The property tax rate in New York is high compared to the rest of the country. That’s according to a new report Wednesday from the financial news and opinion site 24/7 Wall St., which reviewed the effective rate — meaning the total amount of property taxes paid each year as a percentage of the total value of all occupied homes — for every state. The data is from the 2015 fiscal year and came from the conservative think tank Tax Foundation. If you want more information about seafarers tax deduction, click here.

New York’s effective property tax rate ranked 14th highest in the country, the report found, nestled between Iowa and Kansas. On average, state and local governments across the country bring in about $1,500 a year in property taxes per person. Here are the numbers for New York:

Effective property tax rate: 1.4 percent

Median home value: $314,500

Per capita property taxes: $2,696.90

Median household income: $64,894

If those numbers seem like too much, you might consider moving to Hawaii, where the effective property tax rate was just .29 percent. If that sounds like a dream, consider this — the median Hawaiian home is worth more than $617,000 and the typical household earns about $77,000 a year, so don’t forget to bring a checkbook and perhaps buy a lottery ticket upon arrival. Alabama, Louisiana, West Virginia and Wyoming rounded out the five states with the lowest property tax rates.

On the flip side, residents in the Northeast appear to pay the highest rates, with New Jersey, New Hampshire and Vermont all appearing in the top five. New Jerseyans pay more than anyone else in the country with an effective property tax rate of 2.16 percent, the authors found. Residents pay more than $3,000 per capita and the median household income is just over $80,000 a year. A typical home in the state costs about $335,000.

Here are the 10 states with the highest effective property tax rates:Subscribe

New Jersey

Illinois

New Hampshire

Wisconsin

Vermont

Texas

Nebraska

Connecticut

Ohio

Rhode Island

Property taxes are the single largest money-maker for local governments and they’re spent almost entirely on a local level. Generally they are used to fund fire, police, schools, roads, cleaning and repairs.

“As a result, the United States is a patchwork of property tax codes, and depending on where you live, property taxes can be either a trivial expense or a major financial burden,” the report said.

California home sales close year on downward trend as home prices post mild gains, C.A.R. reports

– Existing, single-family home sales totaled 372,260 in December on a seasonally adjusted annualized rate, down 2.4 percent from November and down 11.6 percent from December 2017.

– December’s statewide median home price was $557,600, down 0.5 percent from November and up 1.5 percent from December 2017.

– Statewide active listings rose for the ninth straight month, increasing 30.6 percent from the previous year.

– The statewide Unsold Inventory Index was 3.5 months in December, down from 3.7 months in November.

– For the year as a whole, sales were down 5.2 percent from 2017.

LOS ANGELES (Jan. 17) – California home sales declined for the eighth straight month in December, and a stagnating market for much of the year pushed sales lower in 2018 for the first time in four years, the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) said today.

Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 372,260 units in December, according to information collected by C.A.R. from more than 90 local REALTOR®associations and MLSs statewide. The statewide annualized sales figure represents what would be the total number of homes sold during 2018 if sales maintained the December pace throughout the year. It is adjusted to account for seasonal factors that typically influence home sales.

December’s sales figure was down 2.4 percent from the revised 381,400 level in November and down 11.6 percent from home sales in December 2017 of 420,960. December marked the fifth month in a row that sales were below 400,000 and the lowest level of sales sold since January 2015.

“The housing market continued to shift in December and drift downward as sales have fallen double digits for the past three out of four months,” said C.A.R. President Jared Martin. “This trend is expected to continue, as buyers remain cautious about the murky housing market outlook due primarily to the volatility in the financial markets and uncertainty in the economic and political arenas.

“Additionally, housing markets in and around the wildfire areas have been exhibiting unusual patterns that could remain unsettled for the next few months. The impact, however, is confined mostly within the region and should not have a noticeable effect in the housing market at the state level.”

The statewide median home price declined to $557,600 in December. The December statewide median price was up 0.5 percent from $554,760 in November and up 1.5 percent from a revised $549,550 in December 2017. The statewide median home price for the year as a whole was $570,010, up 6.0 percent from $537,860 in 2017.

“California’s housing market in 2018 was hindered by endlessly rising home prices and interest rate hikes, which combined to erode housing affordability and hamper home sales,” said C.A.R. Senior Vice President and Chief Economist Leslie Appleton-Young. “As a result, while the statewide median home price surpassed its previous peak and set a new record in 2018, annual home sales fell for the first time in four years to a preliminary 402,750 closed escrows in California, down from 2017’s pace of 424,890.

“In the coming months, we expect a brief hiccup in sales as the government shutdown temporarily delays closings due to interruptions in IRS income verification or the processing of HUD, VA and USDA loans,” said Appleton-Young.

