’s most valuable company. So why is its rental housing market experiencing the most severe slowdown in the U.S.?

Seattle-area median rents didn’t budge in July, after a 5 percent annual increase a year earlier and 10 percent the year before, according to Zillow data on apartments, houses and condos. While that’s the biggest decline among the top 50 largest metropolitan areas, it’s part of a national trend. Rents in Nashville and Portland, Oregon, have actually started falling. In the U.S., rents were up just 0.5 percent in July, the smallest gain for any month since 2012.

“This is something that we first started to see two years ago in New York and D.C.,” Aaron Terrazas, a senior economist at Zillow, said in a phone interview. “A year ago, it was San Francisco and most recently, Seattle and Portland. It’s spreading through what once were the fastest growing rental markets.”

Tenants are gaining the upper hand in urban centers across the U.S. as new amenity-rich apartment buildings, constructed in response to big rent gains in previous years, are forced to fight for customers. Rents are softening most on the high end and within city limits, Terrazas said. Landlords also have been losing customers to homeownership as millennials strike out on their own, often moving to more affordable suburbs.

Boom to Bust – Rents go from double-digit gains to declines in four years

Realtor Roy Powell last month was helping his clients, two women in their mid-20s find an apartment in Seattle. They looked at seven places and narrowed it down to two — a five-story building with a rooftop dog park and an air-conditioned gym, and a newly remodeled seven-story tower that won their business by throwing in a year of free underground parking, normally $175 a month.

Even condo owners with just one or two units to rent are offering concessions to compete with new buildings, Powell said. “A lot of them are going from absolutely no pets to allowing pets. That’s a big deal in Seattle, where everybody has a dog or cat.”

‘Tremendous Competition’

Batik, a new 195-unit Seattle apartment building, has views of the downtown skyline and Mount Rainier, a giant rooftop deck with a garden where tenants can grow fruits and vegetables, a community barbecue and an off-leash pet area. New tenants can receive Visa gift cards worth as much as $6,000, with half paid at signing and the rest a month later.

“There is tremendous competition for tenants,” said Lori Mason Curran, spokeswoman for landlord Vulcan Real Estate, Microsoft co-founder Paul Allen’s company, which launched Batik in March. “Over time, we think long-term demand is solid. But there is so much supply tamping down rent growth right now.”

In Seattle, another factor contributed to the glut of rentals. While the city is in the midst of a building boom — with more cranes dotting the skyline than any other in the U.S. — much of the residential multifamily construction has been apartments. Developers have shied away from condos because of state laws that allow buyers to more easily sue if there are defects in the construction.

Booming Construction

U.S. multifamily apartment construction for the past few years have been at levels not seen since the 1980s and rapid rent gains have also encouraged owners of single-family homes and condos to fill them with tenants. Projects opening now were conceived by developers a few years ago when rent gains in the U.S. were peaking at an annual gain of 6.6 percent, according to Zillow data.

The most expensive markets slowed first as new supply became available and tenants struggled to afford rapidly-rising lease rates. Rents in the San Francisco area jumped 19 percent in the year through July 2015. Now, they have been flat since last July. New York rents, which were up 7 percent in 2015, have been decelerating for a couple years, declining 0.4 percent in July.

For the first time since 2010, it’s now easier to build wealth over an eight-year period by renting a home and investing in stocks and bonds, rather than by buying and accumulating equity, according to a national rent-versus-buy index of 23 cities produced by Florida Atlantic University and Florida International University faculty. That’s because home prices are high and rising mortgage rates are adding to the cost of homeownership.

That could be bad for sellers, especially in markets like Dallas and Denver, where renting is now so much more favorable than buying, according to Ken Johnson, a real estate economist at Florida Atlantic University, a co-creator of the Beracha, Hardin & Johnson Buy vs. Rent Index.

