Each year, leading economists look into their “crystal balls” in an attempt to foresee what the New Year holds for the construction industry. For 2018, this proved a tougher task given key uncertainties clouding the outlook at year end, including the incomplete 2018 federal spending package and as yet enacted tax reform legislation (just passed at time of publication). Add in storm and wildfire recovery boosting construction demand, costs and labor woes (further compounded by immigration reform), then throw in the pending mid-term elections, and the future is cloudier still.

That said, economists gave their best shot, and here is a Q&A covering their outlook for the overall U.S. economy and general construction as we neared the close of 2017. Next month, industry experts will take a targeted look at the prospects for the transportation sector.

Overall Economic Outlook

What level of U.S. economic growth do you see for 2018? What are some key drivers that will impact growth either positively or negatively?

Robert Dietz, senior vice president and chief economist, National Association of Home Builders (NAHB): NAHB sees continued modest yet positive growth prospects for 2018. We should continue to grow, but at below 3% rates. Wage growth is increasing, which is good for consumer spending and housing demand, but is a concern for employers. The wild card for 2018 and 2019 is tax reform. Smart tax reform that rewards small business and promotes housing will contribute to growth. Tax reform that increases taxes on homeowners to reward investors, including foreign owners of U.S. assets, will be counterproductive.

The tight labor market is a key limiting factor for overall economic growth. Increases for the labor force participation rate will help labor markets to continue to grow. However, absent those improvements, wage pressure could increase inflation and cause the Fed to move somewhat faster than its current gradual pace of interest rate hikes.

Ed Sullivan, chief economist, Portland Cement Association (PCA): We project GDP growth to be at 2.3% in 2018. We came off the worst recession since the Great Depression and there has been a tremendous pent-up demand. It takes time to fill this demand, and our growth has been slow.

It will likely continue to be slow driven in part by millennials who are in debt, who are taking their time to start families and who currently don’t participate in the housing market. The recession also changed peoples’ behaviors. But people forget and eventually they will return to old spending habits, just as millennials will one day start families and buy homes.

Ken Simonson, chief economist, Associated General Contractors of America (AGC): The economy should keep expanding at a moderate 2% to 2.5% rate, after inflation. However, this could be affected by big changes in tax and spending policy or by an international crisis.

Anirban Basu, chief economist, Associated Builders & Contractors (ABC): As we enter 2018, consumer confidence is at a roughly 17-year high, unemployment is at a 17-year low, financial markets are surging, the global economy is improving and leading indicators suggest plentiful momentum during the year’s early months. It has been many years since the U.S. economy entered the New Year with such momentum.

Consumer spending will continue to be the leading engine of growth. But that will be supported by faster export growth as the world economy continues to heal, and by faster business spending growth, particularly if pending corporate tax cut legislation is passed. In short, the economic outlook for the U.S. in 2018 is quite good.

There are abundant risks, however. One could argue that asset prices rose too fast and furiously in 2017. That could set the stage for significant asset price volatility in 2018. Stock and other prices can’t rise forever. This is particularly true given rising inflationary pressures, whether in the form of wages, tuition, rent, medical care or fuel. Should interest rates rise with unanticipated rapidity due to these emerging pressures, elevated asset prices could become jeopardized, setting the stage for negative wealth effects. This means that while 2018 should be strong for the U.S. economy, there are few guarantees with respect to 2019 or 2020.

Building Construction

How strong was construction in the commercial and housing markets in 2017, and what level of growth do you expect to see in both segments for 2018?

AGC: Single-family construction spending increased 9% through the first 10 months of 2017, about the same growth rate as in 2016. But multifamily construction really hit the brakes, slipping to a 4% growth. I think that in 2018, there will be a lot of rebuilding and renovations in areas of Texas, Florida and California devastated by hurricanes, flooding and wildfires. Meanwhile, multifamily building may dip after six years of generally torrid growth.

ABC: There was a considerable volume of building construction in 2017. Leading segments included hotel, casino, office, distribution center and multifamily construction. There are many forces at work, including Millennial demographics, the e-commerce revolution, foreign investment into commercial real estate and growth both in consumer and business travel. One suspects that this momentum will stretch into 2018 since both domestic and foreign capital is on the hunt for investment opportunities that yield income.

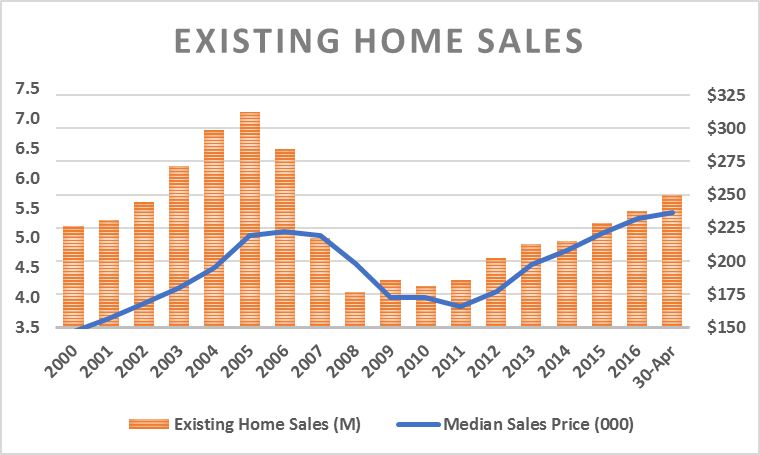

NAHB: On the demand side of the housing market, incoming household formation data show strength for the for-sale market and some softening for rental markets. These trends are consistent with demographic data that show a growing number of millennials entering their 30s. This process will continue to sustain demand for single-family homes in the years ahead.

