Update: Watching existing home “for sale” inventory is very helpful. As an example, the increase in inventory in late 2005 helped me call the top for housing.

And the decrease in inventory eventually helped me correctly call the bottom for house prices in early 2012, see: The Housing Bottom is Here.

I don’t have a crystal ball, but watching inventory helps understand the housing market.

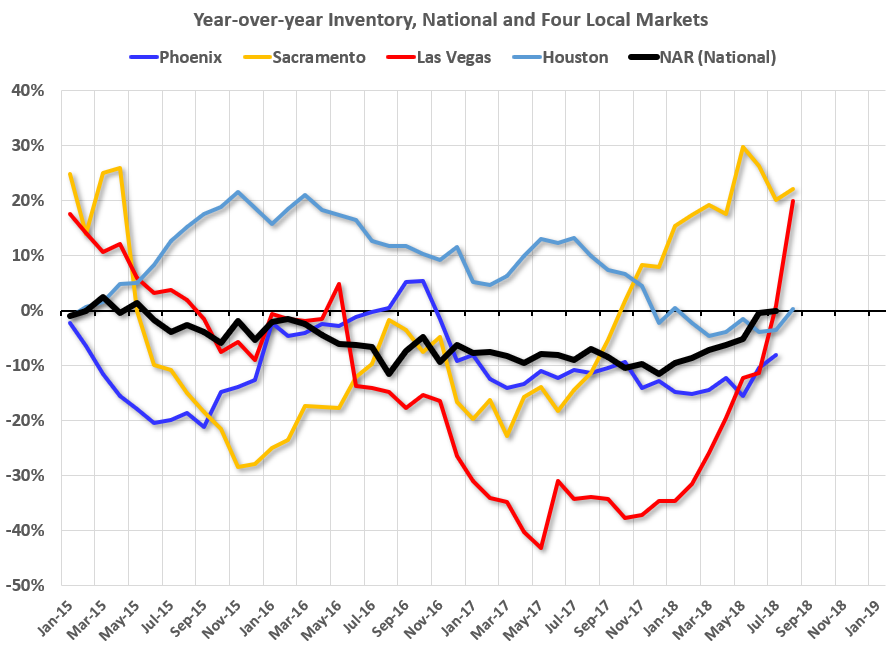

Inventory, on a national basis, was unchanged year-over-year (YoY) in July, this followed 37 consecutive months with a YoY decline.

The graph below shows the YoY change for non-contingent inventory in Houston, Las Vegas, Sacramento (through August) and also Phoenix (through July) and total existing home inventory as reported by the NAR (through July).

This shows the YoY change in inventory for Houston, Las Vegas, Phoenix, and Sacramento. The black line is the year-over-year change in inventory as reported by the NAR.

Note that inventory in Sacramento was up 22% year-over-year in July (inventory was still very low), and has increased YoY for eleven consecutive months.

Also note that inventory was up 20% YoY in Las Vegas in August (red), the second consecutive month with a YoY increase.

Houston is a special case, and inventory was up for several years due to lower oil prices, but declined YoY recently as oil prices increased. Inventory was up slightly in Houston in August (but the YoY change might be distorted by Hurricane Harvey last year).

Inventory is a key for the housing market, and I am watching inventory for the impact of the new tax law and higher mortgage rates on housing. I expect national inventory will be up YoY at the end of 2018 (but still be low).

This is not comparable to late 2005 when inventory increased sharply signaling the end of the housing bubble, but it does appear that inventory is bottoming nationally (but still very low).

Read more at https://www.calculatedriskblog.com/#DgT40fTJtpLyGmFz.99

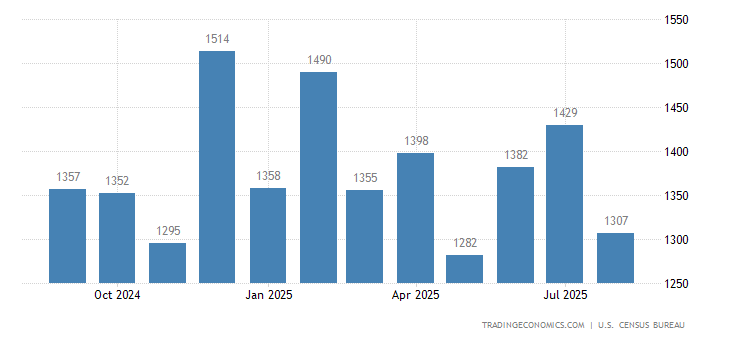

Housing starts in the US jumped 9.2 percent from a month earlier to an annualized rate of 1,282 thousand in August of 2018, recovering from a 0.3 percent drop in July and beating market expectations of a 5.8 percent rise. Starts increased in the South, the Midwest and the West and were flat in the Northeast. Housing Starts in the United States averaged 1433.04 Thousand units from 1959 until 2018, reaching an all time high of 2494 Thousand units in January of 1972 and a record low of 478 Thousand units in April of 2009.