Reminiscent of the Bubble

Already, housing markets in strong economies are cooling, in part because incomes haven’t kept pace with rising prices and borrowing costs. Dallas and Denver have reached so far into favorable rental territory that they look like Miami right before it crashed in the last decade, Johnson said.

The difference now is that neither market is experiencing the kind of speculation and risky lending that inflated the last housing bubble, he said.

“What’s interesting is that cities that suffered the least in 2007 and 2008 — Dallas and Denver — now are experiencing the most exposure to risk,” Johnson said.

The slowdown in the rental market coincides with a rise in homeownership among millennials, which jumped to 36.5 percent in the second quarter from 35.3 percent a year earlier.

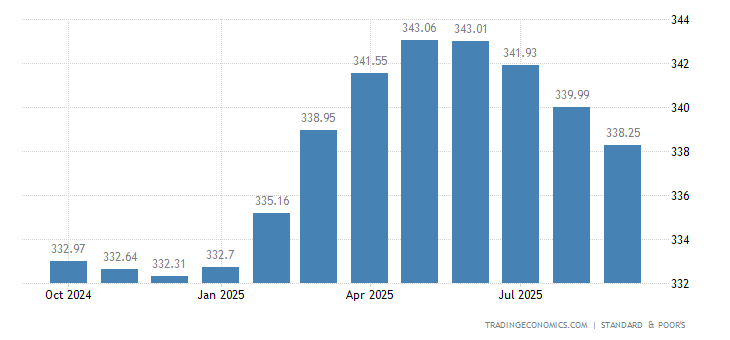

The S&P CoreLogic Case-Shiller 20-City Composite Home Price Index in the US rose 6.8 percent year-on-year in February 2018, following a 6.4 percent advance in January and easily beating market expectations of a 6.3 percent gain. It was the steepest increase in house prices since an 8.1 percent climb in June 2014, with Seattle (12.7 percent), Las Vegas (11.6 percent) and San Francisco (10.1 percent) reporting the sharpest gains among the 20 cities. Meanwhile, the national index, covering all nine US census divisions rose 6.3 percent, up from 6.1 percent in the previous month. Case Shiller Home Price Index in the United States averaged 160.67 Index Points from 2000 until 2018, reaching an all time high of 206.67 Index Points in February of 2018 and a record low of 100 Index Points in January of 2000.

The average rate you’ll pay for a 30-year fixed mortgage is 4.33 percent, an increase of 2 basis points over the last week. A month ago, the average rate on a 30-year fixed mortgage was lower, at 4.31 percent.

At the current average rate, you’ll pay a combined $496.63 per month in principal and interest for every $100,000 you borrow. That’s $1.17 higher compared with last week.

You can use Bankrate’s mortgage calculator to estimate your monthly payments and find out how much you’ll save by adding extra payments. It will also help you calculate how much interest you’ll pay over the life of the loan.

15-year fixed mortgages

The average 15-year fixed-mortgage rate is 3.76 percent, up 3 basis points over the last seven days.

Monthly payments on a 15-year fixed mortgage at that rate will cost around $728 per $100,000 borrowed. The bigger payment may be a little harder to find room for in your monthly budget than a 30-year mortgage payment would, but it comes with some big advantages: You’ll save thousands of dollars over the life of the loan in total interest paid and build equity much more rapidly.

5/1 ARMs

The average rate on a 5/1 ARM is 4.11 percent, sliding 10 basis points over the last 7 days.

These types of loans are best for those who expect to sell or refinance before the first or second adjustment. Rates could be substantially higher when the loan first adjusts, and thereafter.

Monthly payments on a 5/1 ARM at 4.11 percent would cost about $484 for each $100,000 borrowed over the initial five years, but could increase by hundreds of dollars afterward, depending on the loan’s terms.

Where rates are headed

To see where Bankrate’s panel of experts expect rates to go from here, check out our Rate Trend Index.