Other key points from C.A.R.’s December 2018 resale housing report include:

On a regionwide, non-seasonally adjusted basis, sales dropped double-digits on a year-over-year basis in the San Francisco Bay Area, the Central Coast, Central Valley and Southern California regions, with the Central Coast dropping the most at 24.9 percent.

Thirty-nine of the 51 counties reported by C.A.R. posted a sales decline in December with an average year-over-year sales decline of 20 percent. Thirty-four counties recorded double-digit sales drops on an annual basis, and 10 counties experienced an increase in sales from a year ago.

Sales for the San Francisco Bay Area as a whole fell 17.5 percent from a year ago. Eight of nine Bay Area counties recorded annual sales declines of more than 10 percent. Only San Francisco County posted a year-over-year increase, gaining 11.3 percent from December 2017.

The Los Angeles Metro region posted a year-over-year sales drop of 17.8 percent, as home sales fell 16.3 percent in Los Angeles County and 18.3 percent in Orange County.

Home sales in the Inland Empire declined 19.8 percent from a year ago as Riverside and San Bernardino counties posted annual sales declines of 17.7 percent and 23.1 percent, respectively.

The median home price continued to increase in all regions, except in the San Francisco Bay Area. On a year-over-year basis, the Bay Area median price dipped 3.6 percent from December 2017. Home prices in Marin, San Francisco, San Mateo and Santa Clara counties continued to remain above $1 million, but both San Mateo County and Santa Clara counties recorded a year-over-year price decline.

Statewide active listings rose for the ninth consecutive month after nearly three straight years of declines, increasing 30.6 percent from the previous year. All major regions recorded an increase in active listings, with the Bay Area posting the highest increase at 65 percent, followed by Southern California (34 percent), Central Valley (24 percent) and the Central Coast (12 percent).

The Unsold Inventory Index, which is a ratio of inventory over sales, increased year-to-year from 2.5 months in December 2017 to 3.5 months in December 2018. The index measures the number of months it would take to sell the supply of homes on the market at the current sales rate.

The median number of days it took to sell a California single-family home rose from 25 days in December 2017 to 32 days in December 2018.

C.A.R.’s statewide sales price-to-list-price ratio* decreased from 98.7 percent in December 2017 to 97.4 percent in December 2018.

The average statewide price per square foot** for an existing, single-family home statewide edged up from $268 in December 2018 to $266 in December 2017.

The 30-year, fixed-mortgage interest rate averaged 4.64 percent in December, up from 3.95 percent in December 2017, according to Freddie Mac. The five-year, adjustable mortgage interest rate also increased in December to an average of 4.02 percent from 3.39 from December 2017.

Note: The County MLS median price and sales data in the tables are generated from a survey of more than 90 associations of REALTORS® throughout the state and represent statistics of existing single-family detached homes only. County sales data are not adjusted to account for seasonal factors that can influence home sales. Movements in sales prices should not be interpreted as changes in the cost of a standard home. The median price is where half sold for more and half sold for less; medians are more typical than average prices, which are skewed by a relatively small share of transactions at either the lower-end or the upper-end. Median prices can be influenced by changes in cost, as well as changes in the characteristics and the size of homes sold. The change in median prices should not be construed as actual price changes in specific homes.

*Sales-to-list-price ratio is an indicator that reflects the negotiation power of home buyers and home sellers under current market conditions. The ratio is calculated by dividing the final sales price of a property by its last list price and is expressed as a percentage. A sales-to-list ratio with 100 percent or above suggests that the property sold for more than the list price, and a ratio below 100 percent indicates that the price sold below the asking price.

**Price per square foot is a measure commonly used by real estate agents and brokers to determine how much a square foot of space a buyer will pay for a property. It is calculated as the sale price of the home divided by the number of finished square feet. C.A.R. currently tracks price-per-square foot statistics for 50 counties.

Leading the way…® in California real estate for more than 110 years, the CALIFORNIA ASSOCIATION OF REALTORS® (www.car.org) is one of the largest state trade organizations in the United States with more than 190,000 members dedicated to the advancement of professionalism in real estate. C.A.R. is headquartered in Los Angeles.