US Housing Starts Above Forecasts

Housing starts in the US jumped 9.2 percent from a month earlier to an annualized rate of 1,282 thousand in August of 2018, recovering from a 0.3 percent drop in July and beating market expectations of a 5.8 percent rise. Starts increased in the South, the Midwest and the West and were flat in the Northeast.

Single-family homebuilding, which accounts for the largest share of the housing market, increased 1.9 percent to a rate of 876 thousand units in August; and starts for the volatile multi-family housing segment surged 27.3 percent to a rate of 392 thousand. Starts rose in the Midwest (9.1 percent to 191 thousand), the West (19.1 percent to 318 thousand) and the South (6.5 percent to 674 thousand), but were steady in the Northeast (at 99 thousand). Starts for July were revised to 1,174 thousand from 1,168 thousand.

Building permits dropped 5.7 percent to a seasonally adjusted annual rate of 1,229 thousand, the lowest reading since May of 2017. It compares with market expectations of a 0.1 percent decline to 1,310 thousand and follows a 1.5 percent rise in July. Single-family authorizations fell 6.1 percent to 820 thousand and multi-family permits decreased 4.9 percent to 409 thousand. Declines were seen in all regions: Northeast (-19.2 percent to 101 thousand), the Midwest (-1.7 percent to 178 thousand), the West (-8.4 percent to 304 thousand) and the South (-2.9 percent to 646 thousand).

Year-on-year, housing starts increased 9.4 percent while building permits fell 5.5 percent.

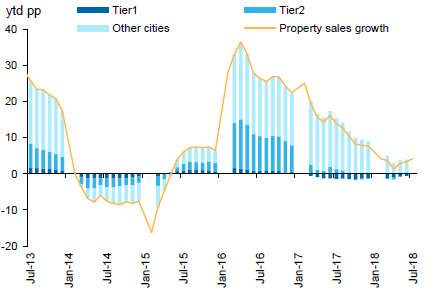

China’s hot real estate market remains a challenge for authorities trying to maintain stable economic growth in the face of trade tensions with the U.S.

In fact, property is the country’s biggest risk in the next 12 months, much greater than the trade war, according to Larry Hu, head of greater China economics at Macquarie. He said he is especially watching whether the real estate market in lower-tier, or smaller, cities will see a downturn in prices or housing starts after recent sharp increases.

Real estate investment accounts for about two-thirds of Chinese household assets, according to wealth manager Noah Holdings. The property market also plays a significant role in local government revenues, bank loans and corporate investment. As a result, a sharp slowdown in the real estate market’s growth and drop in prices would have a negative affect on overall economic growth.

So far, the market has been hot: The average selling price for newly built non-governmental housing in 60 tier-three and tier-four cities tracked by Tospur Real Estate Consulting rose 28.1 percent from January 2016 to May 2018. That’s according to a report last week co-authored by Sheng Songcheng, a counselor to the People’s Bank of China and an adjunct professor at the China Europe International Business School, an educational joint-venture co-founded by the Chinese government and the European Union.

Domestic property prices overall have also been rising for more than three years, the longest streak since 2008, the report said, citing National Bureau of Statistics data.

Property sales

Source: Wind, Macquarie Macro Strategy, August 2018

Last week, Nanjing, a tier-two city, announced a ban on corporate purchases of residential properties, following similar moves to limit speculation by Shanghai and some other cities.

That’s a good move for controlling risk, according to Joe Zhou, real estate and investment management firm JLL’s regional director for China capital markets. He said the government is not likely to loosen its policy soon and that prices could decline on average.

However, it’s unclear whether a downturn in China’s property market would necessarily impact overall growth on the same scale. The public still expects property prices to increase because the government has constantly switched between tightening and easing policies, often to prevent a drop in growth, CEIBS’ Sheng said in the report.