Methodology: The rates you see above are Bankrate.com Site Averages. These calculations are run after the close of the previous business day and include rates and/or yields we have collected that day for a specific banking product. Bankrate.com site averages tend to be volatile — they help consumers see the movement of rates day to day. The institutions included in the “Bankrate.com Site Average” tables will be different from one day to the next, depending on which institutions’ rates we gather on a particular day for presentation on the site.

According to the Census Bureau’s Housing Vacancy Survey (HVS), the U.S. homeownership rate is at 63.9% in the third quarter 2017, which is statistically unchanged from its last quarter reading of 63.7%. The rate of homeownership is on an upward trend after dropping to a cycle low of 62.9% in the second quarter 2016. Compared to the peak of 69.2% in 2004, the homeownership rate is below by 5.3% and remains below the 25-year average rate of 66.3%.

Younger homebuyers are gradually entering the housing market after the Recession. Compared to a year ago, the homeownership rates among households ages 35-44 increased from 58.4% to 59.3%. Millennials also registered noticeable gains – from 35.2% to 35.6%. Older households, ages 65 and over, is the only group where homeownership rates showed a slight decline of 0.1%.

The nonseasonally adjusted homeowner vacancy rate remained low at 1.6% in the third quarter 2017, down by 0.2% from previous year and statistically not different from the rate in the second quarter. At the same time, the national rental vacancy rate increased to 7.5%, compared to only 6.9% a year ago.

The HVS also provides a timely measure of household formations – the key driver of housing demand. Although it is not perfectly consistent with other Census Bureau surveys (Current Population Survey’s March ASEC, American Community Survey, and Decennial Census), the HVS remains a useful source of relatively real-time data.

The housing stock-based HVS revealed that the number of households increased to 119.1 million during the third quarter of 2017. This is 0.4 million higher than a year ago and sustains gains recorded in 2016. Growth in household formations will spur rental housing demand first, and ultimately, home sales. Indeed, the number of homeowner households rose by 0.8 million, after experiencing a large gain of 1.3 million in the second quarter.

An efficient HVAC system can you save you loads of money in the long run and keep your home nice and comfortable throughout the year. Problems in the ductwork, however, can quickly consume your energy budget and make it hard to heat and cool certain areas of the home. If you suspect your HVAC system is not working properly and needs hvac repair, follow this short guide to help identify and fix common ductwork problems. The problem with these repairs is that usually the people who repair the ducts are not painters. To do this kind of work you have to drill holes in the walls and damage the whole design. If you are doing this or any other work you can trust your design to interior painting mckinneythey will take care of leaving it even better than before.

Abnormal Energy Bills

That’s why it’s important to call the skilled and highly qualified HVACprofessionals in Cook County when you need air conditioning repair service near Texas so don’t allow yourself or your family to go through another scorching hot day and night, get your Central A/C or Window Unit repaired today! A sudden spike in your energy bill is a good sign that your home’s HVAC system is compromised. You can go to this web-site for more about the HVAC installation.

Leaky connectors and poor designs lead to air flow loss, which makes the system work harder to heat and cool the home. This in turn expends more energy and runs up the electricity bill. Take a look at this device is a lifesaver this summer if you suffer form the heat.

Noisy Ductwork

Another good indication of a bad HVAC system is noisy ductwork. In rectangular ducting, these noises are usually the result of the metal expanding and contracting. It should be noted that noises are typical when the system first turns on or off. Make sure to change air filters frequently and keep air ducts and registers clean to avoid damages. You should be concerned, however, if the noises continue while the system is running. If you hear a whistling sound, for example, you are likely dealing with vent covers that are too small for the system. If you need financing for your ac repairs in Las Vegas, check out Air Pro Master.

Uneven Temperatures

If you have areas of the home that are hard to heat and cool or get overly stuffy, your HVAC system probably has a leak or two. Uneven temperatures are caused by poor air flow because the system is simply losing too much air to properly do its job. In extreme cases, you will not be able to heat or cool certain areas of the home even if the thermostat is turned to its highest setting. It is essential to get a new heating system installed in your home or get the old one serviced as it will increase its performance and efficiency.