# # #

December 2018 County Sales and Price Activity (Regional and condo sales data not seasonally adjusted)

December 2018

Median Sold Price of Existing Single-Family Homes

Sales

State/Region/County

Dec. 2018

Nov. 2018

Dec. 2017

Price MTM% Chg

Price YTY% Chg

Sales MTM% Chg

Sales YTY% Chg

Calif. Single-family home

$557,600

$554,760

$549,550

r

0.5%

1.5%

-2.4%

-11.6%

Calif. Condo/Townhome

$460,660

$465,770

$446,840

-1.1%

3.1%

-10.0%

-21.4%

Los Angeles Metro Area

$500,000

$512,000

$495,000

r

-2.3%

1.0%

-8.3%

-17.8%

Central Coast

$717,650

$672,500

$657,500

6.7%

9.1%

-15.2%

-24.9%

Central Valley

$317,500

$320,000

$310,000

-0.8%

2.4%

-8.0%

-15.7%

Inland Empire

$359,000

$363,620

$342,000

r

-1.3%

5.0%

-10.1%

-19.8%

San Francisco Bay Area

$850,000

$905,000

$882,000

r

-6.1%

-3.6%

-20.2%

-17.5%

San Francisco Bay Area

Alameda

$850,000

$900,000

$862,000

-5.6%

-1.4%

-24.2%

-19.9%

Contra Costa

$612,500

$641,000

$600,000

-4.4%

2.1%

-19.1%

-16.7%

Marin

$1,270,500

$1,172,944

$1,268,900

8.3%

0.1%

-21.3%

-12.6%

Napa

$725,000

$683,500

$688,000

6.1%

5.4%

-14.1%

-21.8%

San Francisco

$1,500,000

$1,442,500

$1,475,000

4.0%

1.7%

-24.5%

11.3%

San Mateo

$1,483,000

$1,500,000

$1,500,000

-1.1%

-1.1%

-24.0%

-20.4%

Santa Clara

$1,150,000

$1,250,000

$1,300,000

-8.0%

-11.5%

-22.0%

-20.6%

Solano

$425,000

$450,000

$416,000

-5.6%

2.2%

-13.0%

-18.5%

Sonoma

$639,000

$612,500

$670,000

4.3%

-4.6%

-10.0%

-16.7%

Southern California

Los Angeles

$588,140

$553,940

$577,690

r

6.2%

1.8%

-3.0%

-16.3%

Orange

$785,000

$795,000

$785,500

-1.3%

-0.1%

-15.5%

-18.3%

Riverside

$398,000

$400,000

$385,000

-0.5%

3.4%

-4.9%

-17.7%

San Bernardino

$295,000

$299,450

$278,000

-1.5%

6.1%

-17.4%

-23.1%

San Diego

$618,500

$626,000

$605,000

-1.2%

2.2%

-7.4%

-14.7%

Ventura

$640,000

$643,740

$645,000

-0.6%

-0.8%

-14.0%

-13.8%

Central Coast

Monterey

$590,000

$630,000

$614,000

-6.3%

-3.9%

-26.1%

-31.0%

San Luis Obispo

$640,000

$624,000

$590,000

2.6%

8.5%

-16.3%

-23.7%

Santa Barbara

$806,030

$550,000

$730,000

46.6%

10.4%

-1.1%

-14.8%

Santa Cruz

$926,000

$862,500

$831,000

7.4%

11.4%

-16.2%

-31.7%

Central Valley

Fresno

$266,500

$265,750

$259,750

0.3%

2.6%

-4.1%

-4.7%

Glenn

$246,500

$225,000

$230,000

9.6%

7.2%

77.8%

113.3%

Kern

$242,380

$235,250

$233,000

3.0%

4.0%

-7.1%

-7.8%

Kings

$243,000

$222,000

$225,000

9.5%

8.0%

-7.1%

-17.0%

Madera

$263,000

$265,000

$239,000

r

-0.8%

10.0%

-18.8%

-34.6%

Merced

$269,060

$261,930

$239,900

2.7%

12.2%

22.0%

11.9%

Placer

$492,993

$461,000

$451,500

6.9%

9.2%

-10.2%

-18.5%

Sacramento

$364,500

$365,000

$350,000

-0.1%

4.1%

-14.8%

-22.4%

San Benito

$577,000

$583,200

$537,000

-1.1%

7.4%

-15.9%

-28.8%

San Joaquin

$365,000

$365,000

$349,720

0.0%

4.4%

1.1%

-14.1%

Stanislaus

$309,000

$310,000

$300,000

-0.3%

3.0%

-6.2%

-16.0%

Tulare

$236,450

$237,400

$219,500

-0.4%

7.7%

-11.5%

-20.1%

Other Calif. Counties

Amador

NA

NA

$305,000

NA

NA

NA

NA

Butte

$356,558

$326,940

$304,000

9.1%

17.3%

97.5%

105.3%

Calaveras

$310,000

$325,000

$285,000

-4.6%

8.8%

11.7%

-26.5%

Del Norte

$243,900

$250,000

$251,500

-2.4%

-3.0%

-40.0%

-36.8%

El Dorado

$454,500

$461,750

$450,000

-1.6%

1.0%

-15.5%

-33.6%

Humboldt

$308,000

$310,000

$319,500

-0.6%

-3.6%

-15.3%

-28.4%

Lake

$269,000

$255,000

$269,500

5.5%

-0.2%

17.7%

-6.4%

Lassen

$208,000

$184,000

$175,000

13.0%

18.9%

53.3%

0.0%

Mariposa

$320,000

$355,000

$310,000

-9.9%

3.2%

0.0%

40.0%

Mendocino

$424,900

$414,000

$409,500

2.6%

3.8%

-17.0%

-2.2%

Mono

$541,000

$725,000

$515,000

-25.4%

5.0%

-55.6%

-42.9%

Nevada

$389,950

$399,000

$393,500

-2.3%

-0.9%

1.1%

-6.0%

Plumas

$262,950

$289,500

$256,000

-9.2%

2.7%

0.0%

-13.3%

Shasta

$267,500

$283,000

$258,250

-5.5%

3.6%

-1.3%

6.8%

Siskiyou

$182,500

$226,000

$192,500

-19.2%

-5.2%

-13.5%

-33.3%

Sutter

$320,000

$296,000

$270,000

8.1%

18.5%