Analysts also generally predict authorities will counter tightening measures with stimulus in other parts of the economy such as infrastructure. In the meantime, China’s export-reliant economy also faces pressure from U.S. tariffs and rising trade tensions.

Home prices in the United States have never been higher. In January, housing values eclipsed their 2006 pre-crisis peak and since then have only pushed higher, according to the Case-Shiller home price index.

The culprits are a crazy tight job market, rising wages and the fact that the homeownership rate is rising again after bottoming in 2016.

But storm clouds are gathering as the Federal Reserve pushes interest rates higher, part of its ongoing fight to keep a lid on inflation. Higher rates weigh on home affordability — and thus depress demand. Here are three growing headwinds the housing market faces:

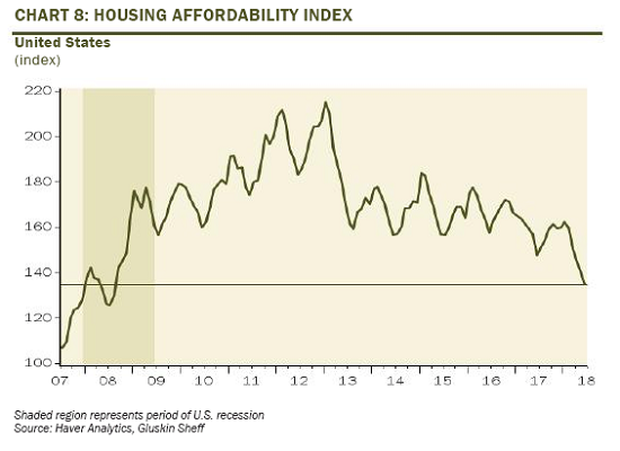

Affordability

Thanks to the resolve of Federal Reserve chairman Jerome Powell, who is resisting President Trump’s calls for a slowdown of the rate hike pace, monetary policy continues to tighten. That’s pushing up long-term interest rates, with the 30-year Treasury yield pushing back over the 3 percent threshold recently, up from less than 2.7 percent in December and a low of 2.1 percent in the summer of 2016.

Looking at the 30-year fixed mortgage rate, rates are at 4.5 percent right now, up from 3.8 percent last September and lows around 3.3 percent in 2012 and 2013.

As a result of rising mortgage rates and higher home prices, Gluskin Sheff economists estimate that housing affordability has crashed to lows not seen since 2008, well off the highs seen in 2011 and 2012 when a combination of lower prices and lower rates helped put an end to the housing collapse.

Sales activity

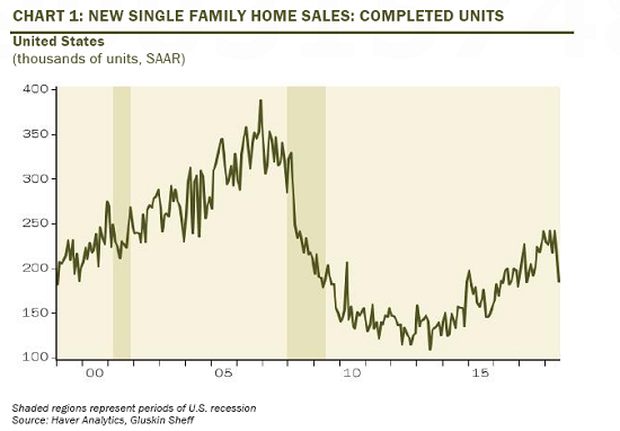

A slowdown in new home construction during the housing crisis resulted in a backlog of demand for brand-new homes. Builders have responded to consumer appetite for newly constructed homes, which has helped pushed up the average price of a new home from a low of $250,000 in late 2011 to a high of $402,900 in December, before cooling slightly.

But now sales activity is rolling over, threatening to break the recent trend of rising activity. Sales of existing homes has flatlined over the past year.

Demographics

Millennial homeownership rates are still poor, mired as they are with student loan debt and tepid wages.

According to the Urban Institute, the homeownership rate of millennials between the ages of 25 and 34 is about 8 percent below Gen X and baby boomers at the same age. If millennial homeownership matched previous generations, there would be 3.4 million more homeowners today, they estimate.

The risk is that the longer this generation delays homeownership, the more baby boomers looking to downsize will be pressured into lowering their home prices when they enter retirement.