Finding Problem Areas

Detecting problems in the ducting is a straightforward process. The biggest issues typically include bad seals around joints, improperly seated vents, and poorly supported ducts. You might also examine the overall design of the ductwork as the installer may have made mistakes in the original installation. Look for areas that feature sharp turns in the ducting as this can significantly reduce air flow.

Feeling

You can also feel for air loss with your hands. Start by feeling the air pressure coming out of vents in multiple rooms after the ac installation services are done at your place. If you detect a difference between vents, then you know you have a leak somewhere in line with that vent. You can narrow down the location of the leak by using some incense, toilet paper, or wet fingertips. The incense and toilet paper will move or your fingers will get cold when coming in contact with the leak.

That’s why it’s very important that you use a local, professional, and highly skilled HVAC technician in Plant City for your Air Conditioning Repairs. Hiring an unlicensed handyman may seem cheap up front, but it could have deadly consequences. When you need it done properly, Call an expert

Do you know what is two-stage cooling AC technology and how to get it? Visit this company’s website for more information about maintaining your air conditioning.

Visual Examination

Examine the ducting for any obvious signs of gaps, holes, and cracks. The most likely problem areas include connections and seams, and places where the ducting links up with the ceiling, floor, registers, and vents. For flexible ducting, ensure the pieces are not crimped or tangled.

Fixing Ductwork Leaks

Once you locate the problem area, it’s time for a little repair. All you need to repair leaky ductwork is some HVAC-grade aluminum foil, a putty knife, gloves, and a few cloths. Begin by cleaning the area with a damp cloth and keep a lookout for any sharp edges. It’s recommended to use mastic for loose fittings, though foil tape can also prevent air loss. Just make sure the connection is tightened up and the screws are back in place before you apply tape. If you detect any major cracks in the ducting, you may need to replace the section with a new piece of sheet metal. Contact an HVAC company and see what heating Services they offer.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the average 30-year fixed mortgage rate ticking up to its highest mark in six weeks.

News Facts

30-year fixed-rate mortgage (FRM) averaged 3.85 percent with an average 0.5 point for the week ending October 5, 2017, up from last week when it averaged 3.83 percent. A year ago at this time, the 30-year FRM averaged 3.42 percent.

15-year FRM this week averaged 3.15 percent with an average 0.5 point, up from last week when it averaged 3.13 percent. A year ago at this time, the 15-year FRM averaged 2.72 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.18 percent this week with an average 0.4 point, down from last week when it averaged 3.20 percent. A year ago at this time, the 5-year ARM averaged 2.80 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Quote Attributed to Sean Becketti, chief economist, Freddie Mac. “After holding steady last week, rates ticked up this week. The 10-year Treasury yield rose 8 basis points, while the 30-year mortgage rate increased 2 basis points to 3.85 percent.”

Find your way to The Market on Spring for fresh foodie fare in a quaint setting.

PHOTOS COURTESY MARKET ON SPRING

Most Northern Westchesterites who drive Route 35 are on a mission — to get from one town to another in a hurry, to make a train, or to pick up their kids. But, there’s a charming spot just minutes off this busy thoroughfare that’s certainly worth the detour.

The Market on Spring is at the center of the tiny but lovely hamlet of South Salem. Antiques, a riding academy, a tack shop, and cozy tavern are just about all you’ll find here, but that’s what makes it so wonderful. The small market is the perfect fit, renovated last year in a mix of natural wood and rustic metal, and serving carefully sourced, high-quality fare for breakfast and lunch. Though tucked away, the shop is attracting a steady stream of customers, explains manager and Vista native Bryce O’Brien. “People tell us they’ve lived in the area for years and have never made the turn onto Spring Street, never knew ‘anything was here,’ but now they’ve found us.”