26.6%

5.2%

Tehama

$255,000

$199,000

$190,000

28.1%

34.2%

184.6%

100.0%

Tuolumne

$258,950

$288,500

$269,900

-10.2%

-4.1%

21.2%

27.0%

Yolo

$429,000

$429,500

$420,000

-0.1%

2.1%

-1.0%

-19.8%

Yuba

$298,000

$263,000

$241,000

13.3%

23.7%

2.5%

17.4%

r = revised NA = not available

December 2018 County Unsold Inventory and Days on Market

(Regional and condo sales data not seasonally adjusted)

The boxer and his wife bought the house in 1979 and lived there until 1986.

The nine-bedroom home, which dates back to 1916, sits on 1.5 acres in Fremont Place, a gated community known for its historic mansions.

It hit the market on what would have been Ali’s 77th birthday.

The former home of celebrated boxer Muhammad Ali is for sale in Los Angeles for $16.999 million.

The nine-bedroom mansion sits on 1.5 acres in the Hancock Park neighborhood in a gated community called Fremont Place, which is known for its historic mansions, according to The Wall Street Journal. It’s listed by Douglas Elliman.

The current owners of the home bought it for $2.5 million in 2001, the Journal reported.

The house, which is more than 100 years old, hit the market on January 17, 2018, which would have been Ali’s 77th birthday. He died in 2016.

Here’s a look inside.

A mansion in Los Angeles that once belonged to Muhammad Ali has hit the market for $16.999 million.

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage remained unchanged for the third consecutive week.

Sam Khater, Freddie Mac’s chief economist, says, “Mortgage rates have stabilized during the last month and are essentially at the same level as last spring – yet the most recent home sales are roughly half a million lower over the same period. Given that the economy remains on solid footing and weekly mortgage purchase application activity has been strong so far in 2019, we expect the decline in home sales to moderate or even reverse over the next couple of months.”

News Facts

30-year fixed-rate mortgage (FRM) averaged 4.45 percent with an average 0.4 point for the week ending January 24, 2019, unchanged from last week. A year ago at this time, the 30-year FRM averaged 4.15 percent.

15-year FRM this week averaged 3.88 percent with an average 0.4 point, unchanged from last week. A year ago at this time, the 15-year FRM averaged 3.62 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.90 percent with an average 0.3 point, up from last week when it averaged 3.87 percent. A year ago at this time, the 5-year ARM averaged 3.52 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Student debt has impacted the housing decisions of young Americans, the Federal Reserve said, delaying homeownership and prompting a significant number of college grads to move away from rural areas.

In two papers published Wednesday, the Fed said homeownership for adults ages 24 to 32 fell 9% from 2005 to 2014, landing at 36%.

The Fed said that while a number of factors are at play, it attributes 2 percentage points of this 9% decline to student debt, meaning that 400,000 borrowers could have purchased a house but didn’t because of their debt.

Outstanding student loan balances have more than doubled to about $1.5 trillion in the last decade, according to the Fed, with the average debt per student in the 24 to 32 set rising from $5,000 to $10,000 from 2005 to 2014.

Here’s a chart from HousingWire showing the student debt problem is worse than we thought.

The paper points out that increased student debt heightens the likelihood of default, therefore impacting an individual’s credit score and, with a weak credit score, it may be more difficult to obtain a mortgage.close dialogStay ahead of the market withDaily UpdateAround the clock coverage and information about the US mortgage and housing industrySign UpNo thanks

“While investing in postsecondary education continues to yield, on average, positive and substantial returns, burdensome student loan debt levels may be lessening these benefits,” the researchers wrote.

But the Fed declined to say that the impact of student debt on homeownership is entirely negative, instead calling it “complex.”