Single-family construction should continue along its modest growth trend (7%), while still being constrained by supply-side bottlenecks, including lack of labor and rising building material prices. Nonetheless, builder confidence, as measured by the NAHB/Wells Fargo Housing Market Index, remains solid. Remodeling should also post gains given rising homeowner wealth and reduced homeowner mobility, which will increase the need for aging-in-place and other kinds of structural improvements.

Multifamily starts peaked in 2015, and NAHB expects a leveling off process to continue over the next few years. The decline in apartment starts in 2017 was steeper than expected, with a 10% 2017 decline expected. We forecast smaller but still negative growth rates over the near-term as rental vacancy rates increase, rent growth softens and housing demand momentum moves to the for-sale market segment.

PCA: We anticipate modest growth throughout the building construction market in both the nonresidential and residential sectors. That should translate into a growth rate similar to 2017.

Nonresidential is approaching a peak and there is slowing in sectors like industrial that are impacted by the macroeconomic environment. The single-family residential market should be fairly healthy in 2018. Gains, however, will be slowed by difficult application processes, lack of Millennial participation and modest increases in mortgage rates that will impact affordability. The multifamily market still has strong potential, but it too is reaching its cyclical peak. Like 2017, next year will likely see 350,000 units built.

The big surprise is the improvement and repair sector thanks unfortunately to two serious hurricanes and California wildfires. This sector saw strong percentage gains toward the end of 2017 and will continue to see these gains throughout 2018.

Raw Material Costs

Do you expect to see the costs of raw materials such as asphalt, cement, steel and lumber increase in 2018? If so, to what level and what is driving the increases?

NAHB: We expect continued gains in building material prices, particularly for lumber given tariffs on Canadian softwood lumber. Rising building material prices was the issue that increased the most as a concern in 2017. While still below the lack of labor and lots, prices for drywall, roofing materials and other building components increased in 2017 due to hurricane repair efforts and the broader growth of the housing market. We expect this pressure on prices to continue in 2018.

ABC: The past year was associated with noteworthy increases in construction materials prices. After slumping for much of 2014 and virtually all of 2015, global commodity prices stabilized and then began to rise in 2016/17.

A more contentious view on trade, including with respect to Canadian soft lumber, also served to elevate price pressures. During a recent 12-month period, softwood lumber prices surged 15%. Diesel fuel, natural gas, iron and steel and other prices also expanded for much of 2017.

Given the expectation that the global economy will heat up even further in 2018, one would expect that materials prices will continue to rise. However, the rise in materials prices could be quite gradual. Quantity supplied is already responding to higher prices in many categories, which should translate into more gradual price increases in general.

AGC: Materials costs ended a years-long slide in late 2016 and rose at a moderate rate in most of 2017. Those increases are likely to accelerate a bit further in 2018 as global demand picks up and construction continues to grow, albeit slowly and unevenly. I don’t foresee a return to the severe, widespread escalations and occasional shortages that cropped up before the last recession.

Employment and Labor Costs

In recent years, finding skilled and experienced workers has challenged many construction companies. In fact, for many, it has been their No. 1 impediment to growth. Do you foresee companies continuing to struggle with this trend in 2018? What impact, if any, will the administration’s stand on immigration have on the industry and finding workers?

AGC: Finding capable workers will remain the leading challenge for contractors in 2018. The job market is continuing to tighten after more than seven years of continuous job gains and ever-increasing retirements of baby boomers. Restrictive immigration policies and stepped-up deportations are adding to the competition for workers and threaten to slow the growth in the overall economy as many industries struggle to fill openings or to replace the customers who are kept out of the country.

NAHB: On the supply side of the construction market, we need additional gains in the labor force participation rate to allow employers to continue filling open jobs. The construction industry is in the middle of a labor shortage and data suggest it will not turn the corner quickly. Without growth in the size of the labor force, it will be difficult for the residential construction industry to continue adding workers at the current pace of a little more than 100,000 per year. Higher wages due to a tight labor market will bring in some additional workers, but will also increase cost pressures on employers.

We could, of course, build and remodel more homes if we could add workers even faster. The demand is there. The industry must recruit the next generation of construction workers.

PCA: There is no easy fix to the labor challenge. Training programs for skilled workers are great, but they take time and we see companies struggling with labor for several years to come. The labor shortage will continue to be an impediment to company growth and immigration reform will only worsen the trend. Labor-saving technologies will alleviate some of this, but they can only go so far.

ABC: The lack of skilled workers is apparent throughout the U.S. economy, whether in construction, trucking, healthcare, hospitality, cybersecurity or a host of other industry segments…

The year 2018 will be yet another during which America’s low labor force participation rates will continue to hamstring businesses in many segments, including construction. A confluence of factors has led to these circumstances, including cultural shifts, shifts in educational philosophy, the atrophying of apprenticeship programs in much of the nation, and the ongoing large-scale retirement of many of the most talented, skilled and experienced construction workers. The nation’s shifting stand on immigration will not help, with employers finding it increasingly challenging to secure both skilled and semi-skilled personnel.

With respect to construction, the impact is to raise the cost of delivering construction services and to stretch out timetables. That makes it less likely that construction projects can move forward because this serves to reduce the predicted rate of return.

read more…

https://www.forconstructionpros.com/business/article/20985203/special-report-state-of-the-construction-industry-2018

Zillow

Zillow