Maybe word is getting out about the delicious sandwiches made from New York State grass-fed beef, or cage- and hormone-free turkey (all roasted in-house by Market’s chefs), with condiments such as chipotle remoulade, onion jam, and honey mustard aioli. The organic egg breakfast sandwiches (options include house-cured salmon and homemade chorizo) are also gaining a dedicated following. O’Brien says the shop’s country industrial decor and elevated deli menu are especially appealing to city folk who weekend at homes on nearby Lake Truesdale. Well, we suburbanites know a good thing when we see it, too!

Sales of newly constructed homes stumbled in April, as builders retreated after a March surge that marked the strongest selling pace in a decade.

New-home sales ran at a seasonally adjusted annual rate of 569,000, the Commerce Department said Tuesday. That was well below the MarketWatch consensus forecast of a 610,000 annual rate, but was offset by sharp upward revisions to data from prior months.

In particular, March’s pace was raised to a pace of 642,000, the highest since October 2007.

April’s figures were 11.4% lower for the month, but 0.5% higher than in the same period a year ago.

The government’s new-home sales data are based on small samples and are often heavily revised. Total sales in the first four months of the year are 11% higher compared with the same period a year ago.

In April, the median sales price for a new home was $309,200, down from $318,700 in March and $321,300 in the year-ago period. As the pace of selling decelerated, there were 5.7 months’ worth of homes available, up from 4.9 months in March. A market with a healthy balance between supply and demand typically has about 6 months’ worth of inventory.

One factor worth noting, April was one of the rainiest months in decades, and that may have helped dent sales. Ralph McLaughlin, Trulia chief economist, said while he wasn’t worried about data from one month, builders still have a way to go before residential construction normalizes.

“If we compare the share of new home sales to total sales, that share needs to more than double,” McLaughlin wrote in a Tuesday note. New-home sales made up nearly 12% of total sales, about half the historical average, he said.

The 12-month rolling total of sales rose to 88.3% of their 50-year average, McLaughlin added.

One of President Trump’s common refrains on the campaign trail was that he would help rebuild the country’s crumbling infrastructure, leaning on his extensive experience in real estate and development to shepherd forth a plan to cut red tape, move projects forward, and put this country to work.

More than 100 days into his administration, his grand design has yet to take shape, though it’s been a constant source of conversation in D.C. There has been movement over the last few days, with reports saying that the Trump team has solicited bids for potential infrastructure investments from across the country and looks toward releasing a plan in the fall that would steer $200 billion of public money to infrastructure investment.

Curbed spoke to infrastructure experts to get their take on Trump’s nascent plans: what should be included, what to watch for as plans come together, and its chances to clear both houses of Congress and help America get to work.

Watch the numbers

Henry Petroski, a Duke professor and infrastructure expert, says that spending on roads and construction is “like apple pie and motherhood—everybody’s for it.” There’s a lot of talk about some kind of plan, a proposal both candidates supported last year, and representatives and senators will have a tough time voting against it, Petroski says. It’s still taking shape, but based on previous reports and statements from Trump administration officials, it would include a combination of government investment, new funding mechanisms to encourage private investment, and regulatory reform to help accelerate approvals and construction timelines.

That makes it all the more important to watch how funding is allocated. The trillion-dollar proposal the Trump administration is developing sounds like a lot, and it is: The federal government’s annual budget is about $3.8 trillion, including entitlements such as Social Security and Medicaid. Petroski believes the spending will most likely be spread out over 10 years, which means a 100 billion dollars annually, roughly double the amount currently being spent on roads and bridges. Doubling funding is a big deal, but it’s important to put things in perspective.

“We can’t just look at the headlines that say $1 trillion; we need the details,” he says. “This isn’t just an issue with this administration, however. This happens with every administration.”

Caiaimage/Getty Images

Will states take the lead?

While the Trump administration has promised to have a plan together by this fall, some analysts, such as Petroski, are skeptical. He feels that health care and other priorities may derail infrastructure this year, at least on the federal level.