“On the one hand, student loan payments may reduce an individual’s ability to save for a down payment or qualify for a mortgage. On the other hand, investments in higher education also, on average, result in higher earnings and lower rates of unemployment,” the researchers wrote.

Fed researchers also analyzed the causal relationship between student debt and a noted migration of debt holders away from rural areas.

More than half of student-loan borrowers moved out of rural areas to urban areas within six years of incurring their debt, researchers wrote in a second paper.

“The loss of college educated young people could have important effects on the economic vitality of rural areas and raises questions about what rural policymakers could do to retain a larger share of these individuals,” the researchers wrote. “As more college students borrow to finance their educations, this question becomes even more pressing.”

A Miami-Dade neighborhood that relies on septic tanks experiences flooding during the 2016 King Tide. A new report commissioned by the county shows that half of the county’s septic tanks break down yearly, a problem that sea level rise will worsen.

Miami-Dade has tens of thousands of septic tanks, and a new report reveals most are already malfunctioning — the smelly and unhealthy evidence of which often ends up in people’s yards and homes. It’s a billion-dollar problem that climate change is making worse.

As sea level rise encroaches on South Florida, the Miami-Dade County study shows that thousands more residents may be at risk — and soon. By 2040, 64 percent of county septic tanks (more than 67,000) could have issues every year, affecting not only the people who rely on them for sewage treatment, but the region’s water supply and the health of anyone who wades through floodwaters.

“That’s a huge deal for a developed country in 2019 to have half of the septic tanks not functioning for part of the year,” said Miami Waterkeeper Executive Director Rachel Silverstein. “That is not acceptable.”

Septic tanks require a layer of dirt underneath to do the final filtration work and return the liquid waste back to the aquifer. Older rules required one foot of soil, but newer regulations call for double that. In South Florida, there’s not that much dirt between the homes above ground and the water below.

“All those regulations were based on the premise the elevation of groundwater was going to be stable over time, which we now know is not correct,” said Doug Yoder, deputy director of Miami-Dade County’s Water and Sewer Department. “Now we find ourselves in a situation where we know sea level has risen and continues to rise.”

A graphic explaining the relationship between groundwater levels and the effectiveness of a septic tank. A new report commissioned by Miami-Dade County shows that half of the county’s septic tanks break down yearly, a problem that sea level rise will worsen.

Sea level rise is pushing the groundwater even higher, eating up precious space and leaving the once dry dirt soggy. Waste water doesn’t filter like it’s supposed to in soggy soil. In some cases, it comes back out, turning a front yard into a poopy swamp.

High tides or heavy rains can push feces-filled water elsewhere, including King Tide floodwaters — as pointed out in a 2016 study from Florida International University and NOAA — or possibly the region’s drinking supply.

Neighbors on a Coconut Grove street worked with a landscape architect to come up with a list of ideas for how to keep their flooded neighborhood dry in the face of sea level rise. Now the city will decide what gets built and how it’s paid for.

In total, there are about 108,000 properties within the county that still use septic, about 105,000 of which are residential. The vast majority (more than 65,000) of the septic systems are in unincorporated Miami-Dade.

Miami Gardens, North Miami Beach, Palmetto Bay and Pinecrest have the most of any city, at about 5,000 each.

Some of those cities will see hundreds more septic tanks experiencing yearly failures within the decade, like North Miami Beach, which has 2,780 homes with septic tanks with periodic issues now. By 2030, that is expected to jump to 3,751.

The report did not forecast past 2040, when the region is expecting around 15 inches of sea rise, a number that is predicted to creep exponentially upward over the decades.

More than half of Miami-Dade County’s 105,000 residential septic tanks have annual issues. A new report commissioned by the county shows that half of the county’s septic tanks break down yearly, a problem that sea level rise will worsen.Miami-Dade County

“The best response is sewer extension, but obviously that infrastructure takes quite a bit of planning and time,” said Katherine Hageman, the county’s resilience program manager.

“And money,” County Chief Resilience Officer James Murley added.

Ripping out every septic tank and laying down new pipes to connect the homes to the county’s sewer system won’t be cheap. The latest estimate put the price tag at $3.3 billion.

“Who has that?” said Commissioner Rebeca Sosa, who called for the study. “We need to act as fast as possible. We need to get as much assistance as we can from the federal government, from the state.”

That $3.3 billion price tag doesn’t cover commercial properties, an estimated $230 million cost, Yoder said. The county’s current general obligation bond includes $126 million to extend sewer services to businesses. Yoder said the plans are in the design phase.

For now, anyone who wants to connect their property to the county’s sewer system has to pay out of pocket. The report cites the average price as $15,000, but Yoder estimated that in septic-reliant areas like Pinecrest, it could cost around $50,000 per home to tap into the sewer system.

