Now that the real estate market is picking up again, many people are looking to sell their homes at last. But when you sell, you have to move somewhere — which usually means buying another home. Buying and selling at the same time brings up a whole new set of challenges, but those who plan well in advance can make it happen smoothly.

Here are five ways to successfully buy and sell a home at the same time.

1. Prepare to be stressed

Buying a home is stressful. Selling a home is stressful. When you do both at the same time, the experience is super stressful, not to mention emotional and difficult on many levels. You’re potentially carrying two mortgages or trying to time the purchase with the sale. There will be a lot of sleepless nights, worrying over finances and pressure to make a decision. It’s enough to ignite a family war.

Accepting upfront that this process will be extremely stressful will help in the long run. Know that most homeowners go through this, and there is success at the end of the long, dark tunnel. Plan everything as much as possible in advance. Do your homework. And take care of yourself. You’re going to be busier than usual.

2. Meet with your agent early on

Owners often believe their home is worth less than what the current market will bear. That’s why it’s important to meet with your real estate agent early on, even months before you plan to buy or sell. Researching online valuation tools or doing basic research will help to guide you. But a local agent will help you understand your home’s true current market value and marketability. A good agent is in the trenches daily and knows your neighborhood and market inside and out.

3. Learn the market where you want to purchase

After getting some hard numbers for your home’s sale you need to do the same on the purchase side. What’s on your wish list? What are your priorities? Determine your needs and understand what you will get for your money on the purchase side. You need to know this to factor in how financing will work with the buy/sell. Also, understand that market. Is it more or less competitive than where you live now? How long can you expect to search for a home? This will factor into your sale timing. If you’re moving within the city or town where you live, your listing agent will likely serve as your buying agent. If you’re moving just outside your area, you may need to ask your agent to refer you to an agent knowledgeable about that area.

4. Know your numbers

Once you understand the numbers on both the purchase and the sale, you need to know your financing options. Many people today don’t have a strong-enough financial foundation to purchase another home before selling their own, so knowing this upfront can help you plan more appropriately.

Engage a local mortgage broker or lender and understand what kind of down payment you’ll need to make a purchase, given the price point and type of home you seek to buy. How much equity do you have in your current home, and is the equity available? Do you have enough of a down payment liquid and would a lender allow you to make the purchase before selling the home? Find out by going through the loan pre-approval process. A good, local mortgage professional is as valuable as a good real estate agent.

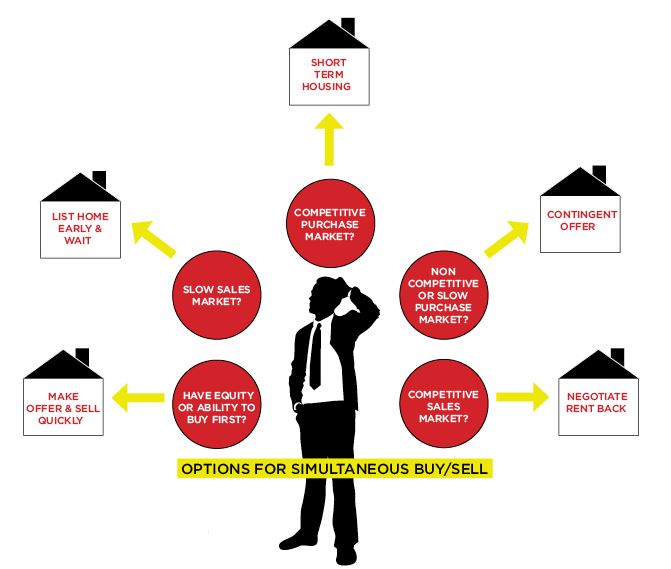

5. Make a plan

Now that you know your numbers, it’s time to come up with a plan and execute. The plan can vary greatly, depending upon any number of conditions. Some examples:

- Buying in a competitive market? Adding a contingency that your current home must sell before you buy probably won’t work.

- Selling in a competitive market? You may be able to negotiate with the buyer for a longer escrow or even a rent back. This would buy you time on the purchase side.

- Selling in a slow market and buying in a competitive market? Need the sales proceeds in order to do the purchase? Unfortunately, you’re in the worst-case scenario. Consider the option of selling your home first and moving into temporary housing. While not the most physically convenient, it could be less stressful.

- Need temporary housing? Start researching those options now well in advance.

Note: Shares of real GDP indexed to 1 at cyclical peak.

Note: Shares of real GDP indexed to 1 at cyclical peak.