Federal delays in approving new spending, however, have spurred many cities and states to take action. Federal infrastructure is tagged to the gasoline tax, which hasn’t been raised since 1993 (Trump has flirtedwith the idea of raising it to fund infrastructure spending). But many states have raised their own rates or passed spending measure to fund infrastructure (federal dollars are, on average, only responsible for 25 percent of infrastructure spending, according to Petroski).

“Close to half the states have raised the state gasoline taxes in the last couple of years, and the others are considering it,” he says. “They simply can’t wait for the federal government to do something.”

Will we build green infrastructure?

In addition to how much we’re going to spend on infrastructure, another big question is what we’re going to spend money on. Armando Carbonell, a senior fellow and urban policy expert at the Lincoln Institute, says one of the biggest problems with any Trump infrastructure plan is the administration’s stance on climate change. It’s not just that any potential new construction may ignore public transit and sustainable options that reduce carbon emissions, it’s that not acknowledging a changing climate means money will be misspent.

“We need infrastructure to protect communities from the effects of climate change that can’t be avoided,” he says. “Sea-level rise, flooding, the effects of wildfires; in many cases, there are infrastructure needs that should be a priority, such as protecting coastal cities. If we don’t take climate change into account, we may well build infrastructure that is vulnerable. There are simple things we can do, such as building on higher elevations, that take account of a rising sea level. If we don’t do that, any investment might be a bad one.”

One of Trump’s promises has been that by creating a new regulatory system, reforming current processes, and encouraging public-private investments (or P3s) he can cut red tape and move long-stalled projects forward. Like other aspects of an infrastructure overhaul taking shape, the devil is in the details.

Carbonell says proper oversight and regulatory update could give the sector a massive upgrade, saving time and money. There are “great benefits” to looking at what and how we do things, especially the procurement and finance processes.

“I don’t have a black or white view of P3s, other than to say people need to be careful and look out for the public interest,” says Carbonell. “With proper regulations and design, P3s may be part of the solution. But we can’t get something for nothing. If we want a trillion-dollar investment in infrastructure, we need to spend a trillion dollars.”

Others have a more pessimistic view of pushing for more private investment in infrastructure. According to urbanist and journalist Yonah Freemark, the push for privatization in infrastructure investment is consistent with Trump’s rhetoric—Secretary of Transportation Elaine Chao has been open to finding new private funding sources for infrastructure, and the proposed Trump budget does make massive cuts in public transportation spending—but will also significantly shape the way any new infrastructure policy works.

“One thing we know is that there’s no way private-sector entities would be involved with an infrastructure project unless it involves user fees or ways to make revenue,” he says. “That makes sense; why would you invest in a project that couldn’t make money? But that changes the decision-making process. It’s the perspective of a profit-making private company, not the public sector.”

That translates into support for moneymaking projects, such as pipelines, toll bridges, and toll roads, not, say, water pipes, or roadways in less dense rural areas, according to Freemark.

Shutterstock

What kind of jobs will it provide?

Trump has also promoted infrastructure as a jobs program to help with unemployment. According to Scott Myers-Lipton, a professor of sociology at San Jose State University and author of Rebuild America: Solving the Economic Crisis through Civic Works and Social Solutions to Poverty, it’s tough to “square the circle” when it comes to providing high-wage jobs while cutting regulations (and potentially, labor protections) and encouraging private investment.

He sees New Deal-era social works programs, which provided direct employment through the government, as a much more effective means of creating a large-scale jobs program and truly putting America back to work.

“How is it going to help people earn stable incomes?” he says. ”So far, he has not yet put forward a plan that, in that Rooseveltian sense, meets the goal of getting living wage jobs to as many people as possible. This was one of his big promises, spend big on infrastructure and drive unemployment down.”

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8509393/GettyImages_164852858.jpg)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8509399/GettyImages_170411738.jpg)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8509429/shutterstock_637266973.jpg)