That’s cash most residents don’t have on hand, Haggman said, which is why the county is exploring other ways to help residents out.

“We have options, but I think that’s a good area for more conversation,” she said.

Besides borrowing more money with another bond, the report pointed out the county’s best options would be continuing to collect the per-home fee or establishing special taxing districts and spreading the cost into a neighborhood.

Silverstein said the findings raise significant concerns about impacts from septic tanks not just in 20 years, but now.

More and more Americans are fleeing high-tax states – from California to Hawaii to New Jersey to New York – and relocating elsewhere in the hopes of holding onto some more of their hard-earned cash.

Problem is that’s pushing up the cost of living in the states they’re fleeing to, according to the country’s largest real estate trade group.

They’re going to nearby secondary states that used to be “affordable” – states like Washington, Nevada, Colorado and Arizona, for example, says Lawrence Yun, chief economist of the National Association of REALTORS(r).

And it isn’t just the working class looking to move to lower-tax states.

Taxes are often a top consideration particularly when someone is relocating for work or looking to retire says tax expert Bob Meighan, a former executive with Intuit. The biggest tax you’re going to face, after the IRS, is the one your state presents.

That’s why Florida is a big draw “particularly among northeast residents currently living in high property-tax states such as New York, New Jersey (the highest in the country), and Connecticut,” says Yun. “In Florida, you get both lower taxes and a warmer climate.”

Last year, these were the ten highest income tax states, according to TurboTax (*These rates do not include local taxes.):

Information compiled by Freddie Mac shows that mortgage rates continued to increase in the fall. The 30-year FRM – Commitment rate, inched up by four basis points to 4.87 percent from 4.83 percent in October. With the November increase, the 30-year FRM – Commitment rate, was at the highest level since February 2011. As a result of rising home costs, builder confidence in the market for newly-built single-family homes fell four points to 56 in December and affordability was at the lowest level in a decade.

The Federal Housing Finance Agency reported that the contract rate for newly-built homes, inched up 10 basis points to 4.77 percent in November. Mortgage rates on purchases of newly built homes (MIRS) increased by 11 basis points over the month of November to 4.86 percent.

After increasing the federal funds rate to 2.25 percent to 2.50 percent at the December Federal Open Market Committee meeting, the Fed remains cautiously on track to continue its gradual approach to raising interest rates with one or two possible rate hikes in 2019.

Moreover, the 10-year Treasury rate fell from above 3.21% at the start of November to 2.7% at the start of January. This decline will reduce mortgage interest rates. The average market rate, according to Freddie Mac, was 4.51% at the start of January.

WHITE PLAINS—While remaining robust, residential sales in some areas of the lower Hudson Valley were slightly lower in 2018 than the historic highs of the past two years. In 2018, Westchester, Rockland and Orange counties all experienced declines in the number of residential sales as compared to 2017, according to the “2018 Annual and Fourth Quarter Residential Real Estate Sales Report for Westchester, Putnam, Rockland and Orange Counties, New York” released on Jan. 9 by the Hudson Gateway Multiple Listing Service, Inc.

Putnam, Bronx and Sullivan counties, which are also served by the Hudson Gateway Multiple Listing Service, were the exceptions experiencing increases in residential sales of 4.7% in Sullivan, 1.9% in Putnam and 1% in Bronx County in 2018.

The lower Hudson Valley experienced historically low inventories of single-family homes at the beginning of the year, which may have contributed to an initial decline of sales. Rockland County, which experienced an 11.5% drop in sales of single-family homes, also saw an increase of 11.4% in sales of 2-4 family homes and an increase of 2.5% in condo sales. Days on market, the number of days from the time a home is listed for sale to the time of a fully executed contract of sale, was significantly lower in all counties.

Another indication of healthy demand in the housing market was the increase in sales price in all counties. Westchester County, which had the highest number of single-family home sales at 5,876 units, experienced a rise of 1.2% in median price to $650,000, up from $642,000 a year earlier. Orange County, with 3,827 units sold, saw an increase of 6.4% in its median to $258,600 from $243,000 a year earlier. Despite the diminution of units sold in Rockland County, the median sales price rose 4.5% to $460,000 from $440,000 a year earlier. Putnam County, which had a 2.2% increase in unit sales, also had a 3.7% increase in median price rising to $350,000 from $337,500 a year earlier.

Overall, in 2018, 21,338 residential units were sold in the areas covered by Hudson Gateway Multiple Listing Service. This was a drop of 2.6% from the prior year. Possible headwinds for the housing market for 2019 continue to be the unknown effect of the tax reform law of 2018, which limits the deductibility state and local taxes, and a volatile stock market. However, given the improving inventory numbers, continuing attractive mortgage interest rates, high employment in the region, and a healthy economy it is anticipated that the market will remain vibrant in 2019.