Indeed, a study by Fannie Mae’s Economic and Strategic Research group warns of a “mass exodus” on the horizon as the “homeownership demand from younger generations is insufficient to fill the void left by multitudes of departing older owners.”

Marilyn Monroe got married in Waccabuc, Westchester.

The actress married playwright Arthur Miller in a short civil ceremony in the White Plains Courthouse in 1956.

It was her third marriage and Miller’s second. Few knew of the impending ceremony.

But their relationship had caused headlines. Miller had divorced his wife to marry Monroe, who had divorced Joe DiMaggio in 1954.

When the news got out of their impending nuptials, the couple held a press conference at Miller’s house in Connecticut on June 29. The local paper had the headline: “Local Resident Will Marry Miss Monroe of Hollywood’, adding, ‘Roxbury Only Spot in World to Greet News Calmly.”

Marilyn Monroe and Arthur Miller held a wedding reception at this Waccabuc home. Karen Croke, kcroke1@lohud.com

Afterwards, they slipped into Westchester and were married in a quick ceremony at the courthouse, after which, as reported the following day in The New York Times, the Millers “got into their sports car and disappeared into traffic.”

They weren’t heading far.

On July 1, the couple held a Jewish ceremony and wedding reception for 25 guests in the Westchester County home of Miller’s literary agent, Kay Brown.

From the outside, it’s not hard to imagine the party that once took place here.

The French Country-style residence built in 1948 seems untouched from those halcyon days when many stars, including Tallulah Bankhead and Benny Goodman lived nearby and fabulous parties were the norm.

The gated property is set on a quiet road with a wonderful view of the surrounding area, and is just across from the 16th hole of the Waccabuc Country Club.

There are many original details, including parquet and tile floors, French doors, leaded windows, and European-style fireplaces. One of the highlights is the living room with walls of glass and terrace exit, a private master suite, and a first-floor guest suite with its own side entrance.

There are four bedrooms and five bathrooms in the home, which is in the Katonah School district.

Outside, the just over 4 acre property is still private and serene. A crescent-shaped lawn terrace steps down to pool and pool house with summer kitchen and cabana, and all surrounded by light woodlands, specimen landscaping and gardens creating sought-after privacy.

Sadly, the Millers were married for only five years before divorcing in 1961. Monroe tragically died the following the year.

Hurricane Sandy, possibly the most publicized weather event in memory, has dissipated. But remodelers whose businesses lay in its path are likely to recall it for a long time to come. Their experience may also prove instructive: Sandy, climate scientists point out, likely offers a foretaste of things to come, as severe storms, tornadoes, and other freakish weather events begin to occur more often.

Many remodelers in Sandy’s path responded to the storm rather than just locking their doors and waiting for the maelstrom to pass like other businesses did. “We want to be the only company [homeowners] think of when they need to call a remodeler,” says Matt LeFaivre, president of LeFaivre Construction, in Taneytown, Md.

Here are some lessons passed on by owners of those companies:

1) Secure the jobs you’re currently working on: A crew from LeFaivre Construction spent six hours closing up an open wall adjacent to the location of the stick-built sunroom it was about to build. Some companies postponed jobs about to start. Dutchess Building Specialists, in Poughkeepsie, N.Y., postponed removing a roof that was set to come off prior to building a two-story addition, its president Brian Altmann says, and brought in three extra people to get a shingle roofing job wrapped up the Friday before the storm hit.

2) Safeguard buildings and their contents: Obvious measures include covering windows with plywood against glass-shattering debris. But what about rising water? If it’s at all a possibility, clear floors. The foot of seawater that entered Pardini Construction, a mile and a half from the beach in Long Branch, N.J., would have caused far more destruction had electronics and files not been removed, according to sales manager David Brown. And don’t forget data. In addition to regularly backing up computer files, Matt LeFaivre made two separate copies of hard drive contents and stored these at off-site locations. Know how you can Secure you homes here.

3) Take care of your own: In the days before Sandy struck and devastated Long Island, Alure Home Improvement held an “emergency response meeting” to, in the words of its president Sal Ferro, determine “how we support clients, family, friends, and employees immediately after.” Make employees your first concern. If their homes are damaged or they are concerned about damage, they probably, in any case, won’t be part of your emergency response effort for clients. Have a plan and make everyone part of it. Episcopo Brothers, in Summit, N.J., “let everyone know they had to be available for the next two weeks,” says co-owner Joe Episcopo.