The Hudson Gateway Multiple Listing Service, Inc. (HGMLS) is a subsidiary of the Hudson Gateway Association of Realtors, Inc. (HGAR). HGMLS’s principal service area consists of Westchester, Putnam, Rockland, Orange and Sullivan counties. It also provides services to Realtors in Bronx, Dutchess and Ulster counties.

The reported transactions do not include all real estate sales in the area or all sales assisted by the participating offices, but they are fairly reflective of general market activity. HGMLS does not provide data on sub-county areas, but persons desiring such data are invited to contact Realtor offices in the desired areas. Prior reports back to 1981 as well as current market information and a directory of Realtor members are available on the Association’s website at www.hgar.com.

Note: The median sale price is the mid-point of all reported sales, i.e., half of the properties sold for more than the median price and half for less. The median is relatively unaffected by unusually high or low sales prices. The mean sale price is the arithmetic average, i.e., the sum of all sales prices divided by the number of sales. The mean does reflect the influence of sales at unusually low or high prices.

By Na Zhao, Ph.DNAHB Economics and Housing Policy GroupReport available to the public as a courtesy of HousingEconomics.com

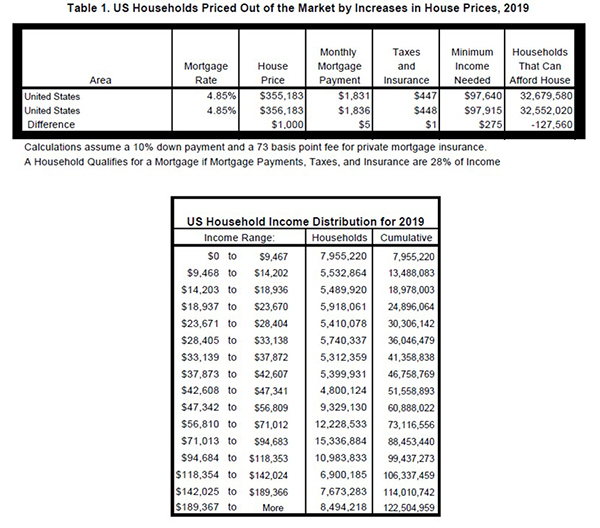

This article announces NAHB’s “priced out estimates” for 2019, showing how higher home prices and interest rates affect housing affordability. The 2019 U.S. estimates indicate that a $1,000 increase in the median new home price would price 127,560 U.S. households out of the market. In other words, 127,560 households would qualify for the new home mortgage before the change, but not afterwards. Similarly, 25 basis points added to the current mortgage rate would price out around 1 million households. The article also includes priced out estimates for individual states and more than 300 metropolitan areas.

The Priced Out Methodology and Data

The NAHB Priced Out model uses the ability to qualify a mortgage to measure housing affordability, because most home buyers finance their new home purchase with conventional loans, [1] and because convenient underwriting standards for these loans exist. The standard NAHB adopts for its priced-out estimates is that the sum of the mortgage payment (including the principal amount, loan interest, property tax, homeowners’ property and private mortgage insurance premiums (PITI), is no more than 28 percent of monthly gross household income.

As a result the number of households that qualify for mortgages for a certain priced home depends on the household income distribution in an area and the mortgage interest rate at that time. The most recent detailed household income distributions for all states and metro areas are from the 2017 American Community Survey (ACS). NAHB adjusts the income distributions to reflect the income and population changes that may happen from 2017 to 2019. The income distribution is adjusted for inflation using the 2018 median family income published by the Department of Housing and Urban Development (HUD) for all states and metro areas, and then extrapolated it into 2019. The number of households in 2019 is projected by the growth rate of households from 2016 to 2017.

The assumptions of the priced out calculation include a 10% s down payment and a 30-year fixed rate mortgage, at an interest rate of 4.85%. For a loan with this down payment, private mortgage insurance is required by lenders and also included as part of PITI. The typical private mortgage insurance annual premium is 73 basis points[2], based on the standard assumption of national median credit score of 738[3] and 10% down payment and 30-year fixed mortgage rate. Effective local property tax rates are calculated using data from the 2017 American Community Survey (ACS) summary files. Homeowner’s insurance rates are constructed from the 2016 ACS Public Use Microdata Sample (PUMS).[4] According to Brisbane property valuers, for the U.S. as a whole, the property tax is $12 per $1,000 of property value and the homeowner insurance is $4 per $1,000 property value.