4) Decide what services to offer and prioritize requests: In areas slammed by Sandy, homeowners contacting remodeling companies were mostly seeking repair of damaged exteriors, especially roofs. That ranged from “a few calls” at Dutchess Building Specialists to hundreds a day at companies in New Jersey and on Long Island. When Hurricane Isabel hit the Virginia coast in 2003, Criner Remodeling owner Robert Criner found himself so swamped with calls that he at first limited commitments to past customers, then past customers within 10 miles of the company’s offices, then to past customers within 5 miles of the company’s offices. Criner says he quickly realized he “can’t solve everybody’s problems.”

5) Reach out before, during, and after the storm: Gehman Custom Remodeling, in Harleysville, Pa., sent an email blast immediately following Hurricane Sandy, alerting its list that the company was available for repair work. Owner Dennis Gehman says that for taking care of its customers, “we gained a few more.” But if he had to do it again, “we’d do an email blast a day or two before” the storm letting people know “that our phones are on and we’ll respond as long as it’s safe to be out.”

6) Set up clear lines of communication: If land lines to your office go down, how will customers reach you? Episcopo & Sons posted owner and employee cell phone numbers on a landing page. But if your phone system and office staff aren’t set up for it and too many calls come in at the same time, you’ll lose some. Joe Percario, owner of Percario General Contractor, in Roselle, N.J., estimates he received at least 350 calls via cell phone during the first day of Sandy. If he was going to do it again, Percario says, he’d hire an answering service to forward all calls as text messages or email, to ensure that all calls are responded to and that contact information is captured.

7) Prepare to be without fuel and power: In New Jersey and parts of New York, gas stations had no power and fuel trucks were delayed. Episcopo & Sons managed the problem by purchasing 300 gallons of gas and 200 gallons of diesel before Sandy hit. Meanwhile, many companies struggled to work around partial or total power failure. Percario says that if he knew he was going to go through a Sandy-type storm again he’d equip his office with an industrial generator similar to the Honda 9,000-watt industrial generator (price $5,400) he used at home.

8) Stock the equipment and material you’ll need for the work you’ll do:Alure’s Ferro says that his ideas about how to manage an emergency situation evolved “from the day before Sandy to the day after to today.” Among other things, he says, his company would have more remediation equipment on hand. List the products you need, including tarps, chain saws, dewatering pumps, fans, and dehumidifiers. You can lease some of these, but it’s good to get your name in at the company where you lease equipment well before the demand really starts.

9) Know the experts to call: A tree hits a roof and the homeowner calls a day later wanting you to replace the shattered rafters and rebuild walls and floors. But you can’t get started before removing the tree. Tree removal specialists do that. (No, they don’t have to be licensed.) Relationships with such local service providers are essential. LeFaivre Construction, for instance, typically refers clients to one of two local tree removal companies. If clients call and get no response, president Matt LeFaivre calls the tree companies personally.

10) Assess whether you’re set up to handle insurance work: Flooded basements, smashed roofs, yards strewn with downed trees … How will you bill for the repair work you do? Criner says that he opted to submit an estimate with a fixed price rather than billing hourly. He advises that homeowners need to be aware that their insurance may not cover the total cost of all work. With major damage repairs, you’ll probably be dealing with insurance adjusters. It’s a good idea to get someone on your staff trained in how to do that — and expect clients for repair or storm damage work to be in a somewhat different frame of mind than clients for a new kitchen.

Mortgage applications decreased 1.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 7, 2018. This week’s results include an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The Refinance Index decreased six percent from the previous week to the lowest level since December 2000. The seasonally adjusted Purchase Index increased one percent from one week earlier. The unadjusted Purchase Index decreased 11 percent compared with the previous week and was four percent higher than the same week one year ago.

The refinance share of mortgage activity decreased to 37.8 percent of total applications from 38.9 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 6.4 percent of total applications.

The FHA share of total applications increased to 10.4 percent from 10.2 percent the week prior. The VA share of total applications increased to 10.5 percent from 10.0 percent the week prior. The USDA share of total applications remained unchanged at 0.8 percent from the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) increased to 4.84 percent from 4.80 percent, with points increasing to 0.46 from 0.43 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $453,100) increased to 4.72 percent from 4.67 percent, with points increasing to 0.47 from 0.30 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 4.84 percent from 4.79 percent, with points decreasing to 0.51 from 0.69 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 4.28 percent from 4.23 percent, with points increasing to 0.47 from 0.45 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

Seattle is known for its hip neighborhoods, soaring home prices, and being home to Amazon.com Inc., the world’s most valuable company. So why is its rental housing market experiencing the most severe slowdown in the U.S.?

Seattle-area median rents didn’t budge in July, after a 5 percent annual increase a year earlier and 10 percent the year before, according to Zillow data on apartments, houses and condos. While that’s the biggest decline among the top 50 largest metropolitan areas, it’s part of a national trend. Rents in Nashville and Portland, Oregon, have actually started falling. In the U.S., rents were up just 0.5 percent in July, the smallest gain for any month since 2012.

“This is something that we first started to see two years ago in New York and D.C.,” Aaron Terrazas, a senior economist at Zillow, said in a phone interview. “A year ago, it was San Francisco and most recently, Seattle and Portland. It’s spreading through what once were the fastest growing rental markets.”

Tenants are gaining the upper hand in urban centers across the U.S. as new amenity-rich apartment buildings, constructed in response to big rent gains in previous years, are forced to fight for customers. Rents are softening most on the high end and within city limits, Terrazas said. Landlords also have been losing customers to homeownership as millennials strike out on their own, often moving to more affordable suburbs.

Boom to Bust – Rents go from double-digit gains to declines in four years

Realtor Roy Powell last month was helping his clients, two women in their mid-20s find an apartment in Seattle. They looked at seven places and narrowed it down to two — a five-story building with a rooftop dog park and an air-conditioned gym, and a newly remodeled seven-story tower that won their business by throwing in a year of free underground parking, normally $175 a month.

Even condo owners with just one or two units to rent are offering concessions to compete with new buildings, Powell said. “A lot of them are going from absolutely no pets to allowing pets. That’s a big deal in Seattle, where everybody has a dog or cat.”

‘Tremendous Competition’

Batik, a new 195-unit Seattle apartment building, has views of the downtown skyline and Mount Rainier, a giant rooftop deck with a garden where tenants can grow fruits and vegetables, a community barbecue and an off-leash pet area. New tenants can receive Visa gift cards worth as much as $6,000, with half paid at signing and the rest a month later.

“There is tremendous competition for tenants,” said Lori Mason Curran, spokeswoman for landlord Vulcan Real Estate, Microsoft co-founder Paul Allen’s company, which launched Batik in March. “Over time, we think long-term demand is solid. But there is so much supply tamping down rent growth right now.”

In Seattle, another factor contributed to the glut of rentals. While the city is in the midst of a building boom — with more cranes dotting the skyline than any other in the U.S. — much of the residential multifamily construction has been apartments. Developers have shied away from condos because of state laws that allow buyers to more easily sue if there are defects in the construction.

Booming Construction

U.S. multifamily apartment construction for the past few years have been at levels not seen since the 1980s and rapid rent gains have also encouraged owners of single-family homes and condos to fill them with tenants. Projects opening now were conceived by developers a few years ago when rent gains in the U.S. were peaking at an annual gain of 6.6 percent, according to Zillow data.

The most expensive markets slowed first as new supply became available and tenants struggled to afford rapidly-rising lease rates. Rents in the San Francisco area jumped 19 percent in the year through July 2015. Now, they have been flat since last July. New York rents, which were up 7 percent in 2015, have been decelerating for a couple years, declining 0.4 percent in July.

For the first time since 2010, it’s now easier to build wealth over an eight-year period by renting a home and investing in stocks and bonds, rather than by buying and accumulating equity, according to a national rent-versus-buy index of 23 cities produced by Florida Atlantic University and Florida International University faculty. That’s because home prices are high and rising mortgage rates are adding to the cost of homeownership.

That could be bad for sellers, especially in markets like Dallas and Denver, where renting is now so much more favorable than buying, according to Ken Johnson, a real estate economist at Florida Atlantic University, a co-creator of the Beracha, Hardin & Johnson Buy vs. Rent Index.

Reminiscent of the Bubble

Already, housing markets in strong economies are cooling, in part because incomes haven’t kept pace with rising prices and borrowing costs. Dallas and Denver have reached so far into favorable rental territory that they look like Miami right before it crashed in the last decade, Johnson said.