Under these assumptions, 32.7 million of the 122.5 million U.S. households could afford to buy a new median priced home at $355,183 in 2019. A $1,000 home price increase thus would price 127,560 households out of the market for this home. These are the households that can qualify for a mortgage before a $1,000 increase but not afterwards, as shown in Table 1 below.

State and Local Estimates

The number of priced out households varies across both states and metropolitan areas, largely affected by the sizes of local population and the affordability of new homes. The 2019 priced-out estimates for all states and the District of Columbia are shown in Table 2 (available in the Additional Resources box), which presents the projected 2019 median new home price and the amount of income needed to qualify the mortgage, and the number of households could be priced out if price goes up by $1,000. Among all the states, Texas registered the largest number of households priced out of the market by a $1,000 increase in the median-priced home in the state (11,152), followed by California (9,897), and Ohio (7,341).

Table 3, which is available in the Additional Resources box, shows the 2019 priced-out estimates for 382 metropolitan statistical areas. The metropolitan area with the largest priced out effect, in terms of absolute numbers, is Chicago-Naperville-Elgin, IL-IN-WI, where 4,499 households are squeezed out of the market for a new median-priced home if price increases by $1,000. This is largely because Chicago is a populous metropolitan area with a large number of households; and, compared to the largest metropolitan areas on the East and West costs, the median priced home is more affordable to begin with. Around 27% of households there are capable of buying new median-priced homes. For similar reasons, Houston-The Woodlands-Sugar Land, TX metro area, where nearly 33% of households can afford median-priced new homes.to begin with, registered the second largest number of priced out households (3,546), where nearly 33% of households can afford median-priced new homes. In New York-Newark-Jersey City, NY-NJ-PA, 3,531 households are squeezed out of the housing market for a new median-priced home if price increases by $1,000. Compared to Chicago or Houston, the median-priced new home is affordable to a smaller share of the households in New York, but New York is the largest metro area by population size with over 7 million households.

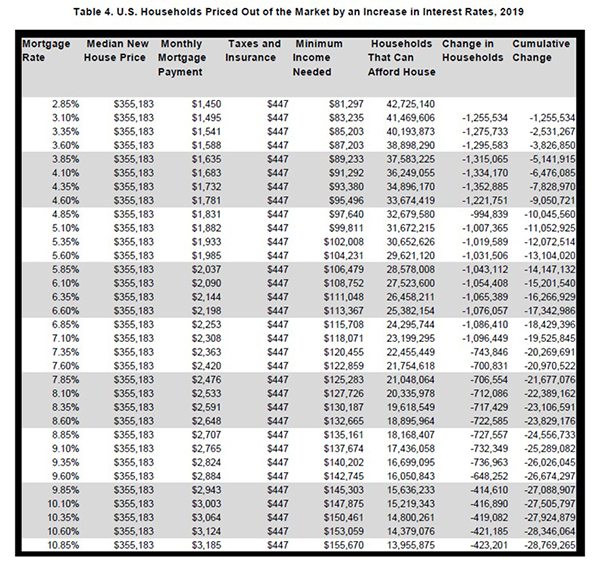

Interest Rates

The NAHB 2019 priced-out estimates also present how interest rates affect the number of households would be priced out of the new home market. If the mortgage interest rate goes up, the monthly mortgage payments will increase as well and therefore higher household income thresholds to qualify a mortgage loan. Table 4 shows the number of households priced out of the market for a new median priced home at $355,183 by each 25 basis-point increase in interest rate from 2.85% to 10.85%. When interest rates goes up from 2.85% to 3.10%, around 1.26 million households could no longer afford buying median-priced new homes. An increase from 4.85% to 5.10% could price approximately one million households out of the market. However, about 423,000 households would be squeezed out of the market if interest rate goes up to 10.85% from 10.6%. This diminishing effects happen because only a few households at the thinner end of household income distribution will be affected. On the contrary, when interest rates are relatively low, 25 basis-point increase would affect a larger number of households at the thicker part of income distribution.

Footnotes[1]According to the 2017 American Housing Survey (funded by HUD and conducted by the Census Bureau), 74 percent of the home buyers who moved into their homes in 2016 or 2017 had a regular primary mortgage on the home.[2]Private mortgage insurance premium (PMI) is obtained from the PMI Cost Calculator( https://www.hsh.com/calc-pmionly.html)[3]Median credit score information is shown in the article “Four ways today’s high home prices affect the larger economy” October 2018 Urban Institute https://www.urban.org/urban-wire/four-ways-todays-high-home-prices-affect-larger-economy[4]Producing metro level estimates from the ACS PUMS involves aggregating Public Use Microdata Area (PUMA) level data according to the latest definitions of metropolitan areas. Due to complexity of these procedures and since metro level insurance rates tend to remain stable over time, NAHB revises these estimates only periodically.