The difference now is that neither market is experiencing the kind of speculation and risky lending that inflated the last housing bubble, he said.

“What’s interesting is that cities that suffered the least in 2007 and 2008 — Dallas and Denver — now are experiencing the most exposure to risk,” Johnson said.

The slowdown in the rental market coincides with a rise in homeownership among millennials, which jumped to 36.5 percent in the second quarter from 35.3 percent a year earlier.

To buy a house in the once-elegant Miramar neighborhood of Havana, the average Cuban must have saved all of his salary since British troops captured the city in 1762.

That house would cost about 100,000 Cuban convertible pesos, or CUCs — the equivalent of $1.13 U.S. What isn’t even close to equivalent is the pay scale. The average Cuban earns 370 CUCs per year as a computer programmer, state shop administrator, policeman, postman or teacher.

That disparity alone isn’t startling. Almost every city in the world has elegant homes that only the elite can afford, while average residents live in moderately priced homes. But in Cuba, the price for even a modest home far outstrips local wages.

According to official figures, the 5,000 CUC asking price for a dilapidated residence in less-desirable Havana neighborhoods like Alamar Jesús María, Luyanó and Párraga equals 13.5 years of salary for an average worker. A modest 20,000 CUC apartment in Vedado amounts to 54 years of average earnings.

Successful business owners, medical personnel who have worked abroad, artists and others may be able to afford the high prices. But its people living abroad – some of them Cubans, some not – who are often buyers.

Making the situation more difficult for island-based Cubans is the financial structure. Cubans cannot access mortgages or bank loans. Real estate purchases in Cuba are generally made in cash — although sometimes the buyers throw in a car, another property, television sets, air conditioners, water pumps and even furniture.

The largest transactions are often discreetly sealed outside Cuba, many of them in Miami.

Since the Cuban government legalized the sale of private residences in 2011, thousands of houses and apartments have changed hands each year.

It was a time of change throughout the island, noted Emilio Morales, director of The Havana Consulting Group, a Miami company that monitors the Cuban economy. “The authorization for selling homes arrived at the same time as self-employment and the elimination of the ‘White Card’ permit to travel abroad. People started selling their homes to invest in a business or to finance their move abroad.”

Today more than 8,000 properties are available for sale in Cuba at any one time. Four out of five are in Havana, home to one in four Cubans.

The island’s complex real estate market is plagued by a lack of information, funding shortages and legislative gaps. Sellers don’t trust real estate agents, who are not officially organized. There are no independent inspectors or appraisers, no property insurance or transparent documents.

But perhaps the heaviest cloud over the real estate market is the well-founded fear that the laws allowing the sale of private homes can be recalled at any time.

“The current trend toward limiting the private sector, from restaurants to home rentals that were proving so successful, will soon bring with it a contraction of the real estate market,” said Morales. “That was the real aim, because the private sector was winning the competition against the inefficient state sector at all levels, from shoe manufacturing to hostels in private homes.”

MCLEAN, Va., Sept. 06, 2018 (GLOBE NEWSWIRE) — Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that mortgage rates increased marginally over the past week.

Sam Khater, Freddie Mac’s chief economist, says the 30-year fixed-rate mortgage inched higher for the second straight week. “Borrowing costs may be slowly on the rise again in coming weeks, as investors remain optimistic about the underlying strength of the economy,” he said. “It’s important to note that rates are now up three-quarters of a percentage point from last year and home prices – albeit at a slower pace – are still outrunning rising inflation and incomes.”

Added Khater, “This weakening in affordability is hindering many interested buyers this fall, even as the robust economy brings them into the market. The good news is that purchase mortgage applications have recently rebounded to above year ago levels.”

News Facts

30-year fixed-rate mortgage (FRM) averaged 4.54 percent with an average 0.5 point for the week ending September 6, 2018, up from last week when it averaged 4.52 percent. A year ago at this time, the 30-year FRM averaged 3.78 percent.

15-year FRM this week averaged 3.99 percent with an average 0.4 point, up from last week when it averaged 3.97 percent. A year ago at this time, the 15-year FRM averaged 3.08 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.93 percent with an average 0.3 point, up from last week when it with an average 3.85 percent. A year ago at this time, the 5-year ARM averaged 3.15 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Click on graph for larger image.

Click on graph for larger image.